Provider level admissions strategies

David Kernohan is Deputy Editor of Wonkhe

Tags

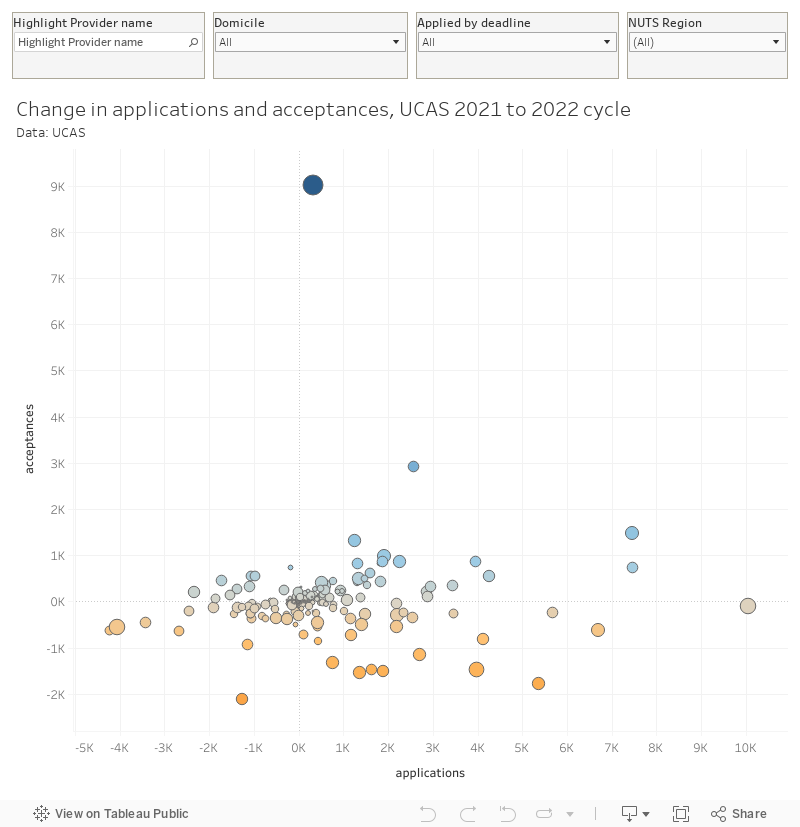

What we are looking at here is – on the vertical axis – the change in the number of accepted applicants between the 2021 and 2022 UCAS cycles. On the horizonal axis, similarly, we see the change in the number of applicants between 2021 and 2022.

You can filter the application numbers by deadline, something you may wish to look at given the emerging pattern of weaker January deadline applications and more strength later in the year. There’s also a domicile filter, that works on both axes (please note the usual UCAS data caveats about Scotland).

The colours show the change in the number of accepted students – I could have used the expected differentiation of mission groups, but this is one area in which we see the idea of mission groups as a unit of analysis break down.

For instance – the bottom right quadrant shows providers making a deliberate decision to limit recruitment (after two or more years of high grades meaning more students got their offer). From most coverage you’d be expecting to find the majority of the Russell Group here, and you do see a few of them – but there are some surprises elsewhere.

Most notably, the bottom left (fall in applications and acceptances) could be argued to show providers becoming less attractive among the applicants they aim to recruit – and there are a couple of big names in here. The top left (fall in applications, rise in acceptances) shows instances where providers are rethinking what constitutes their “usual” intake to continue to grow.

And the top right? Surely here everything is going right for providers, growing in popularity and growing in response? There’s also a lot of franchise/partner activity in here too – most notably at the top and Canterbury Christ Church University. Providers entering this kind of agreement can see a very sharp increase in student registrations at very little cost, but there is no small risk involved with a great deal of due diligence needed from the registry team.

The 2023 cycle – coming slowly to and end, and the 2024 cycle which starts in the autumn will tell us more about what is going on – this is very much just a snapshot, albeit a fascinating on.