When a university is facing extreme financial pressures, what are the alternatives to staff losing their jobs?

As a sector built on the skills and knowledge of staff – academics, yes, but also administrators, librarians, cleaners, IT professionals, marketing and press teams, finance and audit teams, managers, caterers, maintenance staff, vice chancellors, overseas recruitment agents, student support specialists, policy and data analysts, timetabling and estates planning teams, research managers, learning technologists, the registry, and too many others to mention – the primary costs incurred by providers are salary and salary-related.

What are salary costs?

The split between salary and non-salary costs varies by provider, but in most large universities salary costs sat between 40 and 60 per cent of expenditure in 2018-19.

To contextualise that a little, salary costs include all costs relating to paying a member of staff who has a university contract. That would be salary, any taxes (national insurance, apprenticeship levy for most providers), pension contributions, and any additional benefits on offer.

It may include costs relating to redundancy payments or restructuring, depending on how they are counted. It does not include the many people who work for a university without being contracted to them – agency staff – or any of the costs associated with their employment.

Clearly, putting staff out of a job, detrimentally changing terms and conditions, or cutting salaries is enormously undesirable.

That’s not just my position, or the assumed position of Wonkhe readers. There is nobody in higher education who wants to cut jobs unless there is absolutely no possible alternative to doing so. Leaving the compelling moral and ethical issues to one side, it doesn’t even make financial sense.

As anyone who has worked through a period of “restructuring” will know fewer staff doesn’t mean less work needs to be done – and the staff who remain will loudly demand to be compensated fairly for the work they are doing, and will leave for other jobs or other countries, burn out, or continue complaining until they are fairly compensating. And when the financial sunlit uplands return, and one day they will, a provider will just want to take on more staff (at a significantly higher cost when you factor in the training and development required to maintain quality) to meet new demand, expansion plans, or both.

A note on vice chancellors’ salaries

The salaries and other benefits paid to vice chancellors (and to other senior leaders) are under increased levels of scrutiny anyway – a financial crisis will increase this scrutiny. It is very likely that we will see voluntary cuts in salaries – this is already happening, with several vice chancellors, and in some cases the whole executive team, forgoing 20 per cent of their pay. There’s UHR guidance on how to do this.

There is a clear reputational benefit from vice chancellors being seen to make personal sacrifices at a time the whole university is under pressure. It sends a positive message to staff, students, and wider society – though some may use such an announcement to highlight that such pay remains high in comparison to other staff even when reduced. But in terms of making a meaningful difference to university finances, cutting vice chancellor pay is a drop in the ocean.

What other costs do universities have?

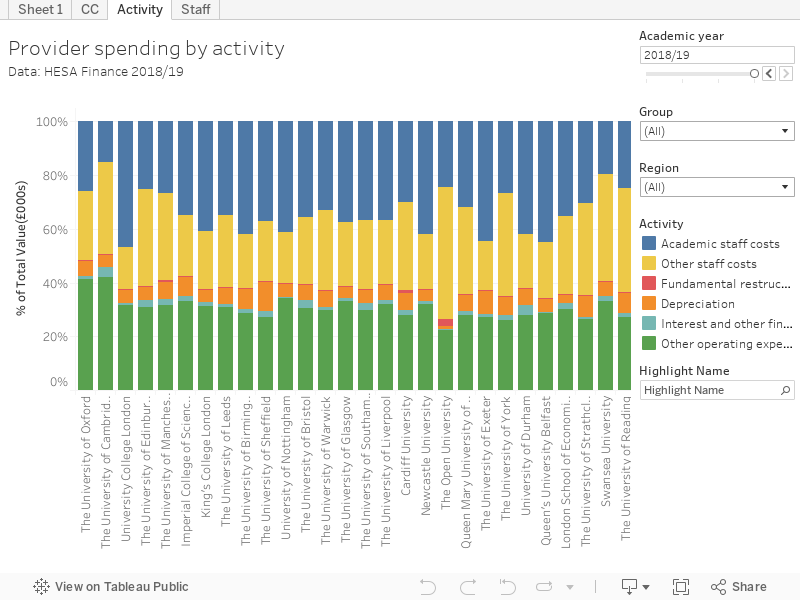

Outside of salary costs, HESA lists fundamental restructuring costs, depreciation, interest and other finance costs – and both the vaguest and the largest outside staff costs – other costs.

The others are broadly familiar terms – depreciation is a measure of the loss of value of equipment or facilities over time (not a cost as we might understand it, no money changes hands, but it needs to be calculated). Interest and other finance costs relate to the costs of borrowing money – akin to the interest and charges you pay on your credit card or mortgage.

Fundamental restructuring costs include things like restructuring and redundancy payments for those moments when your provider needs to take a different shape (schools rather than faculties, merging all central support departments into one structure, that kind of thing).

But “other” costs are a real mixed bag. These include everything from amortisation (like depreciation, but for intangible assets), to maintenance (keeping systems working and buildings standing), to essential infrastructure like phones and IT, to stationery and consumables, to travel. Staff paid without individual contracts are also included in this line – agency workers, temporary administrators and the like (hourly paid and temporary academic staff do have contracts so costs can be seen under the staff line).

Whereas there are likely savings in many of these areas, these can only really be temporary savings. You can forego an IT upgrade or lab refurbishment in the short term, but eventually these things have to be done. And a smaller annual spend often works out much cheaper (and maintains value and functionality better) than doing all the work once every five years. You’ll probably also have spotted that the modifications to the campus needed to maintain social distancing would come under this line.

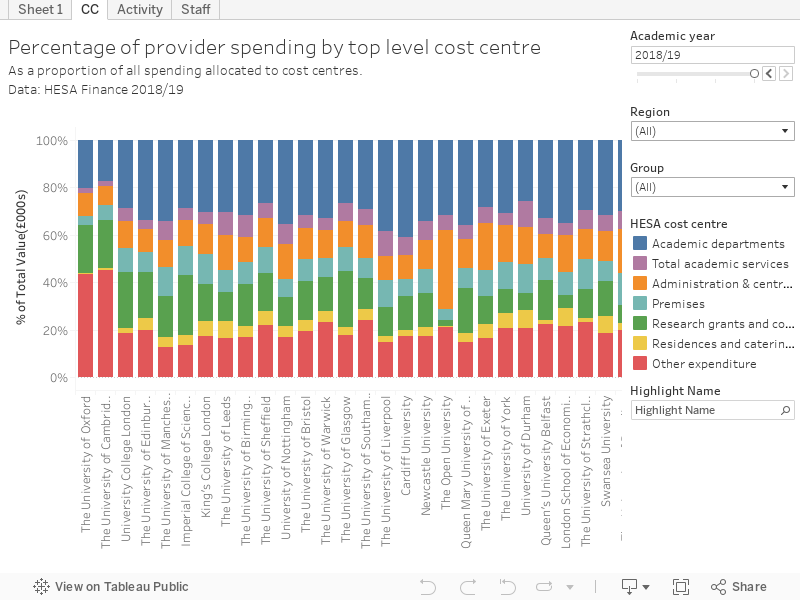

HESA publishes this information by cost centre – allowing you to look at your university’s spending in a more granular way. To do so you should also get to know this document, which explains how each column is used for each cost centre. I’ve built a tool to help you explore granular expenditure in each institution.

And here’s an overview of top-level cost centre spending, by provider.

If you are interested in providers in England, we’ve previously plotted changes in income and expenditure back as far as 1994.

Surpluses and reserves

Universities run as charities tend not to generate large profits each year, though they do aim to generate a small operating surplus. Though this is a positive in that funding supports the activities it was designed to support rather than simply enriching the provider, it is also a negative if you are looking to make cuts to in-year spending if income falls.

These small annual surpluses become a university reserve – but it would be a mistake to think of this as a war chest. To ensure that funds grow at least by inflation most of this income is stored in low-risk investments or in property.

Using reserves to cover gaps in income is not like dipping into a savings account – it is more like selling your house, car, or other assets to raise funds. That said, providers will generally have a small amount of “cash” (liquid, easily accessible funds) available for precisely this rainy day. Indeed, OfS now requires most providers to notify them – as a Reportable Event – if liquidity is reasonably likely to drop below 30 days.

If you are going to sell assets to raise money, doing so in the middle of a global financial downturn is generally not sensible. If a university has an asset worth £10m last year, selling it this year or next year may only yield £8m or £6m. But some providers may find themselves in this position. If I offered you £15 for your mobile phone you usually wouldn’t give me the time of day – but if you needed money and had no other options you might take it.

Borrowing and finance

Nearly all universities borrow money – or have an arrangement with a lender to allow them to borrow money if they need to. We’ve covered this on Wonkhe before.

The pandemic, lockdown, and associated economic slowdown will have an impact on current and future borrowing in different ways. While it is fair to say that many universities will seek to borrow money to cover costs during the 2020-21 financial year (though by no means all), the way in which this plays out will vary on a case by case basis.

Government-backed schemes

We’ve been through the business continuity loans before, in short, such debt is likely to be much more expensive than that which universities have been accessing from other sources, and the volume of credit involved may not be enough to make this worthwhile. It is also worth noting that loans plus interest need to be repaid in three years – the same amount of time that universities will experience the financial detriment from a smaller than expected 2020 cohort as they pass through their courses.

Behind the scenes, the action has been around the Covid Corporate Financing Facility (CCFF). While the other schemes are similar to borrowing from lenders (just backed by government), the CCFF is the Bank of England buying a bond or commercial paper (unsecured, short term debt) issued by your university.

To start off you need to have a credit rating. For example, Moody’s publicly offers credit ratings for nine UK universities, as follows:

| Institution | Moody's credit rating |

|---|---|

| University of Oxford | Aaa |

| University of Cambridge | Aaa |

| University of Southampton | Aa3 |

| Cardiff University | Aa3 |

| University of Manchester | Aa3 |

| University of Liverpool | Aa3 |

| University of Leeds | Aa3 |

| Keele University | Aa3 |

| De Montfort University | Aa3 |

Standard and Poor’s has public ratings for the Universities of Nottingham (A+), Sheffield (A+), Lancaster (A+), and King’s College London (AA-). All of these are investment-grade ratings, based on an analysis of the finances of the provider by each ratings agency (the ratings codes are slightly different for each agency). Where a provider is not rated, it may be able to offer a private rating from an agency, or an internal rating from a bank. However, there are some providers that may not, for numerous reasons, be able to gain investment-grade ratings.

Even if you do have a rating, there are questions around eligibility. Although the Department for Education has indicated that universities are eligible to apply for the scheme there is some doubt as to whether universities can receive credit from the scheme – and the Bank of England has, significantly, not confirmed that universities are eligible or ineligible – they are dealing with applications on a case by case basis.

Under European Union monetary finance regulations, a central bank cannot offer finance that contributes to the national deficit – a rule generally understood to mean that central banks cannot lend to the public sector. Whether or not universities are public or private sector is a complex conversation, but in raw financial terms there appears to be a rule of thumb (though this is hotly debated!).

If something gets more than 50 per cent of funding from the government, it may be classified as public sector – though as above the simplicity of this formulation does not capture the full conversation. Depending on how the decision is made, a lot of universities may not be eligible. And defining precisely which income is from the UK government is far more difficult than it might look at first glance.

Some universities have been given approval in principle for CCFF from the Bank of England. Others have applied and are waiting to hear back. This is a live issue – we don’t yet know of any providers that have been formally turned down, or providers that have received funds. Though details will, eventually (para E6 of these BoE notes), be published.

Other sources

It may be hard to believe, but despite the pressures universities face, they are still attractive places to invest. For nearly a decade and a half, UK universities have benefited from the availability of cheap finance – using carefully planned borrowing to invest in estates and capacity. A few have issued public bonds, but the majority have benefited from private placements and bank lending.

I asked a banker if this mood would continue. Ian Robinson from HSBC told me that:

UK higher education remains a globally leading sector. It continues to be attractive for bank lenders and private placements, though the current uncertainty does bring the timing of financing requirements into focus. Every institution has different exposures, so therefore each request will be looked at on a case by case basis.”

However, it feels fairly likely that providers that were struggling financially before Covid-19 hit would have a harder time borrowing money. And, because historically universities have worked bilaterally with their lenders – the available capacity to provide finance may be lower than might be liked.

Lending to universities is generally not backed by a security (for example a bank will not hold a charge over a campus while a provider pays a loan back, in the same way that the bank effectively owns your house while you pay back a mortgage). Instead, lending is backed by covenants – agreed levels of financial performance that act as warning lights for lenders.

You can get positive or negative covenants or conditions – an example of the former would be a requirement to hold a certain amount of cash, or to spend borrowed money on a stated goal. Examples of the latter would include not being able to take on further debt without permission from the first lender, or maintaining a certain ratio of assets to income.

Every lender wants to be paid back, so it is not in anyone’s interest for providers to fail financially. If a provider feels like it is at risk of breaching a covenant they should be talking to their lender long before it happens. It is much easier for a lender to amend covenants (citing the unique circumstances brought about by Covid-19) than to disregard them (a lender would be negligent if they did so!) once they have been triggered. This process could involve, in extreme circumstances, the reclassification of debt or the reprofiling of repayments.

But – to be absolutely clear – no bank or lender would want to close a university. Apart from the massive reputational damage (which is a key consideration), it would also limit their chances of getting their money back.

A few other issues

It would not be possible to write about university finance without mentioning pensions. You might recall that HESA’s release of 2018-19 Finance open data included pension adjustment costs that were levied in-year by USS following the 2017 valuation.

Although USS assures us that they are working to optimise their investments during the Covid-19 downturn, it is not outside the realms of possibility that a similar thing would happen again in future years – should the downturn turn out to be “U” shaped or “L” shaped rather than “V” shaped. While this would eventually have an impact on provider finances in itself, pensions liabilities (and security to cover pension liabilities) do sometimes turn up in covenants which may be attached to new borrowing.

I’ve also not mentioned accommodation. Even if recruitment holds up, the number of students taking up places in halls is likely to fall for the 2020-21 academic year if it remains likely that social distancing and remote learning will be in place. This is a straightforward loss of income for providers that own their own residences – though some may increase prices to limit the damage. However, some providers have what is called a “nomination agreement” that commits them to sending a certain number of students to privately-owned halls – in normal times a sensible way to offer accommodation to students without much of the development and maintenance cost. If these agreements are breached, there will be a financial detriment to the university.

It works a bit like this. A university sells accommodation blocks to an accommodation provider who offers them a long lease in exchange for a cash receipt that they have long since spent on other campus improvements. The university is contracted to pay the accommodation provider, which in turn needs to pay its own investors – because it borrowed the money in the capital markets to pay the university in the first place. If the university doesn’t pay, the accommodation provider will have to hand the keys back and sue the university!

In summary

There is no magic bullet. Borrowing has always played a big part in university finances, as it does in any business that sets out to expand, upgrade and update.

While universities revisit their business plans and strategies to reshape and reform to suit the changed circumstances, deferring or cancelling larger maintenance or expansion plans will offer short term breathing space, but providers that do this could be storing up costs for the future and losing capacity just at the moment the demographics tick upwards.

For the same reason, staff cuts feel inevitable, even though the capacity lost here will be difficult to replace. As demand for university places expands over the next five to ten years as is widely predicted, this capacity will be urgently needed.

Nobody is actively relishing the idea of taking on more debt (with the associated costs), losing staff, or letting buildings and systems deteriorate. None of these, looked at in the long term, make any sense at all – and each will bring short and medium-term pain into what is already a difficult situation. What should be clear, however, is that government support to maintain the status quo is unlikely to materialise. The world has changed and universities will be forced to change too.

Further reading

What to expect for the next three years – to accompany the above blog, this is my piece setting out the wider financial situation that the sector faces.

BUFDG’s “Understanding university finance” is a superb read.

On Wonkhe Gary Guadagnolo from EAB shared the results of a survey showing what providers around the world are already planning.

Andrew McGettigan has written a report for the University of Sussex branch of UCU, which takes a deeper look at borrowing and covenants.

On Discover Society Stephen Connelly takes another perspective on covenants.

And here’s our regular look at the HESA Finance data, from earlier this spring.

It is probably too much to hope for that the current difficulties lead to a review of the misguided decision to abolish the binary divide ( a decision preceded by an equally misguided decision in Australia). Considerable sector-wide savings could be achieved therein. Leaving that little issue aside, as someone who worked in HE for 40+ years, mostly at a senior administrative level, it is hard to deny that there is considerable scope for expenditure reductions in universities. Too often commentators ( and consultants) who should know better conflate “costs” with expenditure and infer that there is some iron law… Read more »