The HESA finance dataset is always fascinating to explore.

Since the start of the “open data” series you could lose days in there – during lockdown I fully intend to get in depth with the 2018/19 data and some longer time series. But this year attention will be on one measure alone: the level of exposure to an expected downturn in international student recruitment.

There are several very well known providers that derive a larger proportion of their university fee income from international students than from home students. The higher fees, paid upfront in the main, are widely understood to offer a surplus that supports loss making activity elsewhere. The loss or severe shrinkage of this income in 2020/21 will, unless mitigated, run the risk of being catastrophic.

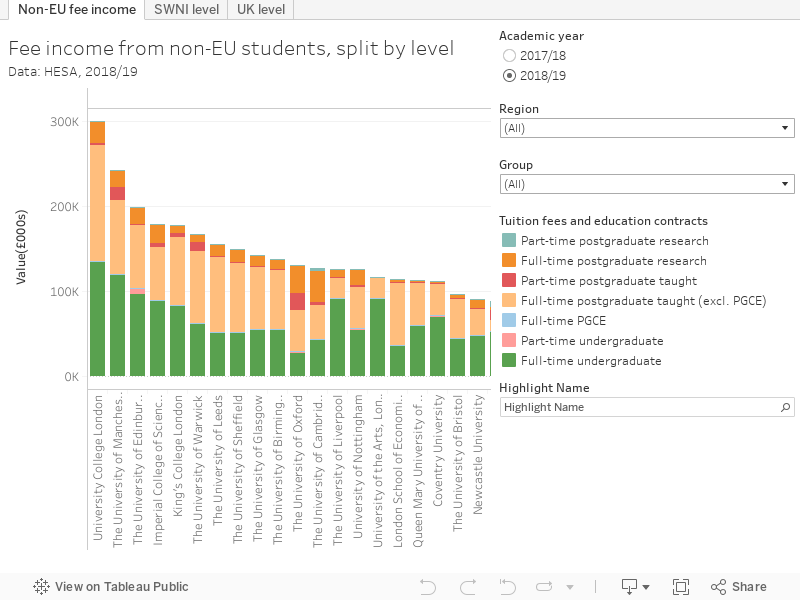

Overseas student income

Here’s a league table of overseas (non-UK, non-EU) income, showing the level and mode of provision involved. Note that for all these visualisations I have rendered the money involved divided by 1,000 (as HESA does) – it makes it easier to read and assess overall proportions, but you need to remember to multiply by 1,000 to get the actual figures.

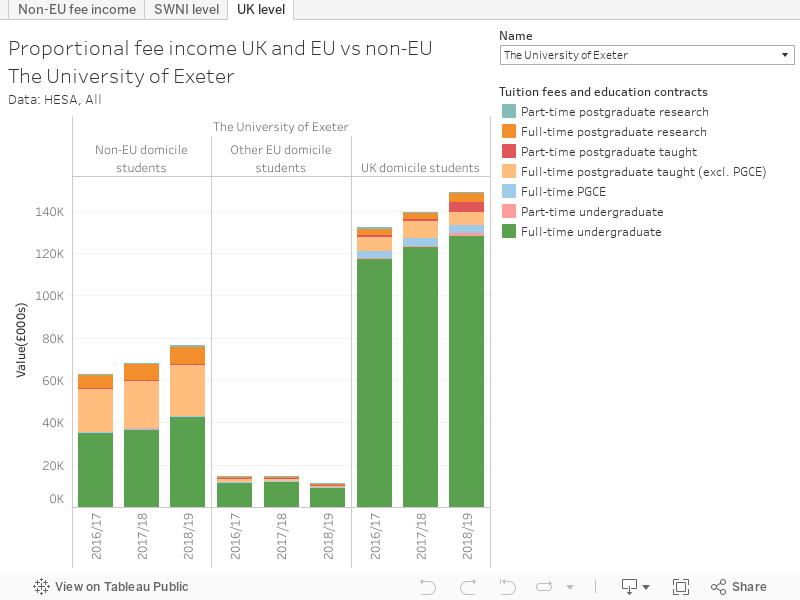

You can see some familiar names making serious money from overseas recruitment, but it is perhaps more helpful to see this in the context of all fee income and over time. Here we see this data for Imperial College London – you can use the filter to see three years of data for any institution you are interested in.

For readers in Scotland, Wales, and Northern Ireland there’s a more detailed visualisation showing two years of data for home student income separated out from others in the UK.

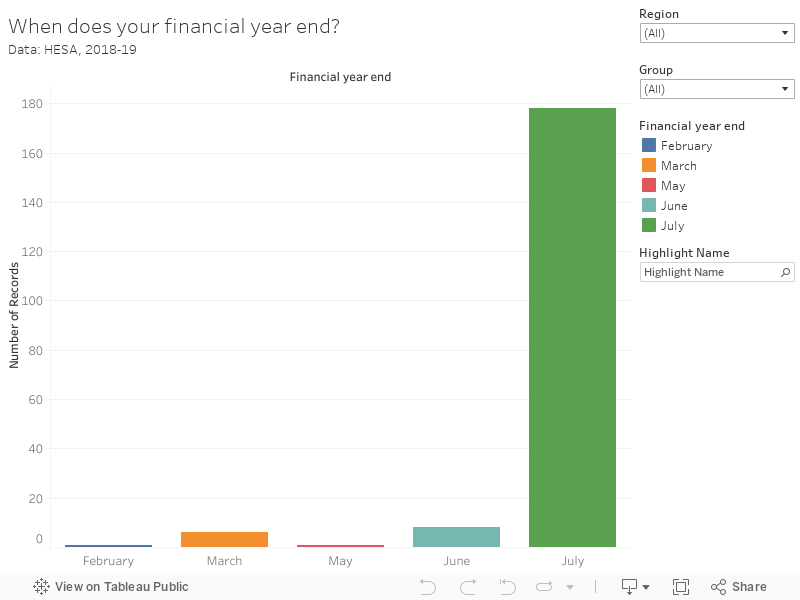

This year’s data

A quick look at those filters should clue you in that a lot more providers are featured this year. Some very clever background work by HESA allows us to peer for the first time at the balance sheets of those providers with financial years that don’t end on 31 July. The expansion of the sector means that the HESA Reporting Year is no longer the standard – there are now 10 different financial years, and this release is only the first of a number of releases planned for 2020.

There’s not many providers that deviate from the July norm, though it is great to have the data:

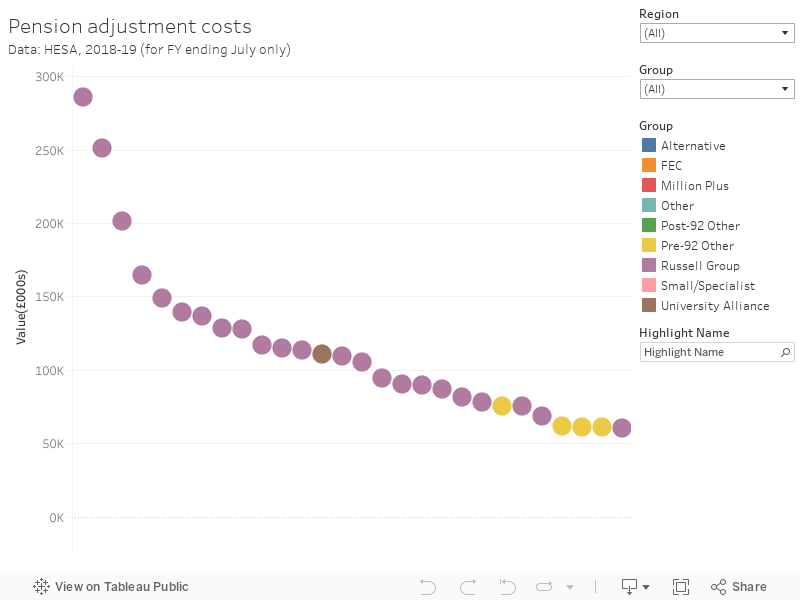

Pensions costs

One characteristic of this year’s income and expenditure data is a general turn into deficit – with a significant in-year adjustment to some providers’ Universities Superannuation Scheme (USS) costs following the 2017 valuation. HESA is quick to point out that this is a non-cash expense, and should not be seen as reflective of underlying financial performance.

Those providers with large numbers of staff with USS pensions have a greater exposure to this effect – but do recall that many non-USS providers do contribute to staff members’ USS pensions where they have them.

One interesting fact we can learn from this is which non-USS universities and colleges have an exposure to USS costs.All this has an impact on this years Key Financial Indicators.

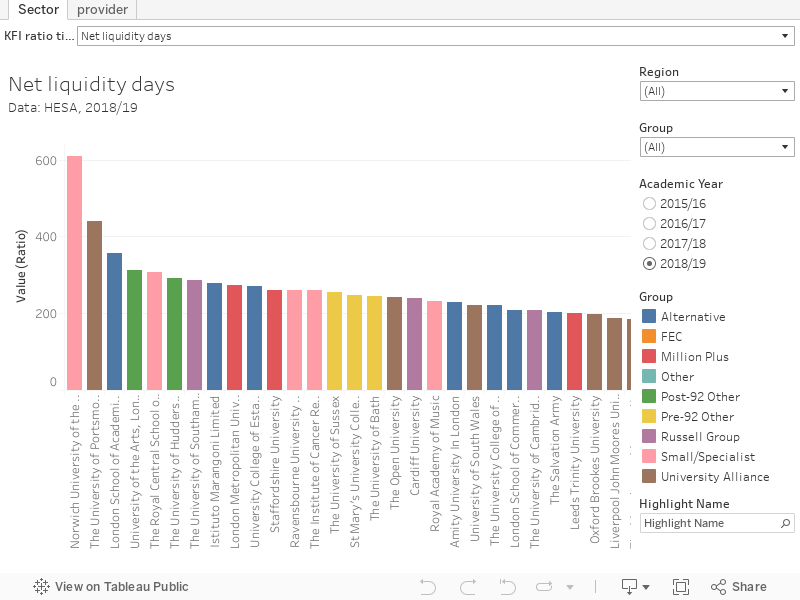

Key financial indicators

Depending on your personal preference, one of the key financial indicators would offer the most useful insight into the underlying financial health of a provider, and once again we get a set of common ones from HESA in the open data release. I covered these in a bit more detail last year, but here are four years’ worth of data from the 2020 release.

You’ll see the default display is kind of a league table for each indicator (use the filters to choose your indicator and academic year), but you can look at a single institution time series on the other tab.

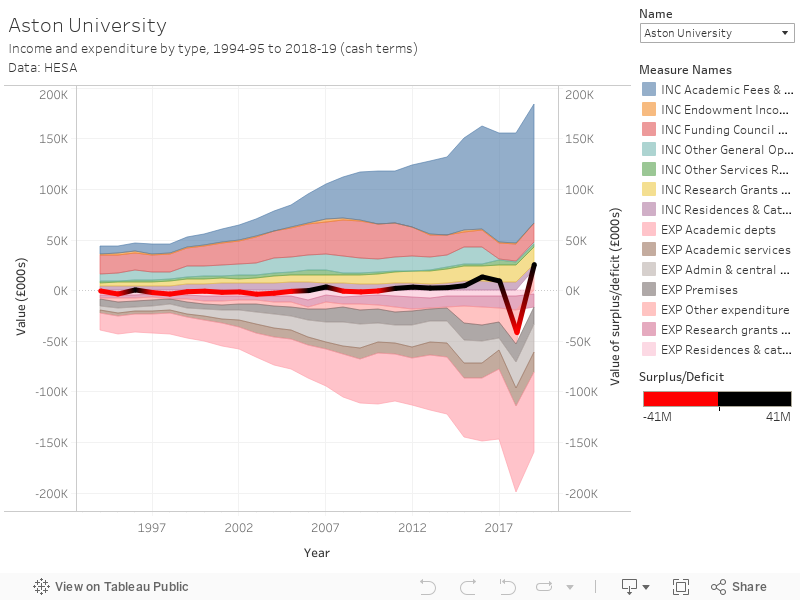

The long tail

As before I’ve taken a longer term look at income and expenditure (and surplus/deficit) in top level categories, with some comparable data available going back to 1994-95 for some larger English providers (though there’s at least two years for nearly everyone). This is in cash terms (not adjusted for inflation).

Eventually I will work this back for as many providers as I can – I’ve made what I think are sensible assumptions concerning stuff like mergers and changes in the presentation of HESA data, but if something looks odd please do let me know.

And finally…

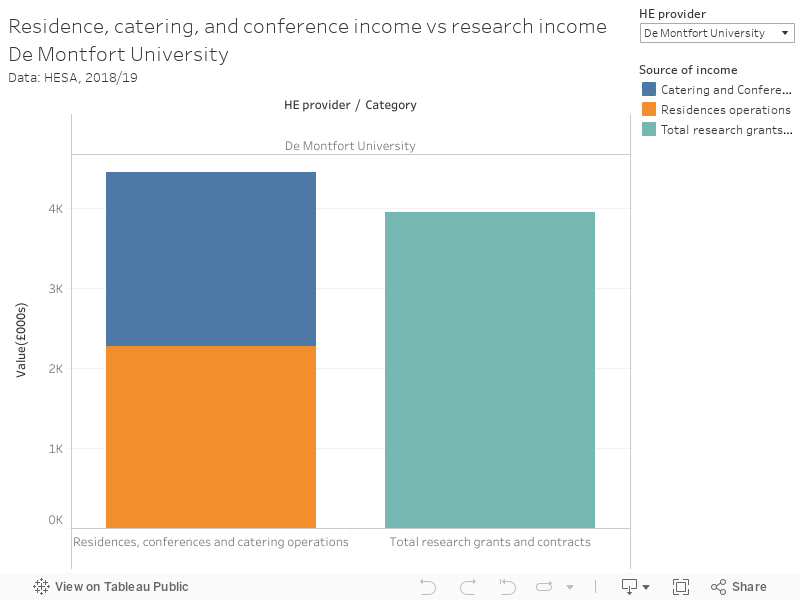

Ever since I started publishing finance data visualisations for Wonkhe, people have been delighted to have the ability to learn whether their university earns more from research or residence, catering, and conferencing. Aside from highlighting the hard work of some of the least frequently celebrated staff in the sector this visualisation also serves as an indicator of the scale of another income stream that will look very different for 2019-20.

Excellent Analytics…….

Thanks for the article https://wonkhe.com/blogs/which-providers-are-exposed-to-a-downturn-in-international-recruitment/ !