The confirmation of sector eligibility to parts of the generic government package for business was easy to overlook in last week’s announcement.

The government focused on the big headline numbers, while the sector focused onto the fact that these numbers were just future payments moved forward a few months and the oncoming mess that is the semi-controlled recruitment process for 2020. But what benefit could universities get from furlough and the various loan schemes that Ministers were so keen to promote?

A category error

There’s a tendency to wring hands over sector borrowing, but it plays and will continue to play a huge role in the way providers invest in capacity and the potential for growth. Borrowing to replace recurrent income is a more worrying practice, and this is what is being promoted.

The Coronavirus Business Interruption Loan Schemes (the main CBILS and the variants for SMEs and larger enterprises) provide a significant cash input, which suits in particular businesses facing an almost complete drop in income during lockdown. This emphatically is not the case for the sector – there have been some income losses (notably accommodation and catering, but also from commercial research contracts) but nothing on the proportional scale faced by restaurants, shops, gyms, and factories. Similarly, the furlough scheme covers staff costs during a period that these would not be covered by business income.

Picking through the available statistics on the impact of coronavirus highlights just what a poor fit universities are to this pattern. The Business Impact of Covid-19 Survey (BICS) conducted by ONS finds little evidence of impact in the education sector generally – there’s some evidence that prices of good sold (fees charged to learners, I guess) are falling, but we don’t get any sense of this under imports or exports (either of which could include international student fees). Other than the water and waste sector education is less affected by a loss of available financial resources (the ability to borrow) than any other part of the economy. Incidentally, seventy seven per cent of the education workforce are working remotely, higher than most other sectors.

Because the main chunk of income for most providers (tuition fees and associated payments from funders) comes in three chunks based on student numbers at the start of term the big shock has yet to hit. There is the potential for it to hit, and hit hard, following the conclusion of the 2020 recruitment cycle – with the damage being seen in the first payment (Autumn 2020) from the Student Loans Company.

The primary government measure to address this is the reprofiling of SLC payments. In a typical year 25 per cent of fee income arrives in the autumn, 25 per cent in January, and the remaining 50 per cent in May. In 2020 the January payment will be made alongside the first one, leading to an organisationally crippling version of waiting for your January pay packet after Christmas except your first salary will come in May.

So January 2021 is now when we expect the pain to arrive, at the same time that (hopefully) society completely emerges from lockdown, in-person tuition is back in place at universities, and the remaining Covid-19 emergency measures are memories. It’ll be just us. We do get a few months to prepare for this, even though we don’t really get the tools we need to do so.

Furlough furlough

The non-specific elements of the sector support package, as above, are CBILS and the Coronavirus Job Retention Scheme (CJRS, more commonly known as the “furlough” scheme). These are designed to support immediate cashflow issues, but some canny providers willl be exploring the opportunity to use these to build a financial cushion for the new year.

Turning first to the furlough scheme, it doesn’t take much searching to find pages like this from HE providers making use of the provision. The pattern is generally similar – furlough is available for periods of three weeks (the minimum permitted time) and upwards for staff who:

- Are not physically able to do work they are employed to do because of the lockdown, and cannot be redeployed

- Are not required to do the job that they are employed to do because of the lockdown and cannot be redeployed

- Have lockdown related caring responsibilities meaning they are unable to work

- Are funded via an external income stream, which has paused or ceased.

In general providers appear to be topping up the 80 per cent of salary available from the government to allow for full pay for staff who are furloughed. This is primarily affecting non-academic staff, and some academics employed on research-only contracts. Casual staff are eligible for furlough in some cases, though we know that staff on casual contracts are suffering in many parts of the sector.

The upshot of all this is that providers are able to save 80 per cent of their salary bill for a small number of staff – which could maybe contribute to a financial cushion for January 2021. Quite how small that number is remains unknown – we know from the ONS that businesses in the education industry are least likely to be using the furlough scheme, and – indeed – least likely to be using any available government scheme. Across the whole education component of the economy, staff are less likely to be furloughed than any part of the economy other than health and social work.

Are higher education providers seeing significant benefit from their use of furlough? It seems unlikely.

Continuity announcement

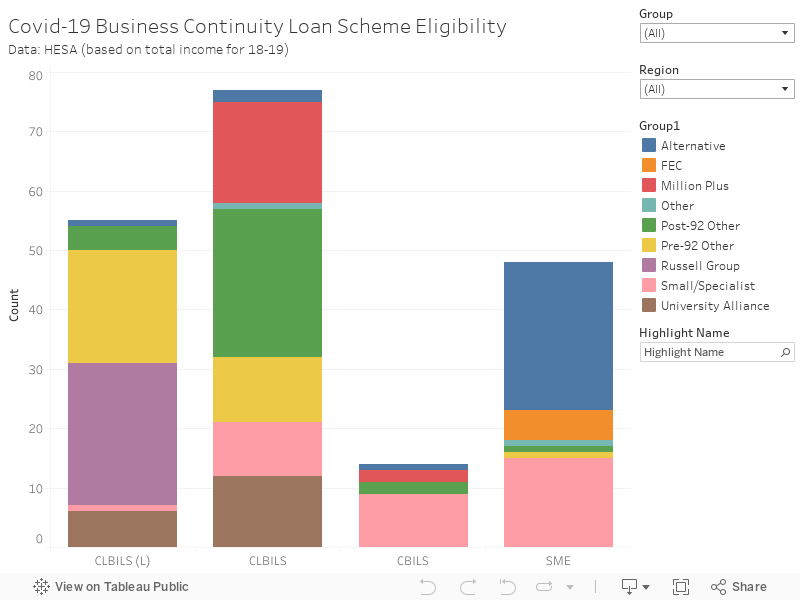

The various business interruption loan schemes are banded based on business turnover.

- SME/“Bounce Back”: For SMEs (that’s turnover under £25m) loans up to 20 per cent of turnover, up to £50,000, are available. These are repayable over 6 years at a 2.5 per cent interest rate, and there are no repayments or interest for the first year.

- CBILS: For the mainstream of businesses including those in the SME category (with a turnover below £45m) there is access to various forms of finance (loans, overdrafts, invoice finance, asset finance) up to £5m. Borrower fees are covered, and the first 12 months are interest free.

- CLBILS: Larger businesses get access to larger sums, with three years to repay. There’s up to £25m for businesses with a turnover of between £45m-£250m, and £50m for a turnover above £250m.

(If you are a primarily grant funded Further Education College, you are not eligible for any of these schemes.)

We need to be clear here that eligibility is not the same as access. These are loans that, although backed by the government, are actually managed by private lenders (your usual banks and specialised lenders) – who also get to decide whether or not you get the money and how much of it. There’s not an overall cap on the amount of money available, though I wouldn’t bet on this largesse lasting.

You need to have “a borrowing proposal which the lender would consider viable, were it not for the current pandemic, and for which the lender believes the provision of finance will enable the business to trade out of any short-term to medium-term difficulty”. It is almost identical to the usual process of applying for finance, with the caveat that those who are used to applying for finance would be likely to have existing finance arrangements that would cover them rather better than this offer. You also need to self-certify that your business had been adversely impacted by Covid-19.

For the sector (I’m using annual income, which isn’t quite the same thing as turnover, but a decent enough proxy for this purpose), this eligibility would work out approximately as follows based on the latest available public data.

Nobody eligible for the SME loans would be eligible for anything less than the £50,000 maximum from that scheme – individual providers would need to work out where a loan of basically one senior academic salary on such terms is worthwhile for them. You’ll see that the entirety of the Russell Group is eligible for the higher CLBILS rate, with all of the pre-92 sector eligible for CLBILS at one of the two rates.

What difference would this make?

How helpful these schemes are will vary on a case by case basis. Clearly £25m is not to be sniffed at, but paying it back over three years is a different matter. It might be possible to cover the terrible trifecta (the value of one year’s absence of international fees, accommodation income, and commercial research) but the level of the repayments for such a short term loan at an unknown rate of interest would be very challenging. The assumption would need to be that income would speedily bounce back above the norm in following years to allow for some fairly chunky repayments. We cannot say this for certain.

It’s far from clear what the overall long term economic impact would be from Covid-19. The Office for Budgetary Responsibility has taken considerable stick for modelling a deep, V-shaped recovery – other observers see a slow and painful call back up to current levels. The quicker return is more likely for the shops and factories the loan and furlough schemes are designed, whereas we know poor recruitment for a higher education provider in 2020 will provide an income detriment until at least the end of the 2023-24 academic year.

It remains clear that the government has not fully considered the particular financial pressures the sector is under. The profiles of likely risk and detriment do not compare to other sectors, and in a rational world there would be specific mitigation designed for the unique circumstances facing higher education.

Interesting observations -I can’t help but feel that Higher education is caught between a rock and a hard place. We are neither public sector nor private sector enough.

Government wants us to operate like a business, but wants to control student fees and regulate significantly. We are not a public good, but we are funded by public money (even though students are taking on a huge private burden. Government gets a huge financial asset on its balance sheet from this exploitation and it has no incentive to change tactics). The government has little to no regard for students and the “Office for Students” is nothing but a policy tactic to pretend they care about social mobility and value for money. If they really cared, they would address tuition fees policy. OfS is currently showing is more about restructuring the sector and consolidating it rather than student advocacy and experience.

No wonder public sympathy for our sector is at an all time low because government policy of a hybrid “public-private” model damages value for money. We urgently need to shift the privileged perception of the sector, which is not helped by VC’s remuneration.

The use of furlough leave in HE, or rather the lack of it, has become something of a preoccupation of mine.

When I look around (very much a straw poll), I see universities delaying furloughing for a very long time – even for colleagues in cleaning/maintenance teams, conference/events roles, and other non-student-facing teams, where switching off entire functions or moving to skeleton staffing for a while is a distinct possibility.

One colleague said to me recently about their university (two and a half months after furlough funding was first available to the sector), “Our HR team is starting to come up with a plan for furloughing”. Only starting? In early May? That’s a decent chunk of two and a half months’ wage bill that the university has missed out on.

I can understand why there was reluctance and delay.

Furloughing is complex, often messy. It can create friction. It involves having to deal with people’s reactions when they find the shutters down on a particular team or service.

The focus was on keeping the wheels on the bus, as well as on shifting teaching online. In that context, furloughing might not have felt like a priority.

Plus there was confusion – probably unnecessary confusion – about whether universities might be seen as public sector and, therefore, a sector that shouldn’t be furloughing.

And all the talk of a ‘bail-out’, fired up by UUK, has probably not helped, as it created a sense of hope (or complacency) that common sense will prevail and that the government will come through for HE in the end.

I agree furloughing was never going to solve HE’s problems. But I’m not sure the sector has even tried to make proper use of the scheme.

If common sense does not prevail – and a government bail-out, on the scale required, does not materialise – universities may regret not using the scheme to cushion themselves a little better as we head into 20/21.