There are so many ways to plot the financial impact of Covid-19 on universities – but they all end in despair.

Research from London Economics, commissioned by the University and College Union, focuses entirely on income from undergraduate tuition fees – from home, EU, and global students. This contrasts with Wonkhe’s earlier approach, which looked at international fee income at all levels alongside income associated with commercial research and accommodation-related income.

Scary headlines

The headline from LE/UCU is a £2.5bn black hole in tuition fee and teaching grant income only – with a prediction that 111,000 fewer UK and 121,000 fewer international first-year undergraduate students attending. You’ll note this is a limited analysis, in the sense that post-graduate fees are a substantial part of provider income and are mostly not dealt with here.

Primarily focusing on undergraduates is a fair method to use, however, as the shift from direct funding to fees for home and EU students over the last ten years in England, Wales, and Northern Ireland has made this area of income one of the most volatile that providers have to deal with. But in looking at the figures in this new report, we need to be clear that these do not represent anything the whole story.

Predicting future recruitment patterns is an established part of the way sectors function – a lot of resources, both internally and externally, are focused on making these predictions based on previous student behaviour. What LE have done here is to use evidence from previous global downturns, most notably the 2008 recession, to map the impact of aggregate predicted changes in HE demand on individual providers. Though the research doesn’t name specific providers – it uses clusters of providers with similar characteristics for the most part – it is able to make nuanced assessments of likely recruitment patterns.

What rings through the whole report is the desperate need for additional government funding this year – we are cautioned that, in reality, the impacts will be far worse than presented here. This is both in terms of provider financial impact and a wider direct, indirect, and induced, economic impact on the UK economy.

Dropping a baseline

To have any understanding of the way sector finances may change we need to know about the state of the sector right now. The most widely used means of doing so is HESAs open data finance release, which covers academic years up to 2018-19. LE base the current state of the sector on the figures for this most recent available year – a reasonable, if imperfect, proxy.

This introduces us to the variability – both in terms of recruitment and financial position – among the HE sector. LE’s clustering process separates Oxford and Cambridge (cluster 1) from other major pre-1992 providers (cluster 2). Other pre-1992 providers are mixed in with some of the most notable post-1922 providers (cluster 3), with the remainder dealt with elsewhere (cluster 4). This is from older LE research – annoyingly clusters are not of equal size in terms of recruitment, and the size in institutions varies from 2 to 67. We see a greater reliance on international student fee income in clusters 1 and 2, as we might expect from previous research, and this is put in context (for the cluster) of top level income and expenditure.

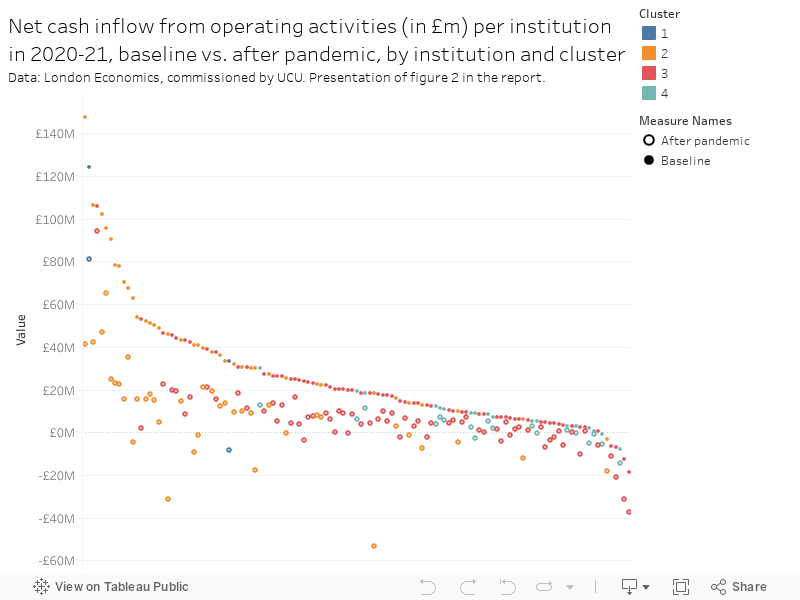

There’s also an in-depth look at net cash inflow from operating activities as a proportion of total income. This is a HESA key financial indicator that gets past some of the problems in looking at straight profit/loss calculations, as it doesn’t include non-cash expenditure – significantly for 2018-19 this gets rid of adjustments for pension liabilities. The KFIs (as I’ve covered before on the site a number of times) are different ways of understanding the overall financial health of a provider – and here’s a provider level plot:

As LE puts it:

“In general, the estimate of net cash inflow from operating activities as a proportion of total income is typically approximately 10-12 percentage points higher than the standard measure of surplus or deficit as a proportion of total income. In the absence of significant financial reserves, we would define organisations with a net cash inflow of less than 5% as facing significant operational challenges in the medium term (as insufficient cash reserves are being generated to service debt or to build up cash reserves to pay for necessary capital refurbishment for instance). Most institutions that focus on net cash inflow would target achieving at least 8%.”

So – less than 5 per cent is probably (provider reasoning may vary) bad.

Pandemic panic?

It’s when you put all of this into the context of a likely downturn that we start getting really depressed. LE takes the notably pessimistic OBR estimate of a 13 per cent decline in UK output as a result of the pandemic and associated economic slowdown as a starting point.

They cite two potential effects of a slowdown on recruitment – a counter-cyclical effect on full time enrolment (so there’d be more full time students in a recession because there’s no jobs) and a pro-cyclical effect on part-time enrolment (if there’s no jobs no-one will take the odd half-day to do a course that they could do quicker full time).

These two pieces of information suggest a 0.03 per cent increase in full time enrolment per percentage point decline in growth, and a 0.56 per cent decrease in part time enrolment. So on average they predict a 1 per cent average increase in full time recruitment and an 8 per cent decline in part time enrolment – equivalent to 11,550 less students in total. A similar analysis of international student recruitment suggests a minimum 1.5 per cent reduction in international student recruitment, equivalent to around 14,000 students. These figures, of course, get scaled up on the application of the LE sector model.

You might think that this sounds a little simplistic, and – fair play to LE here – the report is clear that this is a partial estimate of an overall trend. It is very likely some students will choose to defer – either in hope of a better experience starting in 2021, or to deal with more pressing issues at home or in their community.

So there should be big caveats around all these figures – there’s a dive into survey data but nothing conclusive that can be sensibly modelled with. Which was pretty much my conclusion after playing with similar ideas earlier in the week.

Bottom line

These reductions are mapped into the clusters from earlier to offer a sector level estimate – so rather than just taking the numbers of the top of a sector level figure there’s some nuance going on. I’d wonder if you could do a similar exercise weighting by provider – so much of this is a work around for the fact we don’t know anything other than the average income per international student by mode (and level), so the smaller our boxes the better the overall averages would be.

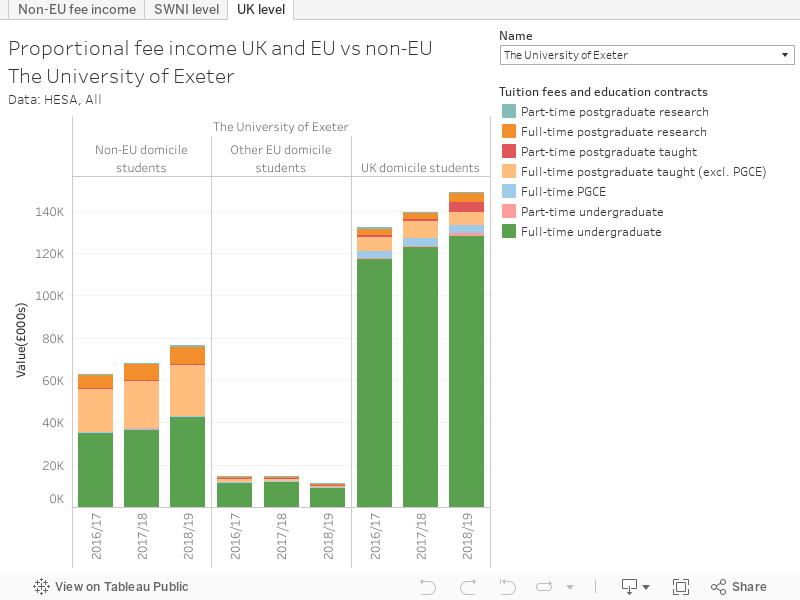

So your total of around 23k first year enrolments down would impact primarily on sector 1 and 2, what we could politely call your most prestigious providers – both in financial terms and raw headcount. This is because of the variation in underlying institutional reliance on institutional fee income, which I’ve plotted in more detail as a dashboard for you here:

Following this through to the impact in net cash inflow from operating activities gets very concerning – we go from most places looking healthy around 10 per cent to a sector average of a deeply worrying 2.9 per cent. Obviously Oxford and Cambridge (cluster 1) distorts this a but we are looking at a shift from a general position of health to a general position of ongoing concern. 36 providers end up with a negative cash inflow position, meaning that a number of renowned providers will be relying on their reserves to get through the year.

We then follow this through to the wider impact on the economy – which would lose, at a conservative estimate £6.1bn and around 62k jobs (around half of which would be outside of the HE sector).

Competition

It is LE’s position that the proposed student number cap (for UK and EU domiciled undergraduates) would be undershot by nearly all providers – meaning that competition for students will be particularly deadly for providers less equipped to compete. Universities in cluster 2 have the greatest loss from falling international numbers, and thus the greatest incentive to recruit more home students (even though this would be unlikely to plug the financial hole).

The report raises the interesting question of a “two-sided” rather than “one-sided” cap – which would offer providers a minimum guaranteed recruitment level. The current one sided design would have a heavy cascading effect:

“In particular, if Cluster 2 institutions take 7,700 prospective students from Cluster 3 institutions (in part to offset losses to Cluster 1 institutions), then Cluster 3 institutions would have the incentive (and potential flexibility) to poach 20,695 students from Cluster 4 institutions. This would essentially more than double the pandemic effect already impacting these institutions.”

I’d hope that this is an unintended consequence – but clearly if you see a bailout as an opportunity to preserve as much of the sector as possible then this effect is unhelpful to say the least.

Summary

This is an excellent and timely report – which should give sector leaders, and staff in the DfE and Treasury, much to consider as negotiations over the sector bailout continue. To me it emphasises just how complex and multifaceted sector finances has gotten, and how the risk introduced into recruitment has offered so many problems alongside so few measurable benefits.

David Green, University of Worcester writes:

“The London Economics Report predicts that Oxford and Cambridge will lose 1775 UK students next year, which is clearly incorrect given the desire of so many outstanding young British people to secure a place at these two universities.

“This wholly misleading prediction is based on a straightforward methodological error which assumes that 14% of all young people will defer their place at university this year and that this applies to each university in Britain equally. Sadly, this error invalidates much of the rest of the report – particularly the sections on regional impact which significantly underestimate the negative impact of Covid-19 on the Midlands and the North.”

It would be interesting to know who set the parameters for the research- the academics or the union?