For any solution to what the higher education sector currently faces to be seen as successful it would need to have the following attributes:

- It preserves sector capacity and quality

- It preserves student choice (which I deal with here)

I’m also going to need a scenario to examine, so I’ve built what I think is a reasonable worst case.

Following Boris Johnson’s full recovery, lockdown is lifted gradually from June 2020. However, a larger than expected number of people are asymptomatic carriers of Covid-19, and both infections and deaths begin to rise sharply. The UK re-enters lockdown in mid July 2020, with the expectation that it will be at least 12 weeks before life can begin to return to normal. This brings the economy almost to a standstill. With no time to reschedule the start of term, students continue to apply to university with the expectation that most if not all of their first term will take place online, and few if any reserve accommodation before they can be certain they will use it. Nearly no international students study at UK providers during this period – other countries have left lockdown and students express a preference against online provision.”

I should add I am focusing here on English HE, because of differences in the financial and policy environments in the devolved nations.

Preserving capacity and quality

By preservation I mean not just for the 2020 cycle, but for 2021 and onwards. People clearly do want to go to UK universities – the proportion of UK 18 year olds applying and accepting places has increased every year, as have international student numbers. Clearly the market is demanding more HE, and we need to be able to offer them it.

By capacity and quality I mean that a similar or slightly larger number of places would be available for undergraduates to commence for the 2020-21 year and beyond – and that these places will be at the same or greater quality as current places. Students should not have to deal with unexpectedly higher staff student ratios, or less access to resources and equipment, or difficulties in securing accommodation, in the same way as they should not in any other year. And we use the sector for a lot of other stuff too – we need the capacity for research and development, the capacity for civic activity, and the capacity for other economic benefits.

All of this requires financial stability, which is where the proposed bailout comes in.

Financial capacity

Update 24 April: A few errors had crept in to an earlier version of these figures, these have now been corrected. Thanks are due to alert reader Peter Thompson.

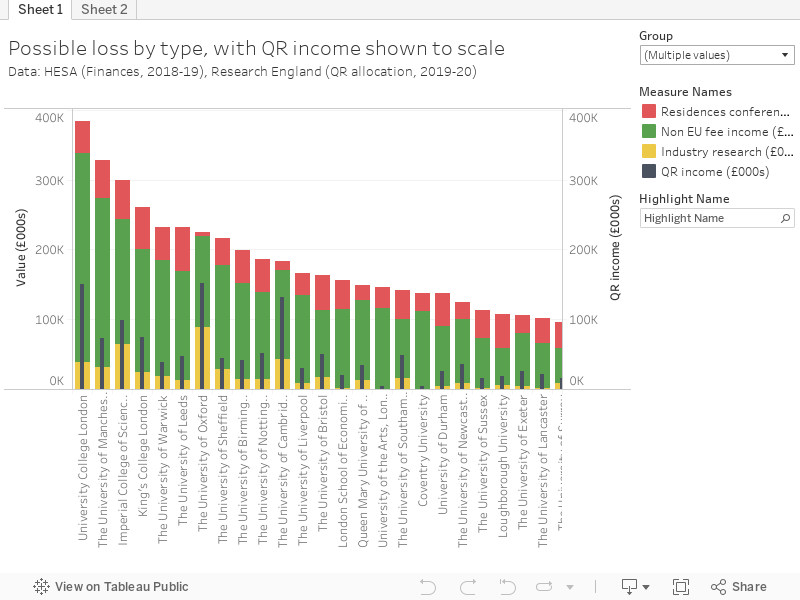

By my reckoning the three areas where providers are likely to be facing an unexpected short fall this and next academic year are:

- Non-EU overseas fee income – as overseas recruitment crashes due to a reluctance to travel, and a lack of English language testing provision.

- Residences, catering and conferences – given the collapse of conference business, the closure of campuses, and residence refunds for 2019-20 and likely delays in income for 2020-21.

- Commercial research income – given the global economic slowdown.

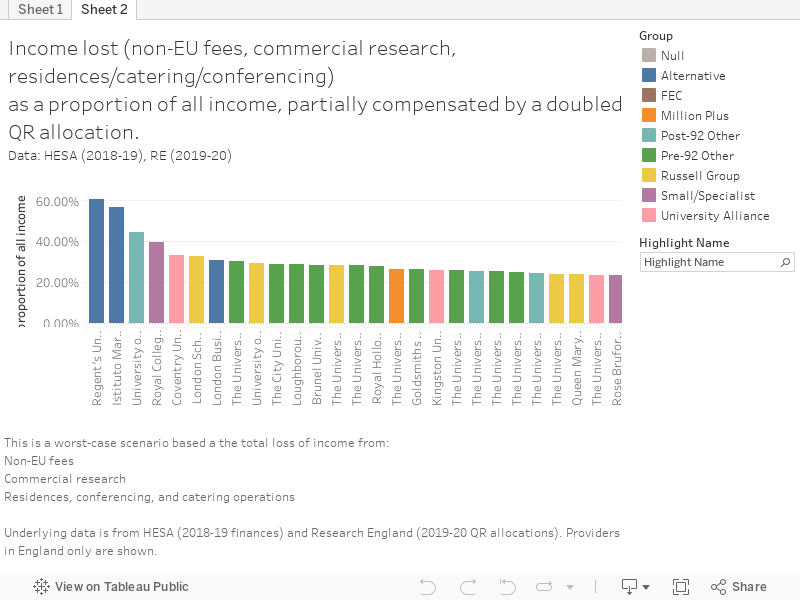

Universities UK has called for a one year doubling of QR funding. This, by my worst case reckoning, covers the loss of commercial research income for most providers – but it makes little impact on the other two.

My worst case scenario assumes losses to the equivalent of a total absence for funds in these three areas. Just to ram home how much of a mess this all is, I’ve plotted the difference between this new QR income and the combined losses from my three shortfall areas as a proportion of total income that would be lost. Eight institutions stand to lose more than 30 per cent of annual income under this scenario.

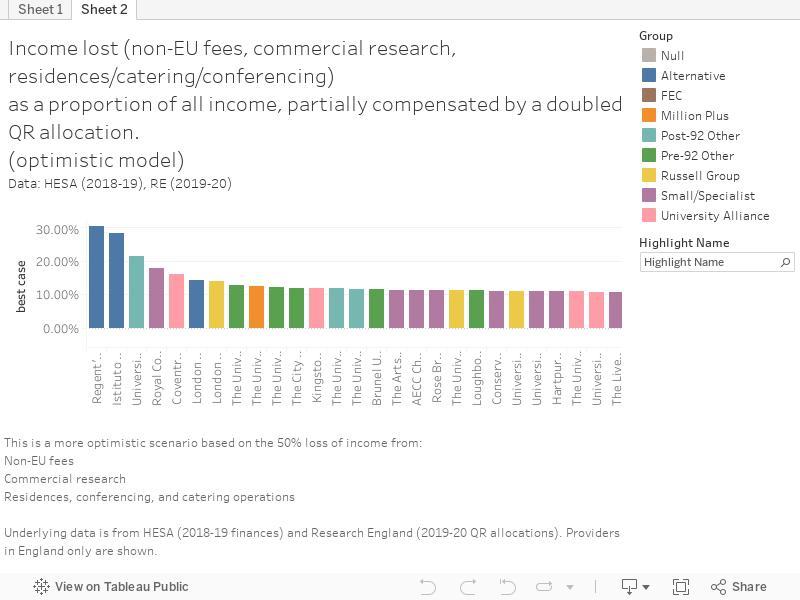

You may think my scenario is pessimistic. I’ve also looked at a situation where only half of income from each of commercial research, non EU fees, and residences/conferencing/catering is lost – perhaps showing an early global release from lockdown and the OBR’s “v-shaped” recovery. Here, losses are between 5 and 15 per cent of institutional income – still enough to require serious changes to the old normal. This graph shows the percentage of all income lost after the additional QR is applied – eight providers even manage to turn a small profit.

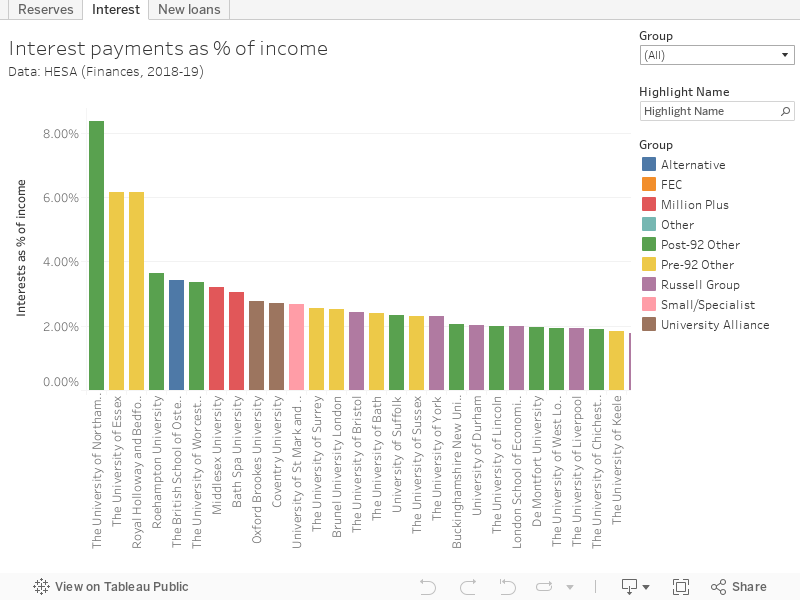

Other money

For some, the crunch will be partially mitigated by the emergency use of institutional reserves. But others struggle with high interest payments on loans – payments that must be made before any other spending can take place due to the risk of default and foreclosure.

Around the sector very difficult choices will need to be made to ensure continued viability. There are other potential bailout income streams in the UUK proposals (as I explored on Wonkhe last week). None would be at the scale of the QR allocation modelled above, though each has the potential to be profiled to offer maximum utility. Here, things like the reprofiling of SLC income and OfS grants will offer a short term solution to the non-appearance of international fees and accommodation income. But they would only move the problem backwards.

The other elements of the scheme are either very selective (full economic costs on UKRI projects only really make a difference for providers that see a substantial amount of income from these sources, small and specialist providers are tightly defined) or very loosely defined (just what will more support for knowledge exchange actually mean in cash terms? Which providers do have a “distinct mission” to recruit overseas students?).

We also need to do more to understand the availability of external finance for providers next year, in terms of existing and new borrowing. The last few years have seen an enormous willingness to lend to universities – will this continue? The other possibility is the strategic use of the government’s furlough scheme – already, several providers have staff on three-week rotation and the reality is that this will intensify over a busier-than-usual summer.

What’s not in the bailout is the sheer volume of financial measures that can support the whole English sector as it currently stands. If things start looking bad, the sector needs to start thinking about a much bigger injection of funds, and what the trade-offs would be to that.

[…] on the theme of a new normal in Higher Education. Some are less than idealistic and see brutal economic realities carving a fundamental restructuring of the sector, other imagine new forms of leadership in HE, […]