The idea of a 2020 recruitment cap has attracted a lot of commentary, most notably from those ideologically committed to a recruitment process driven by market forces – who like to argue for “student choice”.

A cap represents a left-field return to an older higher education policy making, which has wrong-footed much of the sector. I admit this is difficult – so I’m going to start from a position where we agree that we like student choice and take it from there. To be clear, I am not entirely convinced that the market (in the form of the aggregated choices of 18 year olds) is the best way to plan a system of higher education – allow me the fun of playing devil’s advocate to myself.

I said earlier this week that I’d look for two things in a bailout:

- It preserves sector capacity and quality

- It preserves student choice

A right to choose what?

By student choice I mean that students should have the opportunity (given their own level 3 attainment) to study a given subject at a similar number of providers and locations in the years to come. Someone contemplating sociology, for example, should be able to study at a local provider in the same way as they could had 2020 been Covid-19 free.

Of course, these goals are not perfectly achievable even in a regular year. Providers do open, close, expand, and contract courses, and resources are not always allocated appropriately. But I think I can set a goal that benefits students and measure the potential for other proposals to meet this goal.

From this demand-side initial framing, we move quickly to supply-side issues. To provide the same (or similar) courses at the same (or higher) quality, we need to have the same (or similar) number of academic and support staff, the same number of books in the library, seats in the lecture theatre, and so forth. And all this comes as a cost.

It’s from this situation that we understand what should be the true purpose of the bail-out: the preservation of the sector. You may argue that the actions of the market dictates that less popular providers should wither away, but I would counter that this should happen because of the actions of the market, not externalities.

You don’t think the sector should be preserved as it is? You are denying students the choice that they should have had. What gives you that right? If you think the sector should be posher/older/more privately funded, if you privilege the preservation of some providers or courses rather than others, you are disadvantaging prospective students. You might think that students should be studying (say) creative arts, or that public funds should not be supporting the study of creative arts, but to do so is to be against the will of a market-driven demand for such courses.

Mitigating measures

So let’s look at what is on offer as regards a recruitment cap, and whether it meets our newly expressed free market goals.

Institutions in England and Wales in 2020-21 would be able to recruit UK and EU-domiciled undergraduate students up to the sum of the 2020-2021 total forecast for UK and EU-domiciled full-time undergraduate students (plus 5% of the intake), submitted to the Office for Students (OfS) and HEFCW.

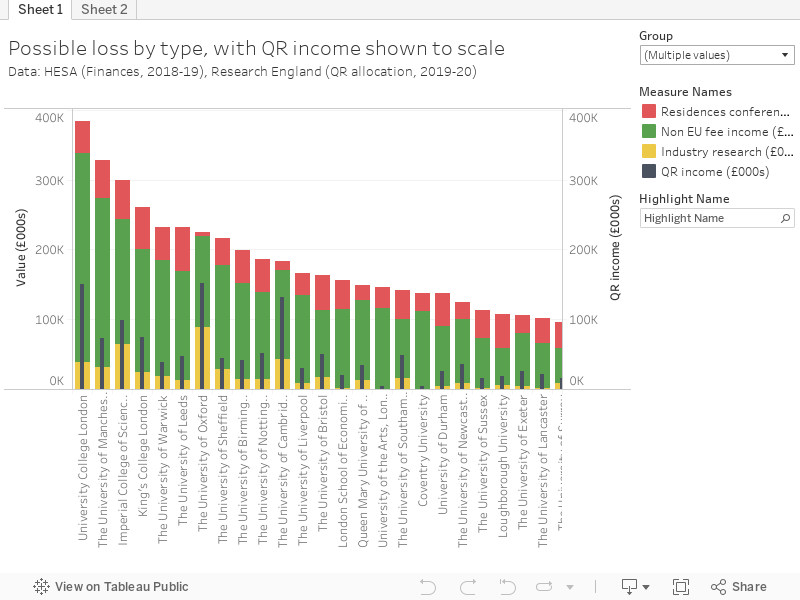

The important thing to remember is that, as we have seen, international undergraduate recruitment income isn’t a game changer. In a few places – mostly Russell Group-y places – we’re edging towards a third of each year’s undergraduate intake. Our problem is the overall financial impact, including accommodation income (as we saw above) and non-undergraduate fees.

This visualisation (based on HESES tables 1-3 from OfS) shows the number of overseas students – in red – entering mainstream postgraduate taught courses in 2019-20, by provider. International students are a huge part of post-graduate provision – and with fees usually higher per year than undergraduate courses, would represent a greater loss to provider income. As yet there has been no suggestion of any measures to deal with a failure to recruit to post-graduate courses – an eventuality that would also have implications for research activities (both indirectly via departmental sustainability, and directly via PGR recruitment) and undergraduate teaching (again indirectly, and directly via the capacity of PG students to teach undergraduates).

How the cap could work

If you use the rather over-optimistic method we tried last week (based roughly on what has been published about provider recruitment targets by OfS – the precise targets are commercially sensitive, I am told), this results in around 50,000 “extra” UCAS places in non-FEC (I’m assuming FECs will be part of a different, simpler, bailout) English HE over 2019 recruitment.

Demographically, we have the smallest pool of UK 18 year olds in recent years – though the number of accepted applicants rose by 1.5 per cent in the 2019 recruitment cycle. Even if we assume that this 1.5 per cent year on year overall growth repeats we still have enough space (ignoring FEC recruitment) before we hit the cap in most places. That is a lot of headroom – I’m sure the model is overstating the exact amount. But the principle remains.

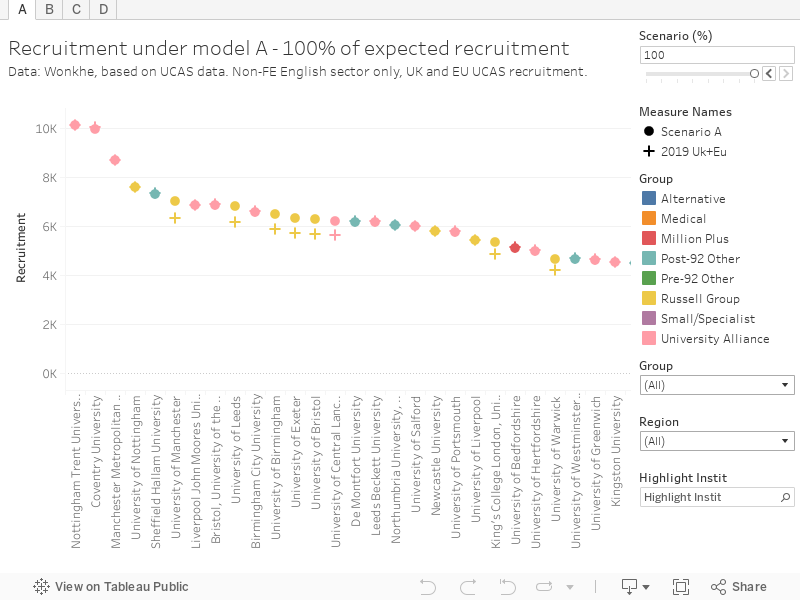

So how will all this extra space play out? I’ve come up with four indicative models. All of these involve only English non-FEC providers that recruited via UCAS last year. I’ve assumed last year’s accepted student numbers for these providers (as a proxy for suitable UK and EU domiciled applicants) rises by 1.5 per cent – giving me a total intake of 408,776 as my 100 per cent scenario. But I (and nearly everyone else) think this will go down, so you’ve other scenarios on the top right slider for each model taking you right down to 60 per cent. Note that these are all indicative – I’m using public data rounded to the nearest 5.

Model A: recruitment changes correlate with tariff band

I’ve assigned tariff bands by ranking all UK HE providers for which I have the data by their median tariff point band, and then assigning each third (approximately) to a band. I’ve assumed that high tariff providers recruit up to the cap, medium tariff providers recruit up 2019 numbers, and the remaining students are shared out pro-rata according to the size of last year’s intake.

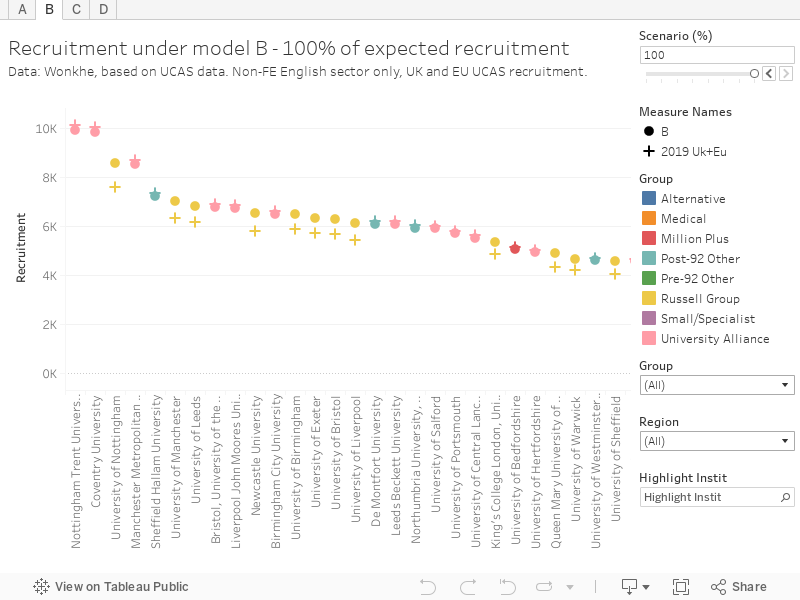

Model B: recruitment changes correlate with mission group

Here I’m assuming that the Russell Group recruits to the cap, other post-92 and small/specialist providers recruit to 2019 numbers, and the remaining students are shared out pro-rata according to the size of last year’s intake.

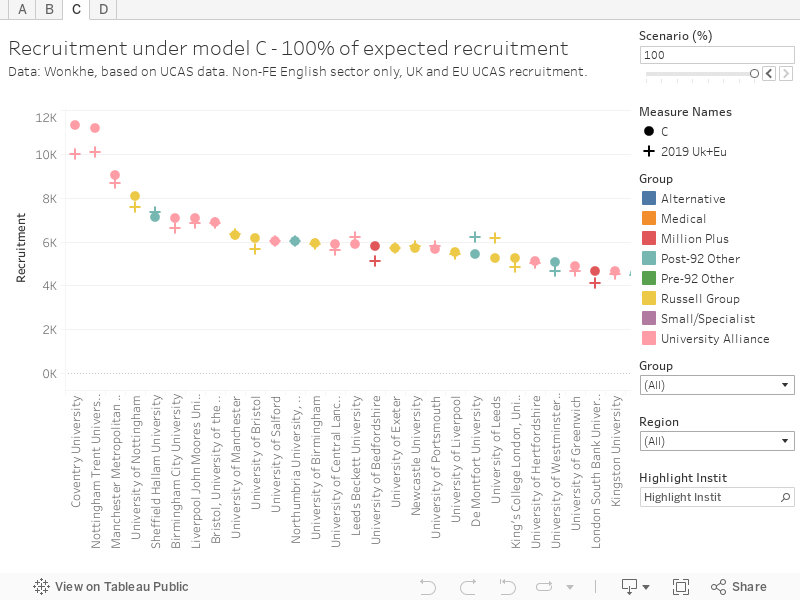

Model C: growth and shrinkage continue

Here I assume that growth or shrinkage in recruitment between 2019 and 2020 cycles will be the same as between 2018 and 2019 cycles. Because there were some outliers, I’ve scaled this so no provider can grow to greater than its (forecast plus 5 per cent) cap, and remaining students are shared out pro-rata to the cap limit.

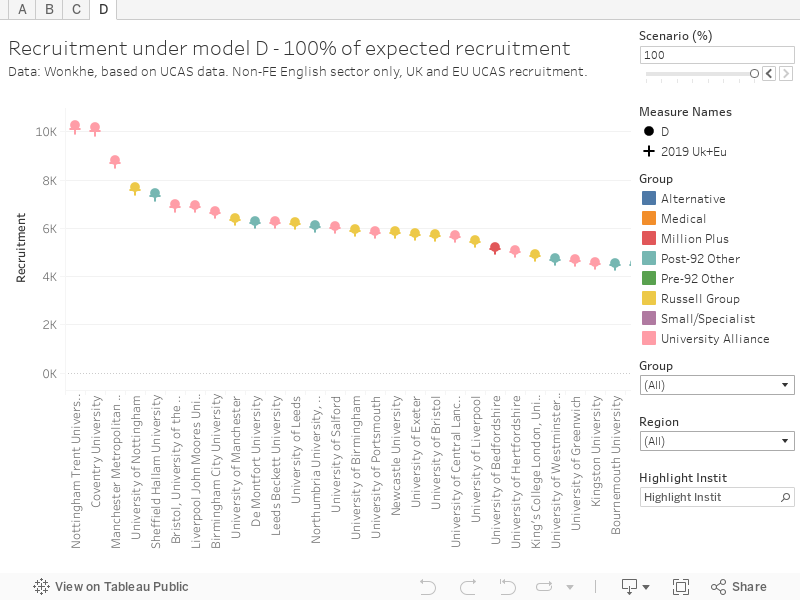

Model D: bigger is better

All students are shared out pro-rata according to the size of last year’s intake.

On the dashboard

For each model, as the total pool of recruitable students goes down, the impact of the assumptions I’ve made in each case becomes starker. And the pool will go down – whether prospective students elect not to apply to help their family or community, or to get the full on campus experience (rather than starting with an online proxy) in 2021. The fall in EU students – reluctant to travel, spooked by gung-ho commitment to Brexit at all costs – also needs to be taken into account.

In reality – all four of these ideas will have an impact on the minds of applicants. As will many more. There may be a difference by subject – will the “hero” subjects (medicine and related, education) see an increase in interest, will business related subjects hold interest for young entrepreneurs who may just want to get started and make a difference. There will be a difference by background – some students can afford to defer, some can’t afford to go.

Given the complexity of this multivariate model, prediction becomes almost impossible. Providers will sit, and wait, and hope. There will be a herd effect – as recruitment teams spot what others are doing, and pile in. Specialist consultancies will make a lot of money.

The question we need to be asking ourselves is: in the name of “student choice” do we want to preserve the current sector or preserve the market? We may only get to choose one.

[…] The incumbent conservatives in Australia and the UK prefer to limit higher education to students and programs they deem worthy. They have reimposed enrolment caps in Australia and the UK. […]

[…] The incumbent conservatives in Australia and the UK prefer to limit higher education to students and programs they deem worthy. They have reimposed enrollment caps in Australia and the UK. […]

[…] The incumbent conservatives in Australia and the UK prefer to limit higher education to students and programs they deem worthy. They have reimposed enrollment caps in Australia and the UK. […]