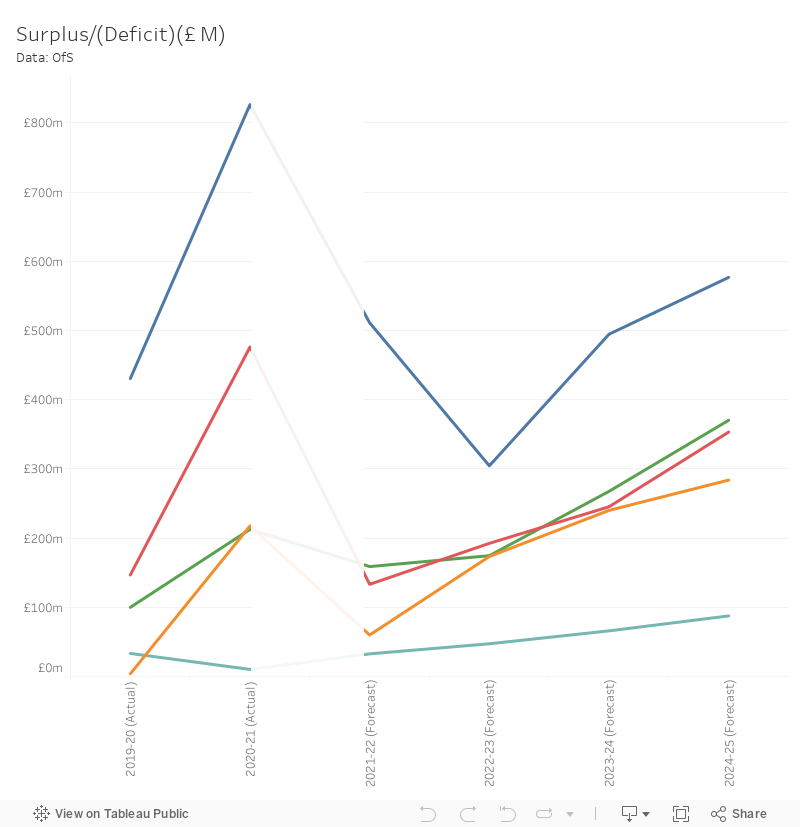

On the face of it, you could argue that a severe cut to operating surpluses would be an optimistic outcome for OfS registered higher education providers over the next few years.

The rise in the costs of living puts pressure on the costs of doing business (everything from materials to salaries), while the real terms freeze in fee income means less spending power overall. Providers are looking on the optimistic side (especially regarding recruitment) but plausibly upbeat averages conceal a huge variety of financial risks.

The headlines

Today’s data doesn’t offer us a by provider position – but we do get a split by tariff groups (you can find out where your provider might sit here). Here’s a straightforward look at operating surplus forecasts.

You’ll note that the dip is longer and deeper for non-specialist high tariff providers – and OfS tells us that these projections do not include the pensions adjustments. Expenditure on every measure is set to rise sharply.

Elsewhere income will also rise in most cases, but not quickly enough or far enough to cover escalating costs. Funding body grants (including funding from OfS and Research England) are a notable exception – these are projected to fall based, as we will see, on a mixture of provider and government decisions.

And all this has consequences for institutional financial stability – net liquidity days will plummet from an average of 173 during 2020-21 down to 104 in 2024-25 for high tariff providers. We should note that liquidity was particularly high during the pandemic, due – in part at least – due to uncertainty over government support for the sector. The unwinding of these positions will release funds for use elsewhere, but will leave less for use during any future crisis.

When ministers brag painfully about a “world class” higher education system I’m afraid this is usually the slice of the sector they are thinking about. This slice of the sector is in trouble.

Recruitment changes

Every time OfS releases data on projections we get a warning about overoptimism on recruitment – this year OfS couch it in terms of the cost of living:

The rising cost of living could have consequences for student recruitment and retention.

Potential applicants, current students and their families could take the view that that attending higher education is less affordable

Though application data shows strong demand for the moment, the regulator notes that behaviour could change quickly. But the other end of the argument is on the availability of places, and there we see another surprise from high tariff providers.

Forecast numbers for UK students in high tariff providers will remain broadly stable each year from 2022 onwards. This year, already seen as the most difficult in recent memory for students seeking places at this group of universities, is in fact the last year where any kind of meaningful growth is anticipated. Recruitment will grow by just 3,000 the year after that, and in 2024-25 will fall by around 500 – in the face of continued demographic growth this will develop into a far more serious issue.

Growth at low and medium tariff providers will push the total size of UK undergraduate recruitment up to nearly 1,700,000 in the 2025 UCAS cycle, but here the risk is one of affordability.

In contrast – all groups of providers are forecasting substantial growth in international recruitment with both FTE and fee income expected to rise sharply over the period. The stagnation of the unit of resource, coupled with high inflation, has weighted the balance even more heavily in the international direction.

OfS is clearly concerned:

The sector, and some providers in particular, continue to be reliant on recruitment of students from China. Any event that reduces the flow of such students to the UK is likely to have a significant impact

The regulator notes in passing that there was no growth in recruitment from China in the 2021 cycle.

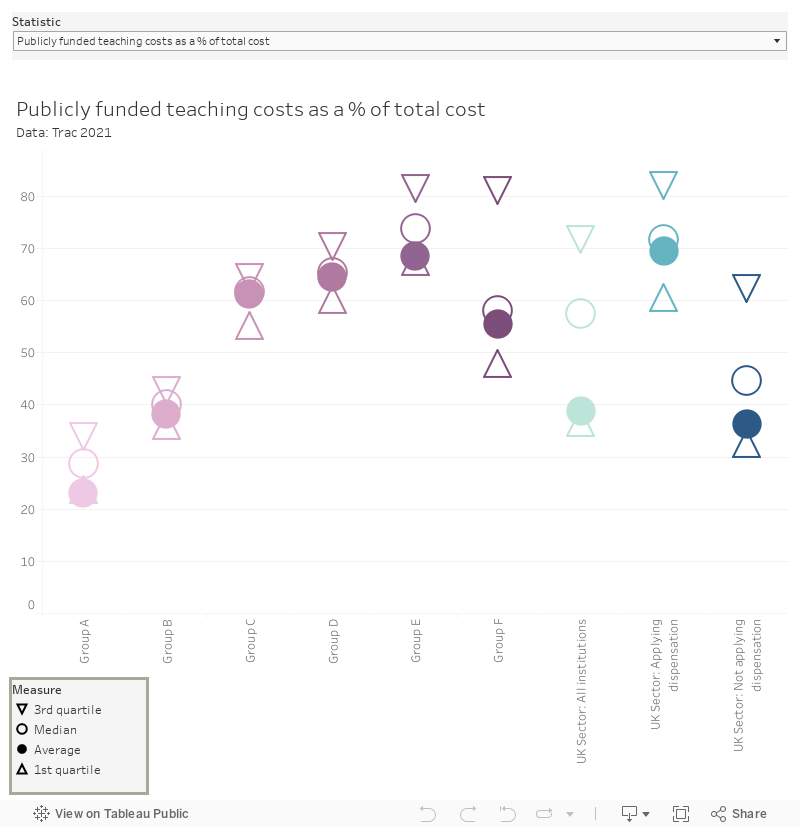

TRAC: covering costs and managing sustainability

With all this data available, it would be easy to miss the (slightly delayed) release of TRAC data for 2020-21. We learn that the full economic costs of all activities in year increased by 1.1 per cent – this was, of course, before the current inflationary spike but does include the impact of Covid.

We get the usual splits by TRAC peer groups (again, find out where you are and how these compare to other measures here) which let us see the proportional importance of teaching costs among newer and specialist providers, and the proportional importance or research costs in groups A and B (as you would expect, the research focused end of the sector.

Fascinatingly, research intensive providers were also more likely to cover full economic costs overall – despite the long documented shortfall in research FEC it seems that teaching shortfalls (though these actually improved over the previous financial year) are increasingly becoming an issue. Group D – broadly providers with a “university alliance” feel about them get the worst of both worlds here.

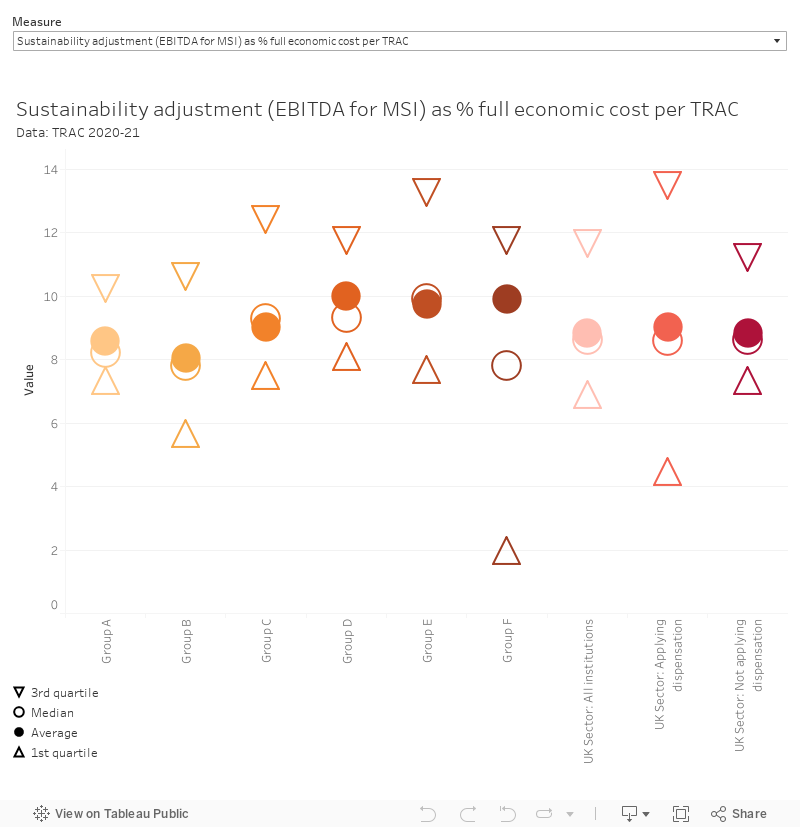

If you think back to the debates around Augar, you may recall the margin for sustainability and investment (or MSI). Here the panel appeared to believe that MSI was a figure plucked from the air, rather than standard government accounting practice for assessing contingencies in full economic costing. Augar expressed disbelief that MSI should be as high as 10 per cent – the TRAC data for 2020-21 shows that it was indeed around nine per cent during a period that pretty much defines contingency.

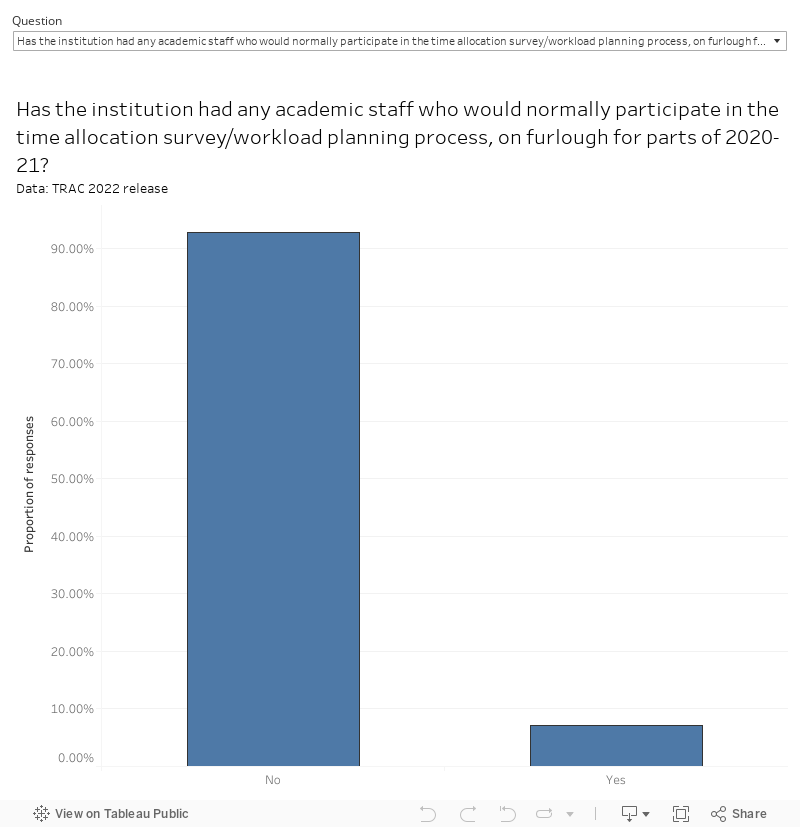

Bonus chart

A set of questions on provider responses to Covid-19 finds that just 11 providers (7.1 per cent) reported that academic staff that would usually be counted in track were furloughed during the main pandemic restrictions.

If growth needs to come to the HE sector as the number of qualified students swells over the next few years, there will need to be investment in facilities to cope. The OfS capital round offers large providers a guaranteed £50k to help with that.