There are higher education providers on the Office for Students register that have never received fee income before – and there are several that received fee income last year that are not on the register.

The whole idea of the new English regulatory system was to bring new providers into the HE system, to grow choice and competition. But as well as market entry, we are seeing a fair amount of market exit.

So far the only view we’ve had of this is via the OfS’ own updates to the register. We know which institutions have made it on to the register, but we only have a partial glimpse of the providers that have either chosen not to register or have refused registration. Thanks to new data from the Student Loans Company, we can take a closer look.

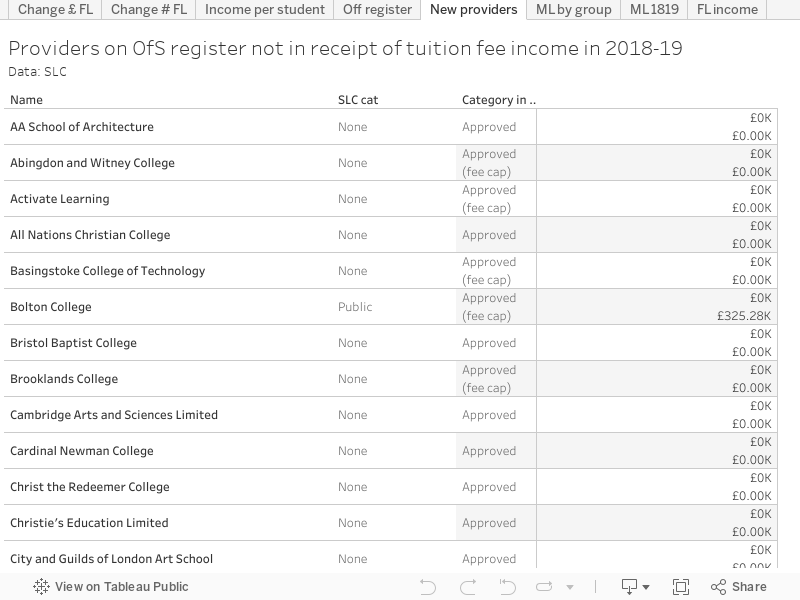

New entries

To start with, there are 52 providers new to fee loan income.

Largely made up of further education colleges and alternative providers, both groups may have been delivering HE in an agreement with another provider. None have university title, and three have degree awarding powers of some sort.

The big surprise – to OfS and DfE at least – is how few of them there are. In February of this year a revised impact assessment predicted 10 less alternative providers and 40 less FECs than the initial prediction in July 2018. At that point the prediction was for 508 providers on the (Approved, or Approved (Fee Cap) parts of the) OfS register, in February 2019 it was 464 – but by November 2019, long after the start of term, OfS have registered only 388 HE providers.

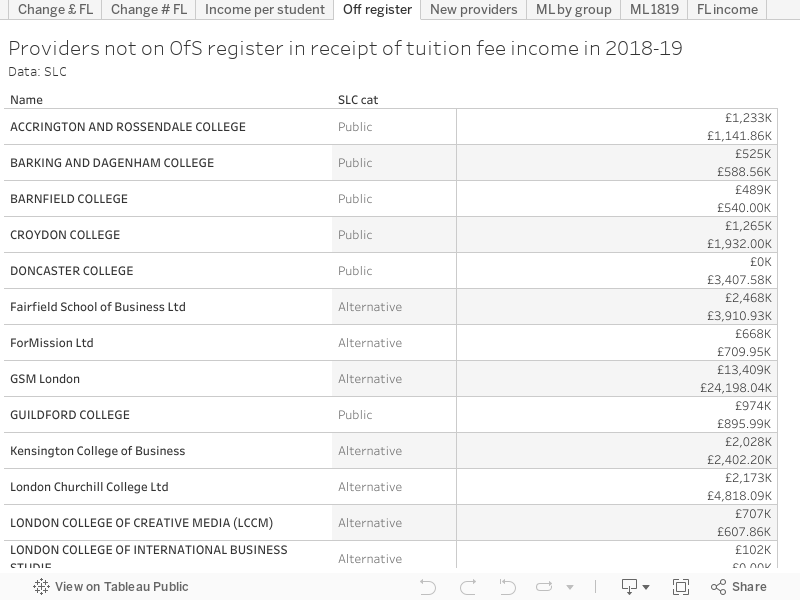

Bye-Byron

There are 23 providers (not including school centred initial teacher training provision, which is regulated outside of OfS) that received fee income in 2018-19 that are not on the OfS register.

We know about 8 providers that have been refused registration for reasons related to regulatory decisions – two of whom appear on this list. In this case some agreements may have been made to continue to support students to complete their course. Some will be related to decisions we don’t yet know about (perhaps for legal reasons). Other list entries relate to providers that have merged or changed names. But for more than a handful, this looks to have been an active decision not to participate in OfS’ system of regulation despite having been regulated by HEFCE. Again, there is nothing in any government impact assessment suggesting this may happen.

A smaller-than-expected sector means a failure in DfE policy making and OfS implementation. Registered providers are paying more than is expected on mandatory registrations to OfS, and the registration system is proving complex and difficult to negotiate. And, most damningly of all, the legions of high quality alternative providers seeking to disrupt the market – the “Byron Burgers” in Jo Johnson’s once again apt metaphor – simply do not appear to exist.

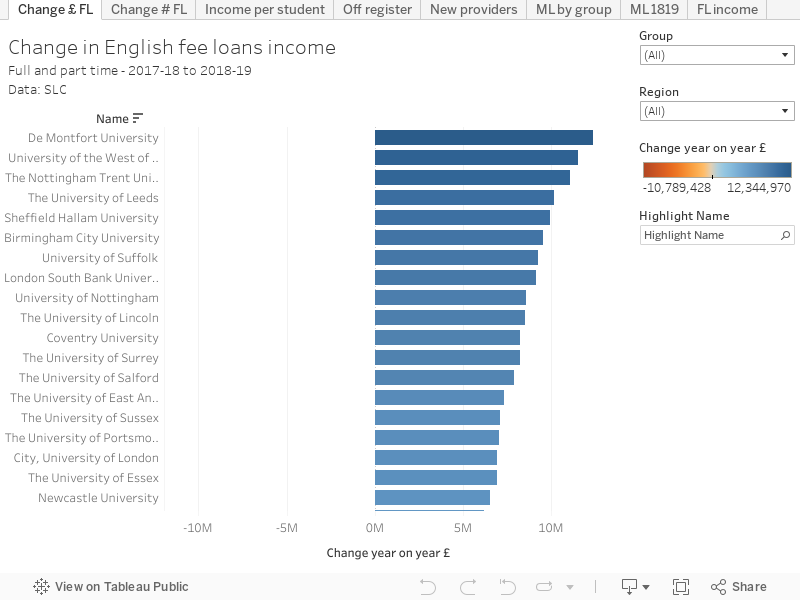

Fee income

Student Loans Company data, now published on gov.uk, is one of the sector’s least explored data sets – for that reason I’ve developed a range of other visualisations that can help you investigate tuition fee income, and student maintenance loan take up, for a range of institutions.

It’s not perfect – some very small providers don’t get their own data (you have to be recruiting more than 50 students to avoid being included in an “other institutions” agglomeration – some of our 52 new providers may be hidden there). There’s data for 2017-18 and 2018-19 academic years for each provider within the supplementary tables.

I’ve plotted data on changes in numbers of students accessing fee loans and the amount of fee income arising. There’s a look at maintenance loans numbers and income by provider and by group (interesting that income fell between 2017-18 and 2018-19 for alternative providers), and a rough calculation of income per student which probably shows the prevalence of part time students.

The data refers to a combination of English domiciled students and EU students participating via the English system. You can dis-aggregate this but for an overall look it made sense to combine it.

What I’ve not looked at yet is post-graduate loans, disability loans, and income from the Welsh and Northern Irish systems – all of which felt like very separate issues that needed a proper examination.

The other main headlines

The release comes with a handy summary, which looks at overall trends in the sector.

We learn that the SLC paid out £17.1bn to students and the sector this year – with the biggest growth related to FT first degree maintenance loans, as a similar number of students are taking out of this support. The average amount of maintenance loan paid out per student has risen by 10%.

There has been a decrease in the amount paid out to part-time students – though numbers have remained similar. The new(ish) postgraduate loans have largely stabilized in their second year of availability.

Also out on the same day was a publication called “UK Education and Training Statistics 2019”. This spans all education sectors in all nations – and we learn such fascinating things as the fact there were 143 universities, 20 other HE providers, and 336 FE colleges in the UK in 2017-18, along with sundry other restatements of HESA data.

Interesting, and even the 52 may be a slight over-estimate of ‘new’, as at least some were already able to access loans in principle even if they had not accessed loans previously or in the last year (e.g. Bristol Baptist College appear to have had successful QAA Reviews for REO 2012-2018 – https://www.qaa.ac.uk/docs/qaa/reports/bristol-baptist-college-reo-12.pdf?sfvrsn=5ab6f581_4 ; https://www.bristol-baptist.ac.uk/qaa-review/).

Agree with Andy’s comment. There are few on the list which will be on the register now for tier four purposes or PG loans but wouldn’t have had tuition fee income, e.g. Christie’s Education. Quite a few on the new list also seem to be providers that have had franchised provision in the past and wouldn’t have needed course designation directly. Why they are registering isn’t clear, unlikely they are all moving to validation relationships.

The list of providers off the register is very interesting, as mentioned for some it will be down to mergers (e.g. Barnfields) and others not wanting to go on the register. However you can perhaps hazard a guess at where the unannounced refusal decisions are, along with possible legal action by looking at their websites and seeing who still have pending registration decisions information on them. For example London Churchill.

5 of the 23 providers (eg Barnfield, Doncaster, Northumberland etc) who received tuition fee income in 2018-9 but who aren’t on the register are FE colleges who have merged with a college that is on the register.