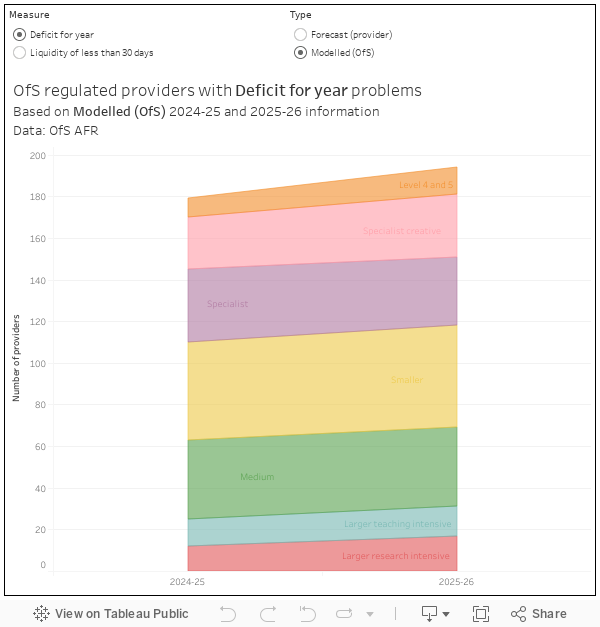

New Office for Students financial modelling suggests that 194 English higher education providers will be reporting a deficit for 2025-26, with 108 projected to have less than 30 days of net liquidity.

This is the main finding of the second ever in-year recalibration of OfS’ assessment of the financial sustainability of providers that it regulates. Chief Executive Susan Lapworth cautions:

Many universities have already taken steps to secure their long-term sustainability. For those that have not, the time to do so is now. That is increasingly likely to involve bold and transformative action to reshape institutions for the future – while continuing to deliver for the students of today and tomorrow.

This work will support the Office for Students in working with the sector to address financial problems as they become apparent – OfS has already devoted substantial internal resources to provider financial monitoring (including staff from teams more used to supporting TEF and freedom of speech) alongside using an additional DfE allocation to buy in consultancy.

Knowing what we know

There’s no new data from providers here. The projections published in May 2024 have been updated in the light of 2024 cycle home undergraduate recruitment, using Home Office visa data (up to July 2024) and confirmation of acceptance of studies (CAS) data for the 2023-24 academic year (published in June 2024). It does build in the top-level implications of the increase in undergraduate fees (at £371m) from 2025-26, and the increase to employer National Insurance contributions (at £430m each year from 2025-26, and £133m this year).

There’s also a couple of eyebrow-raising assumptions in the model too – OfS (who, for the avoidance of doubt, is the body charged with regulating in the interest of taught postgraduate students) has simply assumed no growth in recruitment since 2023-24. It has (again as a body charged with ensuring that regulated providers adhere to consumer law, and enforcer of registration condition C1) assumed that all providers are legally able to increase fees for undergraduate students and have somehow managed to make sweeping savings without breaching promises made to students under consumer law. I mean, it could ask them (I’m assuming here OfS has up-to-date contact details for the providers it regulates).

The lack of up-to-date information is truly striking. OfS will next receive Annual Financial Return data from providers five months and two weeks after the end of each providers financial year. For the majority of larger universities the financial year ends in July, so we should begin to be able to understand the current position around December of next year: the most up to date information the regulator has was submitted late in 2023 based on the 2022-23 financial year. In some cases providers will be subject to “enhanced monitoring” and will provide additional information (including financial data) – as of February 2024 the most this could have been is about one in every 25 registered providers.

Despite providers now having hard data on 2024 recruitment from all sources and all levels – and despite many embarking on strategically significant cost reduction exercises – they have not submitted revised forecasts. There is no formal scope for them to do so (though I would hope those facing serious trouble are already in contact with the regulator regarding their current position).

In 2020, OfS sought a mid-year financial return from providers in the teeth of concerns about the way Covid-19 would play out. It was minimal in scope, but helpful in nature. Why wasn’t this done in 2024, given the obvious financial strain the sector is under? We understand it was considered.

Stable door bolted

To be scrupulously fair, OfS does say:

We are preparing to collect more real-time financial data from providers to increase our ability to understand changes in financial position throughout the year. We consider this development essential in the current financial climate.

It feels almost redundant to point out that OfS was well aware of the financial climate in May 2024 (“an increasingly challenging environment”), May 2023 (“a challenging environment”), May 2022 (“the environment remains challenging”), and May 2021 (“the environment remains challenging”). Perhaps, in the face of such a sustainedly challenging financial environment, steps like these could have been taken earlier.

There are wider questions on the availability of other data – for instance why is there no straightforward way to understand postgraduate recruitment outside of significantly lagged statutory returns? The last OfS Data Strategy was published in 2018 and ran out in 2021 – we are significantly overdue for a new version, and perhaps this retread could consider better and more timely information on provider recruitment at all levels as a key determinant of provider financial sustainability. There would also be scope to build in data sharing agreements with the Home Office – it is genuinely frightening that assumptions are being made based on the same lagged CAS data as mere mortals like us get to see.

If OfS genuinely wants to be a responsive and risk-led regulator it needs timely data. It does not even currently have data that allows it to regulate based on the experiences of students enrolled on courses at providers this year.

Truth is relative

Mind you, if OfS continues to regulate in such a way that providers feel compelled to make submissions as optimistic as possible there may be larger problems at hand.

If you made a submission to OfS that suggested your underlying financial position was perilous you would be at risk of a breach of condition of registration D. If you think that this is an empty threat, bear in mind the University of Buckingham was fined for failing to submit financial data in time (condition F). This is not an environment that is conducive to the sharing of genuine provider concerns.

Provider optimism in recruitment is often characterised as improper planning practice – spun in OfS statements as an unworldly, Panglossian, failure in university character. In practice, a university has a fair idea of costs going forward (and an assumption that cuts to activity were undesirable in a world where the student experience is paramount) and have had to assume recruitment growth to make the numbers add up. A perceived “hostile environment” has led to a world where it has become difficult to talk truth to the regulator. Relationship resets (there have been many) will help eventually, but it is a long and difficult road.

We also have to factor in the burden reduction agenda first placed on OfS during the pandemic. While this has not resulted in any meaningful reduction of regulatory burden, it has made it very difficult for OfS to seek and collect the data it needs in order to successfully regulate in the student interest.

For what it is worth

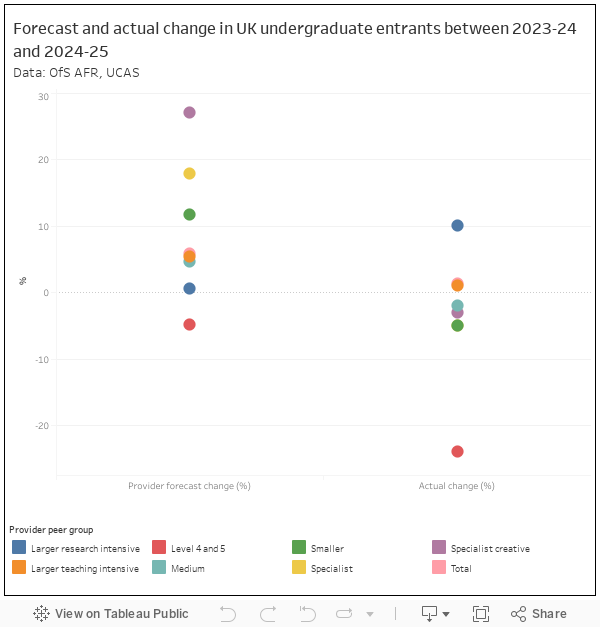

There is just a single scenario presented this time – roughly in line with the most pessimistic of the four presented last time round. Again, there’s nothing at a provider level (god forbid that there was a commercial impact to financial monitoring by a regulator!) but we do get splits based on a variation of the OfS provider groups published in 2022: the ones by size, rather than by financial status, naturally. And as the groups have never been published, I can’t tell you which providers are in which… I suppose it is fun to guess.

You can see everyone other than “larger research intensive” providers overestimated growth in UK undergraduate numbers between 2023-24 and 2024-25 – although the sector grew this intake overall this was primarily due to larger providers, with everyone else seeing a real-terms decline.

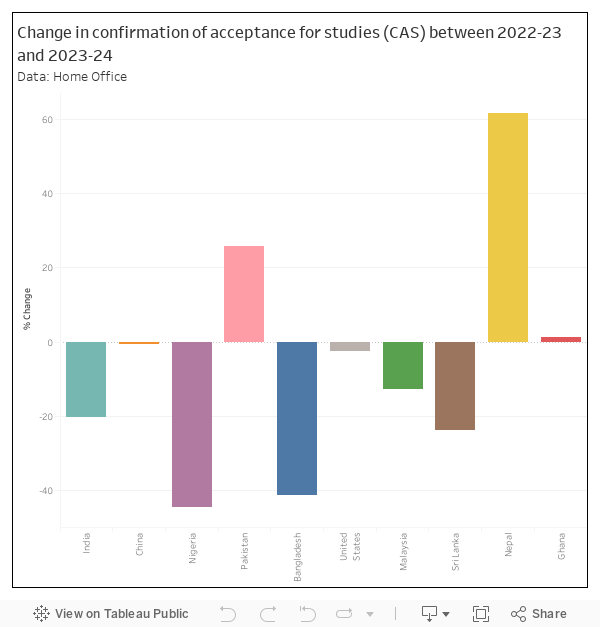

The story is similar (though we don’t get the data here, I have plotted it before) for international undergraduate recruitment – though arguably postgraduate international recruitment has a bigger impact. Because it is clearly beyond the wit of the regulator to have any measure of postgraduate recruitment of any sort we just get an overview of international visa and CAS: here I plot the ten largest countries showing changes between 2022-23 and 2023-24, as if to demonstrate just how long these problems have been visible and how little we appear to know about what is happening right now.

Knit all this together with the various assumptions detailed above and you see the large difference between provider forecasts for 2024-25 finances and what has turned out to be the case (unfortunately OfS did not find space to detail how far of the mark the modelling it presented at the time was).

For me it isn’t a particularly useful forecast: as I’ve been over above the data is either incomplete, lagged or both. On the purely “vibes” level that we seem to think about the sustainability of the sector in regulatory circles it is helpful in that it illustrates that there is a systemic problem rather than a few bad apple providers, and that there will need to be systemic action: regarding which the fee rise is a welcome (if overdue) gesture in the right direction.

That – for governments, regulators, and public alike – we do not have meaningful and timely data on the size, performance, or financial stability of a major piece of economically valuable infrastructure is nothing short of a scandal. We do not have the ability to take targeted regulatory action, we don’t even know whether the (politically) expensive action that has just been taken will have an impact this year. For a publication meant to convince us that OfS has its eye on the ball it does a remarkably good job of illustrating that our regulator is watching on catch-up.

The report focuses on uncertain recruitment. ‘Approved Fee Cap’ providers will be sending in their HESES returns in the next few weeks, so OfS will have a pretty good understanding of student numbers, even if it doesn’t necessarily know about the gap between targets and actuals.

Meanwhile, finance committees have signed off the ‘going concern’ statements in annual accounts ahead of governor/council meetings. It wouldn’t take long for someone to risk assess those…

Presumably if OfS doesn’t undertake that risk assessment of going concern statements (and likely even if they do), it won’t be long before an enterprising journalist/blogger does so.

Even without any actual data to underpin the OfS change in tone – and the report does seem to exist to enable OfS to push for ‘bold, transformative’ change and the idea that local providers needs to stop competing (another success for the market) – it is striking to see the dual impact of fee rises Vs NI changes.

It is very clear that the additional money which the govt has provided, for which it has expanded political capital and for which it requires significant additional work from universities, is unambiguously an overall cut in income, this year and in future years.

Whenever I read about the OfS – and particularly whenever I have to deal with them – I’m consistently struck by how little it actually understands the sector it regulates.

This is perhaps not surprising. If you look at it’s senior team, they are pretty much all people who’ve either been career wonks (at HEFCE etc) or, increasingly commonly, people who have come in from outside, from the civil service or regulators like Ofgem. Very few have actual experience at working in a university, particularly at high levels and / or recently. From looking at a few staff profiles, I suspect this is reflected down it’s ranks.

They could mitigate this by actually listening to the sector, but we all know how that’s gone.

In a similar vein, I’m struck by the lack of competent business managers at a University. Universities need competent management, not people who have written some great academic tomes that few will engage with raising to the top on that basis. Increasing overseas student number targets in the face of significantly declining applications with no other mitigations? Madness. We need managers who understand larger businesses in charge.

Be careful what you wish for, too many failed in the ‘Real World™’ management people end up finding a safe berth in Universities and end up doing similar damage there too…

The University I’m about to retire from, due to such managers appointed by the business people on council selling off the parking to the ‘for profit’ enforcement sharks and that companies demands for absolute access to our bank accounts, all done without consultation with the Trades Unions as it is a change in employee terms and conditions, has suffered badly from ‘professional’ managers and managerialism. Much of which comes from University business school trained people, I saw similar damage done to IBM by Harvard Business School graduates, but as I’m old and part of the ‘corporate memory’ they’re probably be glad to be rid of me…

Two distinct issues here – the information & capability of the OfS to regulate (and intervene) in HEIs, and then the underlying financial performance of those HEIs. As the author states, the forecasting process is inherently biased towards optimism. But lets not forget the other control – the statutory fiduciary responsibilities of the directors/governing body. Unwarranted optimism isn’t sustainable (as we are seeing) and at some point those directors have to take responsibility (and action) irrespective of whatever fantasy number was submitted to the OfS. If Governing Bodies are signing off these budgets, and then not achieving them, they have to accept responsibility for that. Once that starts really happening (and I am sure it is in a number of struggling institutions) then management and regulators will have to start talking more realistically to each other … or we get an institutional failure and everyone asking each other why didn’t we see it coming.