So, way back in December 2021 I had a crack at thinking about the way we classify higher education providers.

It was, for me at least, a fascinating and humbling experience. I had conversations with all kind of people as a result, and it helped clarify my thinking about providers.

Clearly mission groups, although they do a lot of great work, are not the best way to split the sector up into collections of similar providers. We do talk about groups of providers all the time – how often, for instance, do you mention “the Russell Group” as if a self-selecting group of 24 providers had anything more in common than their decision to keep paying subscriptions.

The trouble is, there’s not really an alternative approach.

I wonder where they got the idea from

My previous attempt used a variety of axes – scale, finances, recruitment patterns, regulatory conditions – to draw together similar providers. I ended up with eleven groups – the source of the “colours” you’ll have seen in data visualisations over the last year.

The reason I bring this up is because OfS has done pretty much the same thing this morning. And although my article was the start of a conversation with the sector, in typical OfS fashion the published ones are the way OfS has decided to classify you with only the potential of OfS reviewing these in three years (though, to be clear, there’s no regulatory implications).

The only way anything like this is going to work in terms of getting people (ministers, applicants) thinking about providers relating to what they actually do is if groupings are adopted by multiple users. The only way to make that happen, I now realise, is to get everyone around the table at the start. And OfS was never going to do that.

Dual-axes action

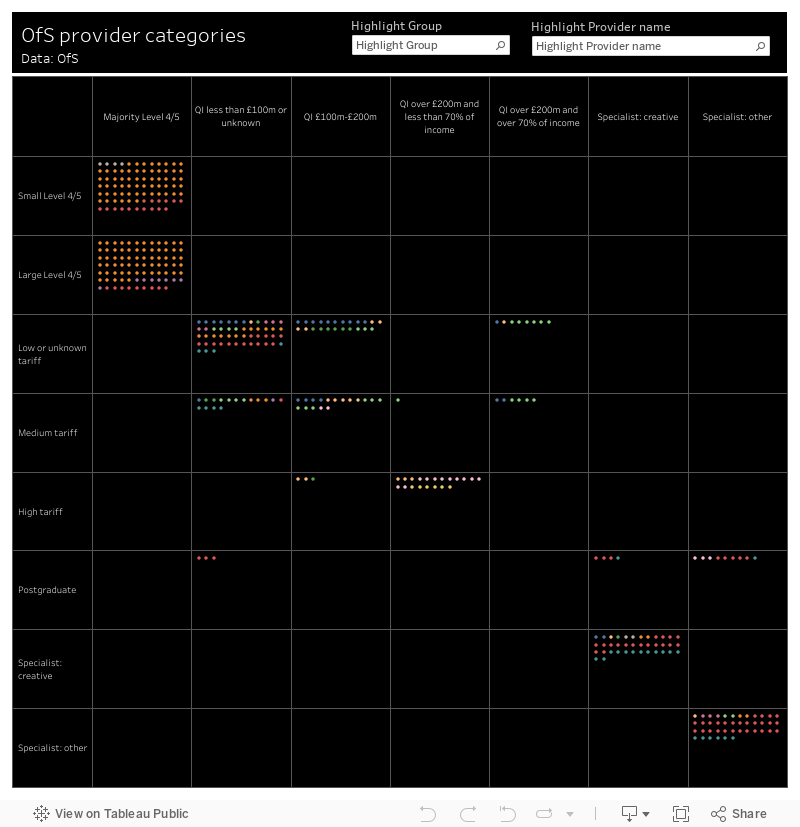

The regulator has actually developed two approaches to grouping providers – one based on finances and one based on the student population. We’ll be seeing the appropriate ones alongside future data releases – so the future iterations of financial sustainability work will use the financial groupings. The methodology uses a similar decision tree approach to the ones I was playing with.

To be scrupulously clear OfS has created two typologies, not one, and intends to use them separately rather than together as I have displayed them here. They will be updated as time passes, so this is just the current mix.

Anyway – let’s have a look at them:

The only thing I think I really need to explain in the (commendably clear) category names is QI, which stands here for “qualifying income” – OfS funding plus fee income (exclusive of VAT) and research contract income (VAT). The colours on the chart show my groupings from 2021, and you can highlight a mission group or provider of interest at the top.

Funny, that

Having done exercises like this myself, the first anomaly that sticks out is how OfS has contrived to put the whole Russell Group in a single box. The fudge here is that these providers get less of their income from the state proportionally, but still get a hefty amount of income from the state. Quite how this makes Oxford (with its massive overall income) comparable with Warwick (a great university but not anywhere near the financial scale of Oxford) I am not sure.

I’m generally intrigued by some of the groupings within boxes – for instance: what connects the Inns of Court, Dartington Hall, and Thinkspace? Well, they’re all of the non-specialist postgraduate-only providers – which is grand, apart from Thinkspace focusing entirely on musical composition for media, Dartington covering solely the arts and ecology, and the Inns of Court being the actual Inns of Court (which is kind of a law thing). Yet Cranfield – the closest thing we have to a large generalist postgraduate only provider – is seen as “specialist”?

What are we trying to do here?

But the big thing that worries me is this. OfS has aimed to satisfy three fundamental need states in creating these categorisations:

- Providers within a group should respond in the same way to regulatory changes

- Groups are neither small enough for a provider to dominate, or large enough to lose homogeneity

- It should be easy to describe the groups to “expert users”

When I had a crack at this I used an idea of barriers to action – what regulatory decisions acted as constraints to each kind of provider. For instance – cutting the higher level fee cap would hurt Approved (Fee Cap) providers, but not Approved (or unregistered) providers. Cutting the amount of money going to arts courses would hurt all arts providers, but would hurt those without degree awarding powers who could not easily spin up new courses more.

FE colleges, as we now know, are in the public sector – meaning DfE has more power over what they can do (for example, regarding compliance to Local Skills Improvement Plans, or controlling borrowing and other management decisions) than OfS does over higher education providers.

The OfS groupings do not really take any of this into account – which seems curious. These are known constraints to provider activity, so will each have an impact if regulation makes or demands changes. And “experts” already know about these things, not least because OfS thinks they are important enough to put on the register.

Testing the categorisations

A few other omissions for me: which providers would suffer should entry qualifications based student number controls, or controls on foundation year fees, be imposed? Which providers would struggle against a cap on international recruitment? Which providers have access to funding for “world class” small and specialist provision? Which providers would benefit from funding aimed at promoting local recruitment from disadvantaged groups?

You can’t really see this from the categories provided. If you wanted to use this as a tool to test policy ideas these are just some of the policy ideas that are literally on the table right now for discussion. And it wouldn’t work in those cases.

But fundamentally, categorisation needs to happen with consent. While I am glad that OfS has been transparent in how this exercise has been carried out – there’s no evidence that it has had any conversations about how the providers involved see themselves or the ways in which they plan to change, and there is no evidence that OfS has considered the ways in which other people would like to use these groupings.

Which, sadly, is par for the course for the regulator.

There is a case for people getting together across the UK to come up with some commonly used categorisations that can help inform the national conversation about higher education. UCAS, HESA, league table compilers – all need to think, on occasion, about “types of provider”. And the only way any of these will take off is if everyone agrees on one approach.

Would be interested to see TRAC and KEF cluster correlation visually (by which I mean – can you add this filter to your Tableau to save me the bother? 🙂

I’ve made you a special sheet (https://public.tableau.com/views/ProvidercategoriesOfS/Sheet3)

Thanks – nowt surprising there!

Worth an FOI to the Office for Students to establish how deliberate having a category which only contains all 20 English Russell Group universities and no other universities was? I would be amazed if there wasn’t some kind of iterative process to get to that outcome…

Well yes! It is remarkable how the top entry tariff boundary is set just below Liverpool’s entry tariff…