The common understanding of the last five years of higher education funding policy in England has been that a drop in the real term value of the undergraduate home student fee loan cap has led to a rise in the recruitment of international and postgraduate students – with these uncapped fees shoring up university finances.

Though the international student end of this equation has been the subject of a great deal of attention as the government balances performative posturing on immigration with a desire for soft power (or a desire not to cover the full cost of a world class university sector if you like) there has been comparatively little attention paid to the plight of postgraduate taught recruitment among home students.

Last time I looked into this, back in 2022, I noted that we were seeing strong PGT growth among home and international students. Two years on, the international boom has largely continued until very recently, but something else has happened to home students.

Running the numbers

The continued absence of 2022-23 HESA Student data means that I’ve had to succumb to the warm embrace of HESES to understand where we are.

I’m looking primarily at “OfS fundable” home domiciled students here: a quick definition – in HESES terms “OfS fundable” refers to the majority of home students, with a handful of important exceptions:

- Initial teacher training and INSET students

- Pre-registration courses in allied health

- Some courses commissioned and funded by an NHS organisation

- Students on closed courses (for example those funded directly by employers)

- Students aiming for an equivalent or lower qualification (ELQ), unless specifically exempt

Within this group I’m looking at PGT (Masters’ loan) and PGT (Other) students, this excludes a small number of fundable home students (c15k) who pay undergraduate fees for PGT courses.

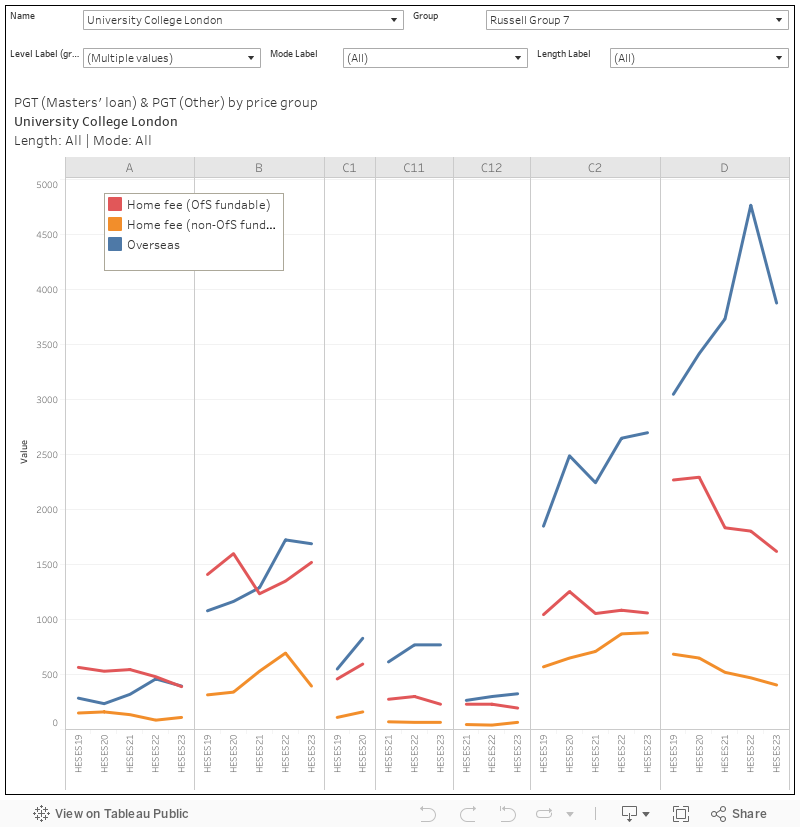

PGT students (headcount) paying home fees have fallen sharply, from over 200,000 in HESES20 to just over 160,000 in 2023. This could be a decline from a pandemic-era boom, or a result of a high number of vacancies within the high-skill end of the job market, but it also represents bad news for provider incomes.

Which providers? By far the largest provider for fundable home PGTs is the University of Law – with only slightly less home PGT students in the HESES23 data than UCL and King’s combined. The biggest proportional drops in fundable home PGTs are among the Cathedrals group and non-aligned post-92s. The only providers growing this market anywhere near the rate they did in 2020-21 are alternative providers, and those in Million Plus.

There’s a subject aspect to this too. The continuing absence of HESA Student 2022-23 data means we can’t be as precise as I might like, but the most notable decline is in the “D” (classroom-based, non-STEM) subjects – and I’d take an educated guess that much of the decline has been in business courses. This still remains a huge category (especially among overseas students) – that MBA option.

You can also view this chart for an individual provider, using the filter.

Finances

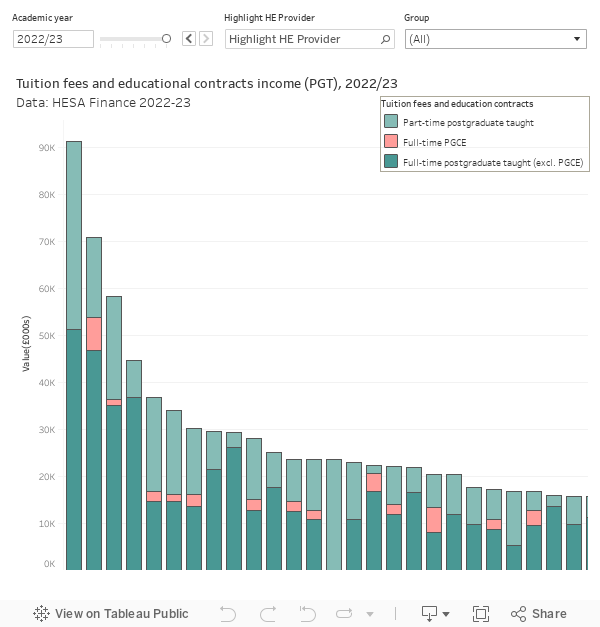

In 2022-23, home PGT fees represented nearly £1.7bn of income for the sector. In contrast to the very visible fall in numbers, the fall in income for full time non-PGCE home fees is around 10 per cent – noticeable, but by some measure mitigated by the ability to raise fees in line with inflation (or above). As a mode of study without a price cap (the nominal maximum £12,167 available loan for postgraduate study hasn’t really had an impact on fees, especially in the more prestige-focused of the sector)

We don’t really talk about a competition for taught postgraduate places, it is in most cases very much the case that if you meet the entry requirements (a decent degree in a relevant field) and can raise the fee you are in – something that surprises those who think in terms of selective universities. Very few universities are selective (in the usually accepted sense of turning down a lot of applicants) postgraduate recruiters.

If you are interested in who is most heavily exposed to the home PGT market, this is easily retrievable from the latest set of HESA Finance data:

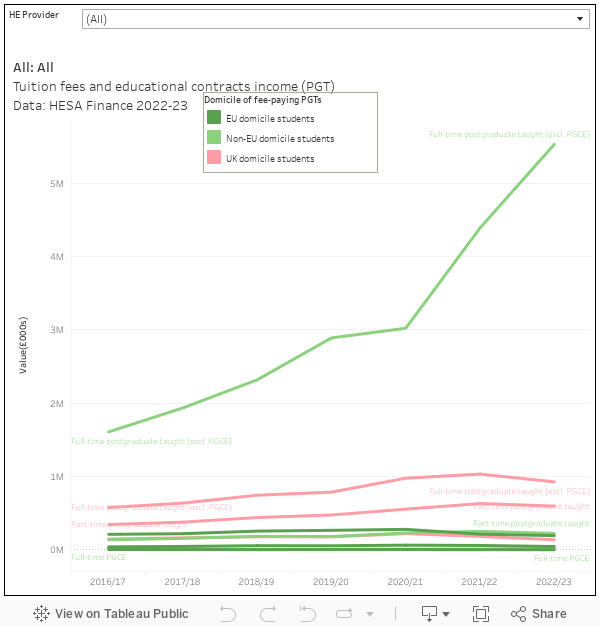

And you’ll find very few providers that have seen anything much better than income stasis over the last year or two when it comes to home PGT income:

And afterwards

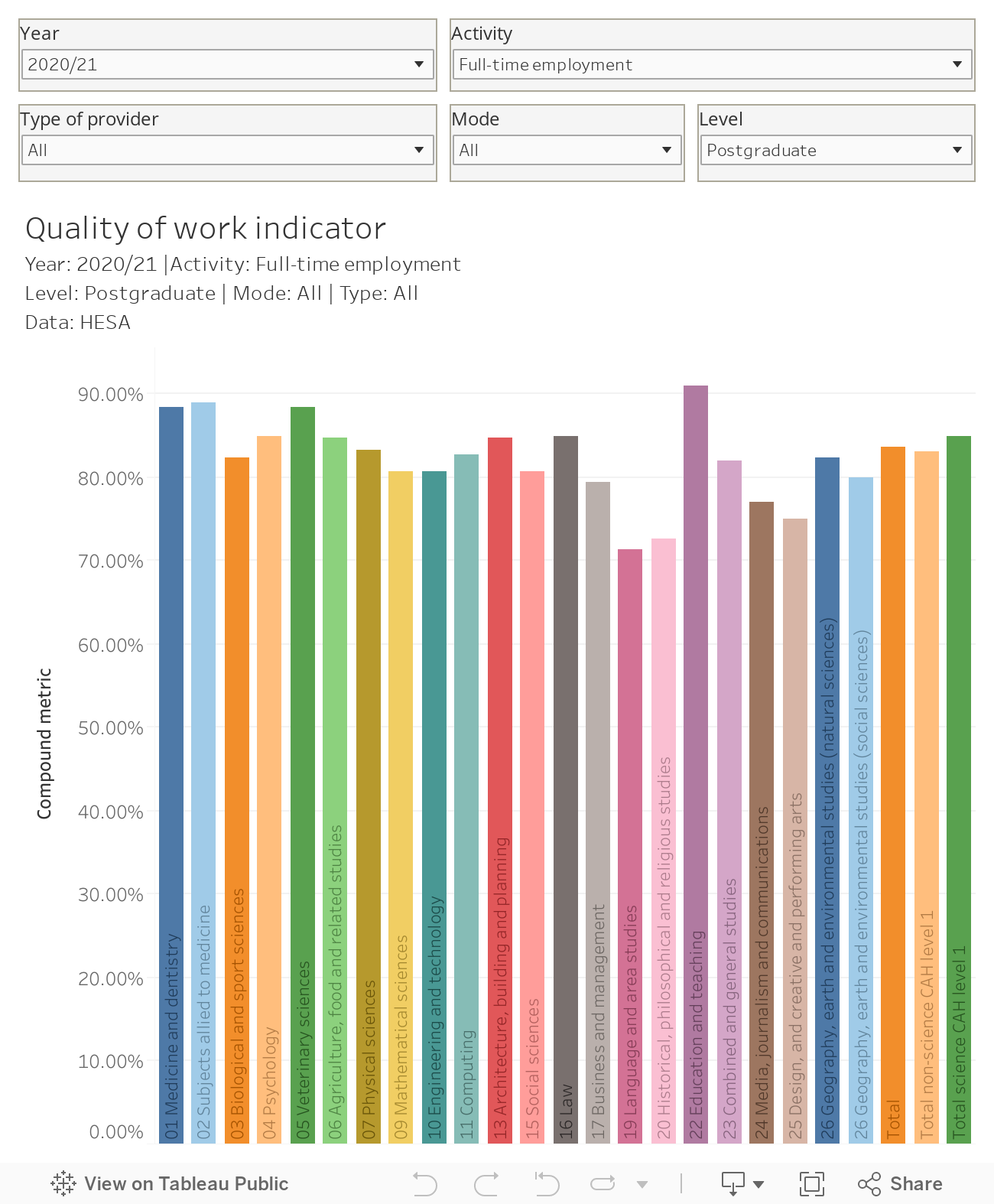

People who have completed a higher degree report a higher quality of work (a compound measure developed at HESA that includes consideration as to whether a graduate finds their work “meaningful”, whether they are using what they have learned in their studies, and whether what they are doing aligns with future plans). This is variable by subject, but offers a better insight into the wider benefits of postgraduate study (salaries or job types don’t really work when so many take postgraduate courses while already in employment).

We also need to think about the reasons someone might take a masters – it can often be for personal growth (or personal interest) rather than an employer or career requirement. This is the kind of study that is more likely to be affected by the wider economic climate – there is a sense in which people do turn to training and education during downturns, but a cost of living crisis can make discretionary spending harder.

Is there more change to come?

With per-capita home undergraduate fees unlikely to get inflation uprating any time soon, and with continued uncertainty about international recruitment (given international instability and government vote-chasing), there’s a case to see home PGT as the last great hope of the UK higher education sector. The pool of eligible graduates is larger than it ever has been, the availability of postgraduate loans is a welcome historical anomaly, and as an economy we are not going to stop needing higher level skills and knowledge any time soon.

Postgraduate taught courses receive comparatively little regulatory attention, and students have almost no official information about quality or comparability – it may be the only part of the sector where price signals work, but this is because of a lack of other information. To drive PGT expansion universities do need to come clean about the variable student experience (the PGT national student survey that Richard Puttock calls for would be a huge help).

It is great to see some discussion of this topic. The home PGT ‘market’ is extraordinarily diverse and those progressing direct from UG study just a slice of a bigger pie. The CPD element is significant (and often part-time); there are those changing tack (the conversion course market) and the engaged retired. However the real issue for the full-time UG to PG cohort is that fees are generally above the maximum student loan and often well above. This leaves living costs entirely unfunded. And with the state of accommodation costs in most university towns and cities this renders a Masters unaffordable. The only home folks who can afford PGT study are those with parental backing, deep pockets or a war chest from working for several years before returning.

Some thoughts. PGT market is made of sub strands with differences between the full and part-time, face-to-face and distance learning, the vocational and non vocational, etc. I think you have to look at the fall in PGT home numbers alongside: economic issues such as cost of living – including housing, mortgage and rental costs; changes to repayment levels on student loans; fuller employment; very different types of PGT provision – vocational versus academic, rise of 4 year UG degrees, etc. It is difficult to put a value for a home student on PGT study. Lots of universities are holding up (or trying to hold up) their PG numbers with scholarship schemes, which are basically discounts on full fees, which may make some PG provision unsustainable. Some disciplines see PGT study as a precursor to PGR study and with changes to PGR scholarship schemes, a PGT year may not be viable for the student. Not sure that I think the home business studies market is as impacted as you might think, but certainly home students interested in PGT are shopping very carefully. Economically, it is even harder for WP students to take a PG qualification. An interesting question is whether what we are seeing in the home full-time PGT market could ultimately be the same pattern for the overseas market if we don’t revisit the objectives and nature of PGT study(?)

The fact that “the nominal maximum £12,167 available loan for postgraduate study hasn’t really had an impact on fees”, considered here primarily as an indication of importance for the sector, would also seem to be an obvious explanation for falling numbers. How are students already heavily in debt supposed to fund a course which costs more than the loan available to pay for it?

A related factor is competition from integrated masters degrees: many (esp. STEM) students can choose between a whole year on freestanding MSc charged at uncapped PGT rates, or an extra nine months as an undergraduate charged at much lower UG rates and yielding a qualification many employers treat as equivalent.

I wondered about competition from integrated masters courses, plus of course apprenticeships in some disciplines, which might also impact on PGT study.