Universities need to pay staff properly, and staff deserve decent terms and conditions.

It’s not possible to be more unequivocal than that. It’s not a debate – there’s no valid position that says paying staff badly and treating them poorly is good for business or good for the UK. There’s no argument to be had on this principle.

There is often argument around what is affordable – and we do see a great deal of cherry-picked data used to argue for a particular position. With fresh claims made in recent days it feels like the right time to set up some parameters and definitions to make for a more informed debate.

How much money do universities have in the bank?

Cash and cash equivalents include, as the name suggests, cash – literal money in an account. It can also include things that can be readily and reliably converted into cash: stuff that has a market price that doesn’t fluctuate, like short-term government bonds and some other types of investment.

At the end of 2020-21, UK higher education providers had around £13.5bn as cash and cash equivalents, compared to £10.9bn at the start of that year. However, the figure was £11bn at the end of 2019-20, and £8.4bn at the start of the year. What gives?

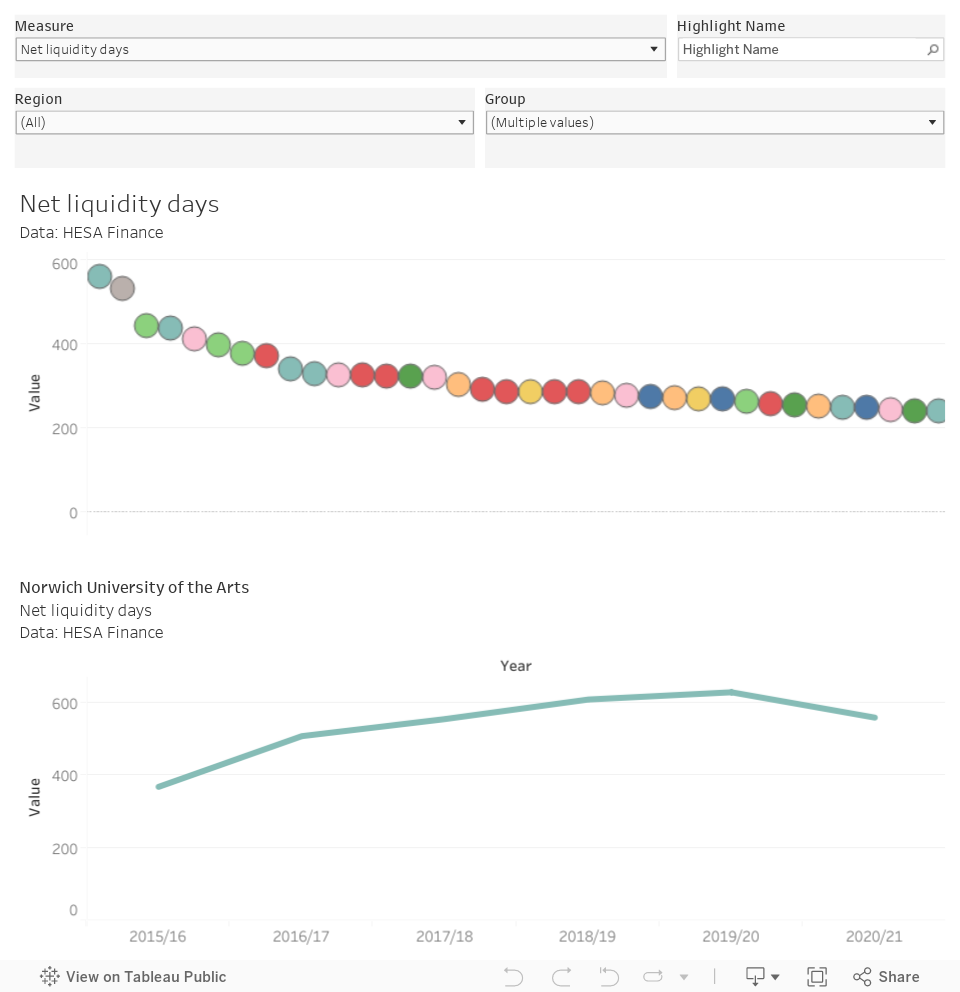

Cash and cash equivalents are often used to cover (unexpected) short-term costs – including the repayment of short-term debts and unexpected costs. It is a safety margin that feeds into our understanding of institutional liquidity – usually seen as a calculation of days of liquidity (crudely the number of days-worth of required expenditure a provider could manage without running out of money in the unlikely event of a complete cessation of income).

The overall liquidity of the sector is of less immediate interest to us than the liquidity of each provider. After all, it would be surprising (although really rather lovely) to see one university altruistically bail out a competitor. Here’s a plot demonstrating the variance in liquidity between providers:

It’s also important to remember that cash is what is there now – it is not a guarantee that similar amounts will be available to spend in the future. You could pay a bunch of salaries from your current cash holdings, but the thing about salaries is that staff prefer to be paid every year.

How much do they spend on “vanity projects”?

We’d have to take some issue with that framing. Removing dangerous cladding, and repairing decaying estate, isn’t the university equivalent of splurging on that shiny new paddleboard you’ve been fancying. Maintenance is a huge part of capital spending, and for both safety and financial (if you don’t maintain stuff it is worth less, and more likely to need replacement) reasons it needs to happen. There’ll be some of those new buildings too – providing much needed capacity, or replacing estates resources that are uneconomical to upgrade. Or maybe just making a tired old campus look more attractive to applicants and potential funding partners – investing to bring in more income.

Other things that fall under the bracket of capital spending include research resources (those cyclotrons the STEM folks like are pretty pricey) and computer hardware or software. As a rule of thumb, capital covers one-off spending whereas recurrent covers stuff you have to spend every year (salaries, energy costs, rates etc).

Capital spending on estates is becoming increasingly expensive – due to rises in the cost of raw materials and problems with logistics. On that basis, coupled with the fact that it has been quite difficult to do estates projects during a lockdown, you’d expect a projected increase in capital in 2022-23 compared to previous years.

OfS reported that:

Total capital expenditure fell from £3.7 billion in 2019-20 to £3.3 billion in 2020-21 as many providers continued to pause their capital plans as part of a strategy to protect cash flow while managing operations through the pandemic

And, looking forward at provider projections, noted:

Capital spend is expected to increase in 2021-22 (by 36 per cent to £4.6 billion) as many providers begin to implement post-coronavirus investment plans, consistent with reports from many lenders. Thereafter, forecasts show that annual capital investments are expected to reduce to lower levels than recent, pre-coronavirus years.

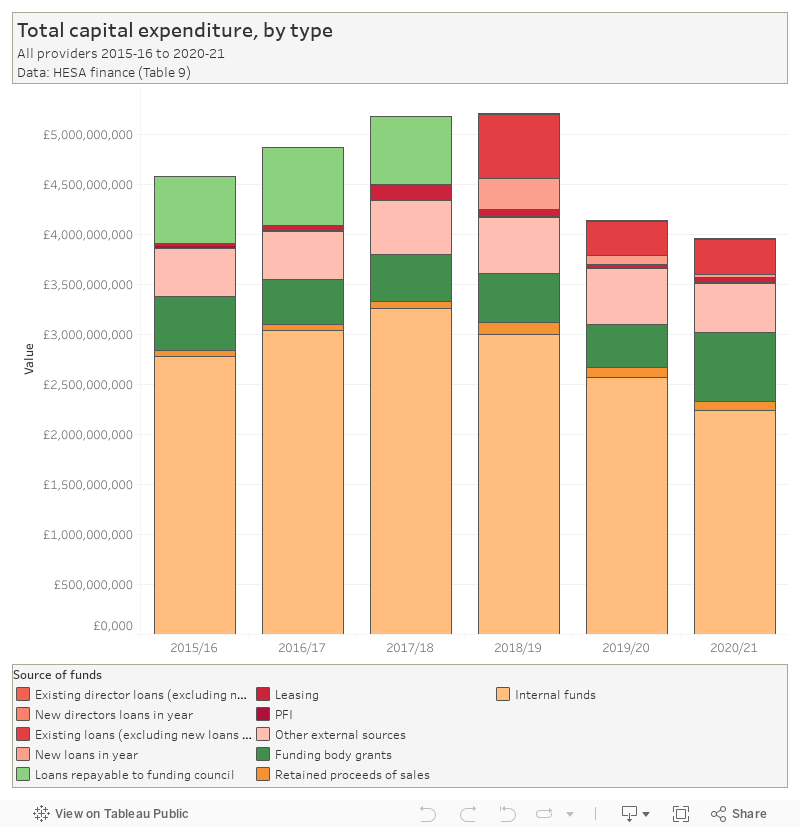

Where does this capital come from?

These charts are based on Table 9 from the HESA finances collection. The sector level one shows clearly the steady decline in capital spending since 2018-19 and the increasing role played by external income.

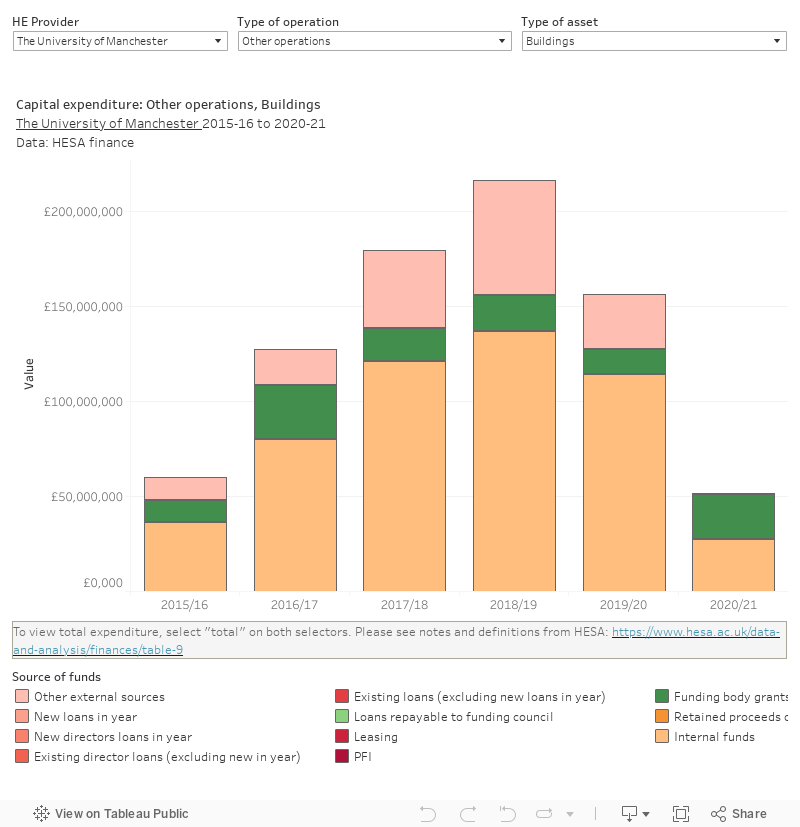

The provider level view lets you see a bit more detail at provider level (again, it is provider level that is important here – a scroll through a few shows a number of different positions and patterns, and the very largest providers skew the overall picture quite a lot).

You can also examine types of operation – with figures for catering, residential, and other spending – and types of asset – buildings, equipment, and intangibles (software and the like) by provider. To look at overall figures you need to select the “total” option in each box.

As we can see – on a sector level somewhere between a half and two thirds of capital spending comes from internal funds, with the remainder coming from external sources (basically borrowing and grants). You’ll note that proportionally more capital expenditure over time has come from borrowing across the whole sector. Again all this varies a lot by provider, so it is worth drilling down in the second chart.

How much do universities spend on staff costs?

Salaries and other staff costs represent the majority of recurrent spending by all but the very largest providers. In 2020-21, the sector spent just over £23bn (excluding pension adjustments) – up from £20.1bn the previous year. However, in 2020-21 the sector had 411,542.97 FTE staff, down from 412,182.5 the previous year – meaning the total spend per FTE (including on costs, not just salary) was up £7,289.03 (at £56,109.39 in 2020-21, £48,820.36 the previous year).

Bearing in mind what I said about the problems with looking at this in aggregate, and noting variations in salaries – this represents an ironically inflation busting 14.9 per cent increase in spending on a single FTE of staff over one year. If you are staring at your payslips in disbelief – bear in mind that on costs have risen sharply over that period. This does not absolve your employer from giving you a pay increase that addresses the rise in inflation.

And if you are wondering about more senior leaders on a high salary – there were 6,249.98 FTE staff on over £100,000, up slightly from 6,105.73 last year. We say “staff” because these are more likely to be senior professors rather than vice chancellors – and we also know that only 1,005 people in “academic services” and 1,000 in “administration” earn more than £62,727 a year compared with nearly 30,000 academics.

How much does the sector earn from fee income?

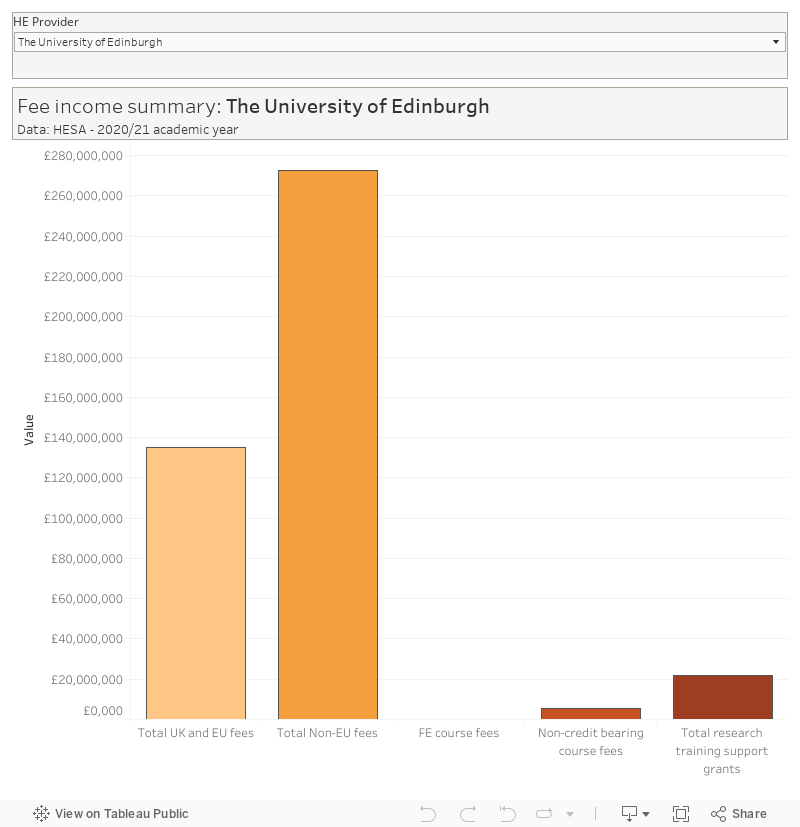

The proportion of provider income from fees (all fees, including the infamous £9,250 per year of undergraduate study plus the higher fees charged to international students and postgraduates, and plus income from other training activity) varies widely between providers.

As a sector – there was £23bn of fee income in 2020-21, up from a hair under £22bn in 2019-20 and roughly covering sector staff costs. Again there’s a surprise when we work this out per student – the average income per student (all levels, all domiciles) was £8,660 in 2019-20 but fell slightly to £8,639 in 2020-21.

We’re talking here about around half of the sector’s £44bn income in 2020-21, with the remainder coming primarily from a mix of funding body grants, research grants and contracts, and other income (such as commercial income) – with each of those bringing in between £6bn and £7bn in 2021.

UK and EU student higher education fees brought in £14bn in 2020-21 – this compares to £7bn of international fees. The majority of larger providers (including most Russell Group providers) earn more from home students than international students – though this includes both undergraduate and postgraduate fees. Here’s how this looks by provider:

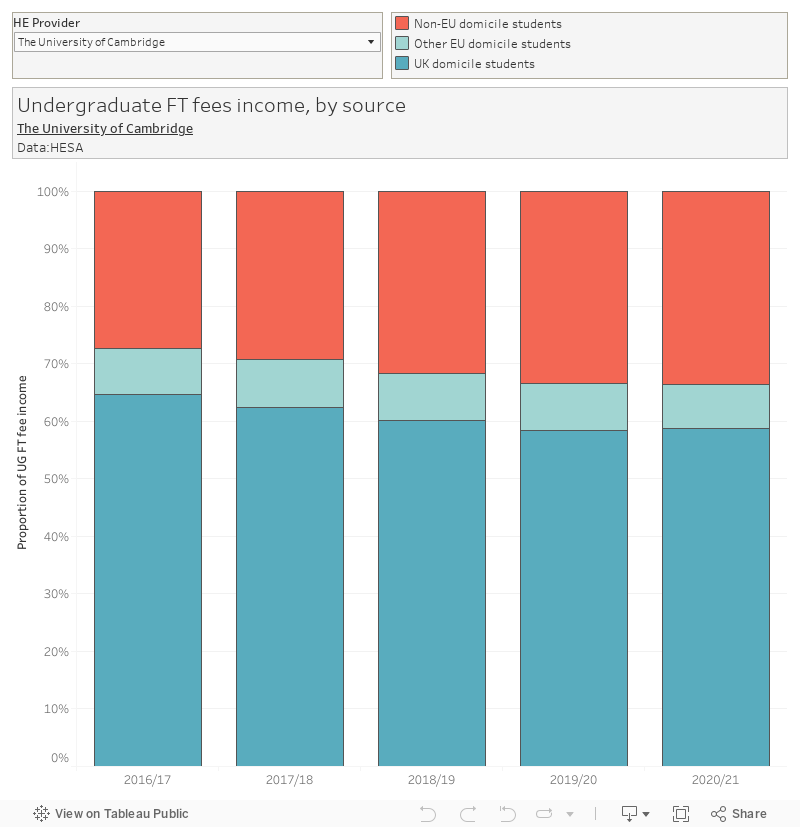

There’s been a lot of interest in the breakdown between income from home and international full-time undergraduate students. At a sector-wide level, undergraduate fees were worth a little over £14bn in England, Wales, and Northern Ireland in 2020-21 – with fees relating to home students coming in at £10.6bn. Again, here’s a provider level version:

International full-time undergraduate fee income does play a significant role for some providers. But – though numbers are increasing (inline with the government’s own international education strategy) we’re not really seeing any evidence of international UG FT recruitment playing an existential role in university finances.

But what about all those vanity project stories in the press?

With universities’ finances in their current state, you would be surprised and concerned to hear that institutions are planning a “£4.6bn splurge on vanity projects”. But this is exactly what it has been suggested the capital expenditure figures reveal, with frequent citation of the 36 per cent one year increase we have unpacked above.

The issue of spending on expensive new buildings is an interesting one, and worthy of detailed analysis – what was the business case for the new school of management, and how has that panned out ten years later? In reality, even the most hair-raising Private Eye expose is a drop in the ocean if seen at a sector level.

Investments in overseas campuses by University of Reading, Glasgow Caledonian University and University of Birmingham are given as examples – the latter in Dubai only fully opened this year, and is criticised on human rights grounds rather than as a wasteful white elephant – along with the case of University of Chester being obliged to “close down a campus which was built next to an oil refinery”. This refers to a former Shell research station turned science park which the university did not get permission to use for teaching, although it appears to still be available for research and commercial tenants to use.

What this all tells us

Higher education in the UK is, by any standards, big business. It’s easy to get lost in the billions that are being talked about at a sector level, and the temptation to see every provider as well off as a result of a single headline figure needs to be avoided.

The reality on the ground is different in every provider – some are doing enormously well, while others are genuinely struggling to make ends meet. It would be wonderful to be able to point to some reserve or unnecessary spend that could solve all of our problems – in the likely lack of further government support things next academic year are going to be very difficult.

It’s becoming more expensive to do pretty much everything – be that filling your petrol tank, buying your lunch, or refurbishing and making safe a mouldering science block. None of this excuses poor pay or worsening conditions, none of this makes squeezing more work out of staff (or, for that matter, more money out of students) anything other than a dereliction of duty. But identifying exactly where and how to make the changes that need to be made is a lot more difficult than some analyses let on.

Fantastically balanced and informative article – great piece of research.

Someone should direct UCU towards this article. Again, while offering lower than inflation pay increases is not excusable, the misunderstanding and/or (more likely) deliberate spreading of misinformation by UCU is astounding and extremely frustrating to witness as a member (especially from academics who are tasked with being objective and robust in their research).