2023-24 financial data (early year financial year end version)

David Kernohan is Deputy Editor of Wonkhe

Tags

Of the seventy-seven providers submitting financial data to HESA in the latest round of collection, twenty-seven were running a deficit in the 2023-24 financial year.

Providers with non-standard financial years (those who do not follow the patterns established by more traditional providers, who tend to start a new financial year in August) are primarily smaller and more specialist institutions who have entered the sector more recently.

Many are explicitly private, for-profit, providers – a failure to break even in this part of the sector represents a surprising turn of events. It also augers poorly for performance in an even more difficult 2024-25 financial year.

The variation in form and financial practices mean that some KFIs – such as net liquidity days – are less useful in understanding performance. However, the fact that five of these providers have external borrowing at more than 100 per cent of total income is a worry.

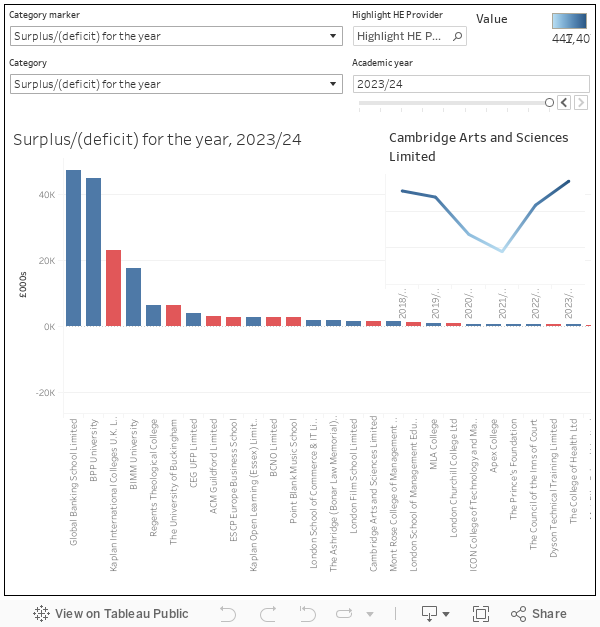

Some larger providers in this group – Global Banking School, BPP, Kaplan, BIMM, and so on – show a healthy surplus for the year, while others (notably Study Group) reported a significant deficit. BBP and Kaplan were in receipt of more than £100m a year in tuition fee income, with Study Group not far below that.

This early look at sector finances for last year meshes with the kind of thing we are seeing in financial reports currently being published by larger providers (that will find their way onto the HESA data tables in the middle of next year). There are no huge surprises – providers with a sustained record of good financial performance are suffering, but in general are weathering the storm. It’s the places where fundamentals have looked anemic over the past few years that are beginning to ring alarm bells.