It’s hard not to feel a deep sense of despondency when reading the Unipol/HEPI interim student accommodation costs report.

The exercise is usually carried out every three years by Unipol and NUS – but given the weight of anecdotal evidence that something dramatic and significant has been happening to rents since 2021’s exercise, Unipol resolved to run a shorter and more tightly focussed version of the exercise this summer.

The headline – at least in the ten key city markets chosen to reflect a range of supply/demand scenarios – is that student rents have gone up by an average of 14.6% over the past two academic years, and now “swallow up” pretty much all of the average maintenance loan on offer to students from England.

“Crisis” is an overused word – but when Victoria Tolmie-Loverseed, who is Unipol’s Assistant Chief Executive, says that student housing has reached a crisis point in affordability, she’s clearly right:

Rents are rising rapidly just as real-terms government support has stagnated. With rents consuming unhealthy levels of an average maintenance loan, students are being forced to take desperate measures – illegally doubling up in rooms, taking on increasing amounts of paid work or even avoiding university altogether due to costs.

Failing to address the student housing crisis risks undermining decades of progress in widening participation in higher education. We risk excluding those from poorer backgrounds, forcing middle-income students to take on unsustainable debts, and damaging the student experience for all.

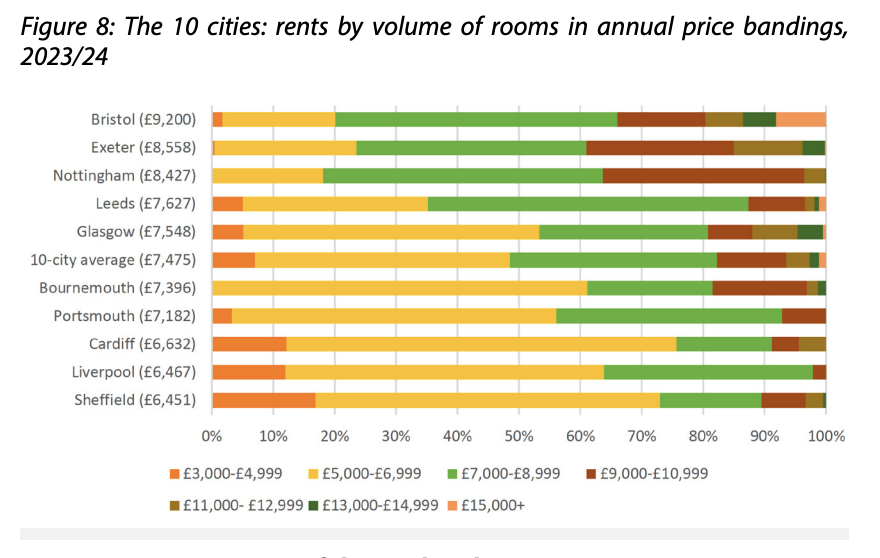

Averages can be deceptive – so one of the more interesting tables in the report is the one showing the 2023/24 rent range. Here cities are ordered according to that average – Sheffield, Liverpool and Cardiff all have lower rents in the mid-£6,000s and offer a broad spread of prices.

Meanwhile most expensive are Bristol and Exeter where there’s much less spread – a market that the report says is likely to be a setback in efforts to widen participation and rebalance populations historically dominated by students from more affluent backgrounds.

Will we stand a loan?

There’s a frustrating little section in the report on rent as a proportion of maintenance loans that states that “student loans were never meant to cover all living costs for all students”. Fair enough – but at least the maximum loan used to be designed as such.

The adequacy of the total maximum package of loans and grants was debated extensively in 1990 when the system cut students off from the benefit system – especially when considering different parts of the country – but the government’s formal position then was that its package…

…provides an adequate level of support for a student to be maintained without work during the course of study.

Later in 2006, having just received results from the Student Income and Expenditure Survey (SIES) the previous December, Charles Clarke’s big announcement was that from September 2006, max maintenance loans would be raised to the median level of students’ basic living costs on the basis that:

…the decision will ensure that students have enough money to meet their basic living costs while studying.

Regardless, that the maximum loan – still available to those on a family income of £25k or less – now only leaves less than £2,500 to live on after paying the average rent explains the hours students are working and the private debt they’re getting into.

The big question, though, is what we do about it – and to work that out, we really need to understand how we got here.

Supplying demand

The report identifies four key reasons for recent rent rises being so steep. First is costs, where both universities and private operators of halls report significant rises in energy costs, staff and wage costs, supply chain costs, debt servicing and the rising costs of construction. They are pretty hard to argue with – although there isn’t commentary on the extent to which profits or surpluses have been hit as a result in a market that has historically been exceptionally lucrative for private investors.

Next is inflation – which is really a subset of costs and a way of explaining a slow down in supply growth. Third is the costs of voids faced during Covid – where 25 per cent of private providers are in the process of clawing back those costs through hiking up rents now rather than taking a profits hit. And fourth is a short section on “supply and demand” – which pretty much only discusses supply, giving the example of Liverpool as a city which has had a surplus of beds and where rents have increased by only 10 per cent (a 5 per cent rise in each academic year).

That leads to the sort of recommendations we might expect – fixing the “broken” maintenance system and basing it on how much it actually costs to be a student living independently; restructuring long-term university-private partnerships to have a focus on affordability; better information, advice and guidance for students; facilitating more supply through the planning system; and more joined-up government policy.

As a set of recommendations, they all make sense – save that it’s not really good idea for rent to be this high, even if loans did cover it. If it was possible to squeeze more borrowing out of the government, students and the sector would surely want that funding food, study materials, social activity or travel to campus – not rent. How on earth can it be that rent is now almost as expensive as the actual tuition fee, and why on earth would the sector want to maintain that?

That’s why for me, the “solutions” are also the source of that deep despondency – because they’re either painfully long-term in their outlook, call for money to go to the wrong people for the wring things, or feel unrealistic in the current political climate. Crucially, they’re all things where universities have limited powers – whereas when it comes to demand, universities have plenty.

Transitional demand

I should be clear that demand is discussed briefly in the report – but while the word appears 15 times, supply appears 40 times. Where it is discussed, it feels like an inevitable – something the sector is helpless over, something to respond to, rather than something that could be influenced. And there are precious few references to postgraduates.

I had a look at the Scottish question on the site here – but if we take England and only look at the growth in international postgraduates in the two biggest providers in the eight cities in the report between 2020 and 2022, numbers went from 21,035 to 42,215 – they doubled. Visa issuance figures suggest they’ll have climbed further still this year.

Either there were 20,000 spare beds in those cities in 2019, or the sector recruited more students than its local housing markets could bear.

| OfS/HESES | INTL PGT 2020 | INTL PGT 2022 | % Increase | |

|---|---|---|---|---|

| Bournemouth | 885 | 2080 | 135% | |

| Bristol UWE | 875 | 2225 | 154% | |

| Bristol Uni of | 2515 | 3405 | 35% | |

| Exeter | 1735 | 2690 | 55% | |

| Leeds (uni of) | 2910 | 5925 | 100% | |

| Leeds Beckett | 710 | 3065 | 332% | |

| Liverpool (uni of) | 1200 | 2400 | 100% | |

| Liverpool JM | 350 | 860 | 146% | |

| Nottingham (uni of) | 1445 | 3215 | 123% | |

| Nottingham Trent | 955 | 2715 | 184% | |

| Portsmouth | 1675 | 3860 | 130% | |

| Sheffield (uni of) | 4695 | 4785 | 2% | |

| Sheffield Hallam | 1085 | 4990 | 359% | |

| Total | 21035 | 42215 | 101% |

Some of those totals may be making up for lost students from other parts of the student body in those universities, but given the big reason that we’re told has led to those increases is the ability to get onto the 2-year graduate route, the compound impact of those increases on housing demand is almost certainly much bigger than the headline figure. And by definition, every single one of those students needs a bed.

If “supply” is identified as often as it is, it’s impossible to believe anything other than more modest increases in international recruitment would have led to more modest increases in rent. Rents have gone up in the way they have because providers could put them up. Because demand has grown much much faster than supply.

Full and standing

Where a university recruits students that it knows will be living away from home, there are factors to consider when resolving how many it can recruit – given there are no caps. One relates to where those students – both home domiciled and international – will live.

If we consider it pretty essential that they’ll be able to rent somewhere that’s affordable, of a reasonable distance from campus and of a reasonable quality, overall supply analysis matters. It’s a key thing that Universities UK suggests universities do in its guidance – yet I still hear of it not happening in any kind of systematic way across the UK.

The truth is that universities previously didn’t have to think a lot about it outside of first year guarantees – but it’s increasingly important now given the scale of HE and the wider housing crisis.

Universities don’t, and won’t any time soon, “control” the local housing market. But given it is a market, for any market to work there has to be a moderate oversupply. That, in a market, is what allows for both downward competitive pressure on rent, and for choice over type and quality to emerge – as that chart above vividly demonstrates.

Thus the tighter the market, the more morally dubious it becomes to recruit “away from home” students into that local market – given the impact it can have over experience and outcomes. ·

That is not to discount the pressure on universities to increase international enrolments in order to make their budgets work. But it is to say that when that involves recruiting students into a tight or even undersupplied housing market, it just transfers a financial pressure point from the provider to the student body – and in the end, back to the provider.

Outside of the in-principle debates about number caps, the question remains – when is a university “full” from the POV of the recruitment of students living away from home?

The current picture in several university cities has moved from loose (where competition drives down price and increases choice), to tight, to chronic undersupply. Or put another way – it’s gone from a market that sort of worked if you ignore the other things that make landlords powerful and students vulnerable, to one that is broken and completely failing to do what markets are supposed to do. Those markets are full.

Not my job

This isn’t really about blame – but once full, it raises the question – should the responsibility be on students to judge that and avoid the place, on universities to stop or slow recruiting, or an arm of the state to cap places either regionally or nationally?

If you place the responsibility on students, there has to be much much better information and consumer protection enforcement. That’s not coming any time soon, and the competition between providers for students will always cause a tendency to mislead on housing by omission if not by direct action in a way that the CMA seemingly couldn’t care less about, and OfS has no remit over.

If you place it on universities, there has to be some forced collaboration centred around place, and a reduction in the need to fund UK HE through international recruitment. The former appears to be much more difficult than even the UUK guidance envisaged, and the latter is pretty much a write off for the next five years.

And if you place it on the state, you have to pick which bit of that state and give it powers to exercise responsibly. And honestly? In a wider housing crisis, there almost certainly aren’t any bits of the state that would act in earnest to prioritise beds for students, let alone international students, given the acute problems for other citizens, the way we “other” students as educational tourists, and the way in which politicians under pressure from voters will blame universities for exacerbating the problem.

But we do have to pick. It can’t be that providers are free to recruit when a place is “full” and the only solution is to cry into the wilderness “more supply in the long term”.

Supply is part of it. But it can’t be the only cry. Not when the behaviour of providers in the HE market makes it consequently impossible for the related student housing market to work – with impacts on local people as a result.

Put another way, all other factors aside, if in a market the price of something is about both supply and demand, we have to face up to the fact that universities have much less influence over supply than they do over demand when it comes to housing. The sector helped to break it. The sector has to help fix it.