University education remains aspirational – a route upwards to securing the right job and the ability to compete for it.

Degree courses are expensive, but applicants see it as worth the investment in a life plan (among disadvantaged young people in particular) that is extremely clear. The discussions tend to be around ways to minimise living costs – choosing a university based on rental costs, or living at home during study. Students from less affluent families are much better informed about the true costs of university and sources of help available, but there is still a problem in accessing good quality formal advice on this. And full time is still seen as the gold standard – maximising the university experience and hastening entry to graduate employment.

The All Party Parliamentary Group commissioned Public First to get a grip on how young people in England feel about university and university finance. The timing is such that it is difficult not to read this a rebuttal to an announcement that didn’t happen on Wednesday last week – an (unweighted) poll of 1,000 students on the cusp of applying to or starting university, plus three “less affluent” focus groups (Wolverhampton, Derby, Middlesbrough) and six in-depth interviews (Richmond, London, Sheffield, Oldham, Manchester) of applicants from a range of backgrounds would make for uncomfortable reading at number 11 and in the Sanctuary Building had the stars aligned slightly differently.

Access

There is no support among these young people for limiting access to university places – and this opposition became clearer during conversation than when asked as a poll question. Academic requirements are perceived as de facto minimum entry levels, suggesting that if a person has the requisite UCAS Tariff points then he, she, or they should be able to access the course whether or not their early academic career passed muster.

The cry from the expensive commentary seats is that there are too many universities (and other places offering higher education courses) and too many courses – Russell Group member the University of Birmingham’s targeted vocational offer on Golf Course Management (typical offer: ABB at A level, employment rate: 88.9 per cent) being one of the current targets of ire. It’s an example of a niche course that is hugely attractive to students with particular career goals – less affluent students benefit in particular from a wide range of courses available from multiple providers.

Clearly, tuition fees are not popular and in yet another survey this is borne out with hard numbers. Prospective students generally accept that the political weather is such that fees are here to stay, and the argument that those who do not benefit from university education should not subsidise those who do (frequently made by ministers over the past decade) appears to be at least attractive in concept. Interest rates on loans are also not popular – most feel they should be reduced, but neither of these are issues that really seem to cut through.

But a concern for equity and access remains – as one student put it:

If you’re poor you’re less likely to go to university which I don’t think is very fair because they might have the same goals and aspirations as someone who’s more fortunate.

When led through options, applicants can be made to agree that different fees for different courses was fair, with some courses having more value than others – even so, with 40 per cent in favour and 33 per cent against we’re perilously close to this being a margin of error effect – hardly a ringing endorsement of the idea.

There’s some fascinating stuff on applicant awareness and interest in alternative post-compulsory destinations. It doesn’t look like there is any untapped interest or demand for other higher level qualifications – even part-time university study was not of interest to this same (80 per cent were aware and not interested in it, 9 per cent expressed an actual interest). Degree apprenticeships were the best of the rest (25 per cent aware and interested, 66 per cent aware and not) – but this all points to a continued demand for the existing offer, no matter what DfE put in their impact assessments. Shifting behavior will require serious work.

Debt

Meanwhile, the idea that disadvantaged students are not put off by high debt levels takes a knock – 35 per cent of applicants in this study who had been eligible for free school meals reported being put off applying to university by debt concerns. For those who do, the story is one of a leap of faith rather than an actuarial calculation – the debt is daunting, but the belief that it will somehow work out is stronger. As one applicant put it:

I reckon I’ll apply – definitely – I think they’ll be a way to pay; but I need to look into it more.

It’s a balance of risk, but one based on incomplete information and self-belief – with the latter lacking in students with a history of financial family struggles. Having friends and family who have already been to university and balanced things helps a lot in making this leap too. Even before getting to university, the value of a good network is paramount in understanding the realities and costs of student life.

Maintenance

The report doesn’t get much into maintenance but the data tables absolutely do – and it makes for painful reading. The average weekly student spend was £187 this year according to save the student, and a narrow majority (54 per cent) respondents who are either already at university or about to go expected to spend between £100 and £300. However, the plurality (57 per cent) of students from financially struggling backgrounds put the cost at between £200 and £400 – perhaps anticipating that having the occasional cost covered by parents is not an option.

The maximum available loan for a full-time undergraduate studying outside London works out at £182 a week over 52 weeks – the average student in receipt of a maintenance loan saw £134 a week last year according to the Student Loans Company. More than 28 per cent of all students in this survey expected to be able to access more than £200 in loans a week – suggesting either a lack of information (a further 23 per cent did not know) or the inclusion of non-SLC borrowing. Unsurprisingly 39 per cent felt that maintenance loans (and any grants) would not be enough to cover living expenses.

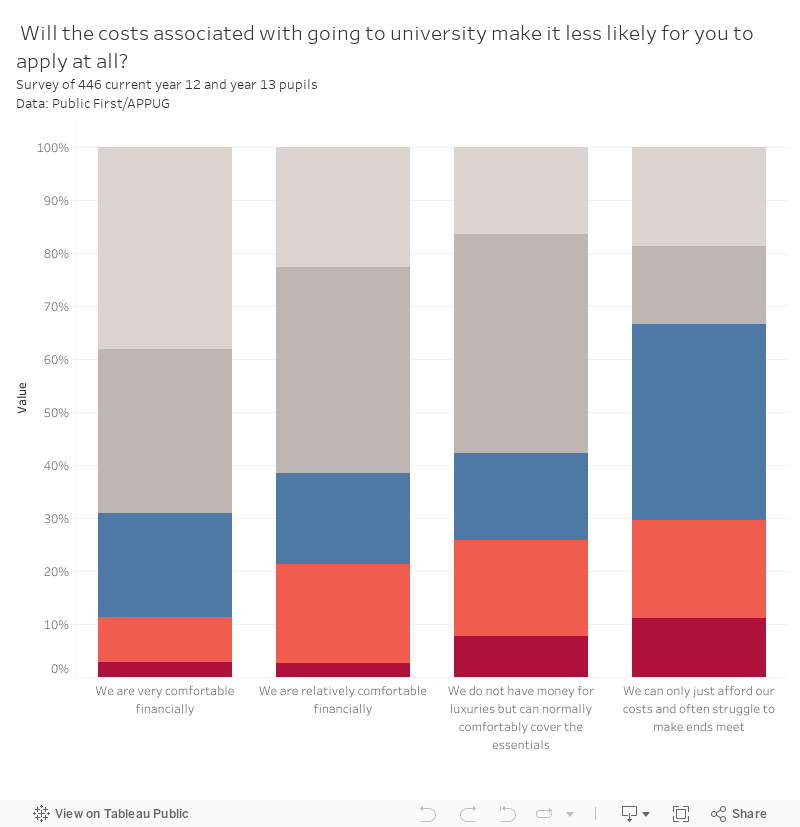

Six per cent of those from poorer backgrounds reported that they would not be able to cover the costs of attending university – a further 31 per cent reported that they would cover costs “with great difficulty”. Thirty per cent of the poorest group of respondents in their final year of Level 3 courses would definitely or probably not apply to university because of the costs associated with it – a further 37 per cent were “not sure”.

If there is a policy prescription here, it is not a new one. Applicants are most exercised about the unfairness of interest – support for a 30 year limit on repayments was overwhelming, as was a repayment threshold of £30,000. There’s also strong support for fee amnesties for public sector workers. There was no question about support for maintenance improvements, but I think we can guess what the answer would be.

What’s next

Once in a while, a survey comes along that acts as a partial corrective to some of the more speculative positions that seem to become orthodoxy. The raw numbers of access suggests that university is more popular than ever among students from all kinds of backgrounds, the findings here at the very least problematise that sense that this means that loans and fees don’t put off disadvantaged applicants.

And there is little to support the oft-cherished idea that young people are crying out for vocational alternatives to the traditional full time three years of study at university. Even among the small number of applicants who have heard of the alternative there is little evidence of interest – which rather suggests that if government wants to limit spending on higher education it may mean limiting the number of available places.

But the big findings here are on the inadequacy of current arrangements for maintenance – a topic deemed less newsworthy than fee levels and with fewer recommendations that get people lobbying in either direction. It feels unlikely that any pending changes to “fees and funding” will make a meaningful difference – and all the while inflation (and thus the cost of living) looks set to keep rising.