Nobody has any complaints about learners of all ages having access to government support to learn new skills and pursue new interests.

The Lifelong Loan Entitlement, as proposed, is just one among many possible approaches to doing this. Every major political party has, or is developing, their own approach to support for lifelong tertiary learning.

With the principle settled, the arguments between competing systems are necessarily technical – and burdened with projections about the future earnings of individuals and the course of the national economy through what are likely to be difficult times ahead.

Intentionally simple

It can be hard to get your head around what is going on, so I’ve built the most basic model of Plan 5 within the LLE context that you can possibly imagine.

Simple models do not accurately reflect the lived experience of people who take out these loans. They have nothing to say about the effectiveness (or otherwise) of lifelong learning. Even some of the most sophisticated analyses of student finance only talk about medians and “most likely”. But what a simple model – with sensible assumptions – can do is give us an overview of the principles by which loans and repayments work.

I’ve assumed wages will rise inexorably by the same proportion each year – and RPI will be constant. Against hope and experience I’ve assumed the government doesn’t change the terms of the loan midway through. I’ve assumed that not everyone will choose to take out maintenance loans, but – if they do – they will take a pro rata amount based on the current figure for living away from home, outside London (you can tweak this if you want). You can also tweak the fee loan available per credit – I’ve taken ministers at their word that it will be pro rata based on the current £9,250 higher level fee cap, but you can also tweak this on the model.

In fact you can tweak most of the variables – the only important hidden one is the expectation that your repayments are 9 per cent of the portion of your annual salary above the threshold. It’s helpful to see loan repayments as 9 per cent tax on income above the threshold, lasting either for 40 years or until the principal (adjusted annually by RPI) is repaid.

What to mess with

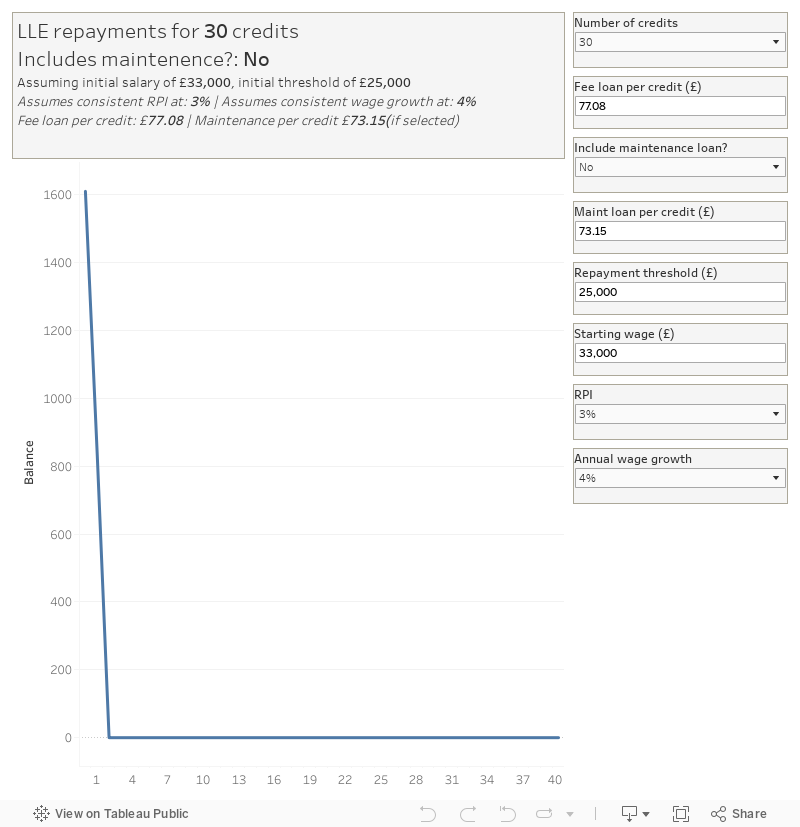

For the learner, there are two projections that are absolutely key – the future interest rate (RPI) and the future growth of your wage. As long as your wage is growing faster than RPI, the system will work as expected – you will gradually pay down your loan. For my initial example, above, a person earning the national median wage of £33,000 taking out a fee loan for 30 credits (£2,312) will pay it off in 3 years, assuming RPI at 3 per cent and wage growth at 4 per cent.

But if you take a long term RPI in line with the current economy – say 8 per cent – the learner in this same example will be paying off their loan for the next 40 years with everything else as previously assumed. And if you assume someone starts with their wage at the threshold, RPI just needs to hit 4 per cent for this same hysteresis to occur.

As long as you have a fee loan to repay, you are repaying 9 per cent of your salary above the threshold. If you imagine someone taking the smallest available loan (30 credits) each year, they will be making this payment every year until the last of these loans are paid off – and as repayments start at the end of the period of study in question this will include the period of study.

This doesn’t affect your repayments (it’s always 9 per cent of your salary above threshold) but it does affect the length of time you will be making them. And if you are in a low-wage job where pay grows more slowly than inflation you will be paying the same 9 per cent of your salary over the threshold for the next 40 years – whatever the initial value of the loan is.

Advice needed

Two things to note – this is based on a very simple model that will not address the experience of most learners. And the issues I have highlighted are not issues with the LLE specifically – they are issues within the design of Plan 5, and the way LLE would allow people to use loans just makes them clearer.

Recently, Wonkhe’s Sunday Blake argued that to help people make the most effective use of their LLE entitlement we needed a sea change in careers advice and guidance. I’m afraid that I’d have to add an understanding of both fiscal and monetary policy, an eye on national economic performance, and quite probably trade union membership to ensure wages grow. I can’t assume that this is the government’s intention.