“Students make a considerable investment in their studies… they need to be confident that they can choose a high quality course from a financially sustainable provider”.

So begins a curious new note from the Office for Students (OfS) on how it regulates financial sustainability within higher education.

As well as being assured that OfS has the right people (“experienced and professionally qualified accountants, experts in data and analysis, colleagues with significant experience in the policy and legal environment”) we are told that the regulator has successfully intervened in providers that have faced significant financial difficulties – ensuring it takes steps to mitigate risks and to support students to continue their studies.

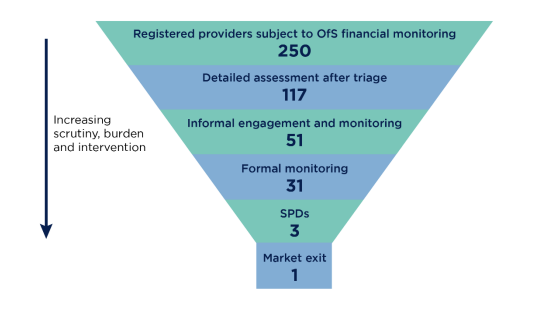

We’re treated to this cone of burden, scrutiny and intervention from its work in 2021 – which reveals that of the 414 providers on the register, 250 have to submit a detailed return, 117 had been subject a more detailed assessment after triage, 51 got a closer look via “informal engagement”, 31 were being “formally” monitored, 3 were subject to “student protection directions” and 1 collapsed.

We’re not, of course, given the identity of any of the above except the one market exit case, which from a student perspective, is more concerning the further a provider travels down the cone.

We also don’t have any sense of the scale of the providers in each part of the cone – for all we know, the bulk of problems are in smaller providers ushered in by the current government’s decade-long reforms to encourage alternative providers.

What we do know is the identity of that one provider that exited the market – the Academy of Live and Recorded Arts (ALRA) – and as well as the general note on financial sustainability, we get a whole note on that tale.

We’re talking about Reaganomics

You’ll recall that on April 4 last year, it emerged that ALRA staff had been sent an email at 2am informing them of a Zoom meeting at 9am that announced the provider’s closure and their redundancy. Its circa 300 students had been locked out, both from the two buildings in Wandsworth Common and Wigan, and from their email accounts.

That raised questions about who knew what and when – and crucially, whether students should have been warned, even though, in this case, Rose Bruford handily stepped in to save the bulk of affected students.

We didn’t really get answers at the time – but now in a document that technically includes two other anonymous case studies, we have a retelling of the tale, which like the regulating financial sustainability guide, very much describes OfS as the caped crusader sweeping in to save students.

Here OfS tells us that towards the end of 2021 ALRA reported both a substantial increase in its deficit for 2020-21 compared with what it had reported previously, and an increase in its forecast deficit for 2021-22 – ostensibly due to the termination of a partnership with an American university. It also highlighted a number of long-term financial issues, including poor debt recovery, limited investment in back-office functions and overstaffing.

It doesn’t tell us whether ALRA had used the “reportable events” regime to tell OfS about its restructure in Spring 2021, or whether having done so that sounded any alarm bells in Stoke Gifford.

We’re therefore not told why a restructure like that didn’t trigger a rewrite of the student protection plan, which means the version on its website dated September 2021 (the one that year’s freshers will have seen) said that the risk that it would be unable to operate was “very low” and the risk that it would be unable to deliver any of its programmes in the next 3 to 5 years was therefore “correspondingly low”.

I went to the bank to see what they could do

What did ensue was a series of interventions – closer monitoring and the imposition of a “student protection direction” – all on the basis that OfS figured the chances of the management pulling off an acquisition were shaky, or in other words OfS judged that ALRA was at “material risk of market exit”.

As well as puzzling over the SPP describing a bed of financial roses, we might also wonder why that “material” risk judgement and protection direction was kept a secret. The answer is as follows:

We took the view that public statements about a market exit plan and ALRA’s financial position would have affected its ability to progress its acquisition and would have increased the likelihood of a disorderly market exit. We considered that the need to minimise the risk in relation to the continuation of study for current students outweighed other factors, such as the interests of prospective students

Technically OfS has to weigh up respective interests when deciding whether to make most of its judgements and interventions public, and here it went for secrecy. Those who enrolled earlier in the year and those on the roll at the time will almost certainly resent being kept in the dark. And the secrecy also has the advantage of allowing OfS to avoid scrutiny over its interventions and judgements in cases like these.

What we do learn is the speed at which things went pear-shaped.

Son, look like bad luck got a hold on you

In early February, OfS had threatened a “student protection direction”, and ALRA had duly submitted a “market exit plan” that OfS thought not good enough. By Feb 15th ALRAs hopes of being acquired were dashed – at which point our superhero regulator “established a multi-agency taskforce” to coordinate planning.

We’re told that “there were more than 60 meetings of the taskforce, or sub-groups of taskforce members, between 12 February 2022 and 27 April 2022”, which is designed to sound impressive, but I think sounds chaotic, and makes you worried for what could be to come if lots of providers run in to trouble at the same time amidst an inflation crisis.

The rest of the story we pretty much know – Rose Bruford stepped in, and most students lived happily ever after. But questions remain.

As we noted last year, what we can say with some confidence is that the “current” published and apparently approved Student Protection Plan from last April predictably turned out not to be worth the paper it wasn’t printed on.

Its risk assessment simply wasn’t accurate – students who enrolled in 2021 will still want to know how a “low risk” judgement could have been compatible with a restructure last spring and a collapse by early 2022 – and its risk mitigation step of a commitment to “teach out” in the event of provider closure exposed as hopelessly inadequate.

And had Rose Bruford not been able to take up the slack, the situation could have been much worse.

I can’t even qualify for my pension

As well as the ALRA tale, we are given two other case studies. The first is designed to assuage fears that “current” SPPs are inadequate – describing a provider where income from student fees had not kept up with staff costs.

OfS says it required the provider to update its student protection plan – but again the secrecy issue rears its head. On the one hand, OfS says its view was that the provider’s old plan did not contain sufficient detail about the actions it would take to ensure continuation of study for its students as it made changes to its course portfolio.

It did not think that a student would easily understand the options available and how their interests would be protected in these new circumstances – and so approved a revised student protection plan and ensured it was published and drawn to the attention of students. Great news.

But at the same time, it did not consider it appropriate to require the provider to include in its student protection plan the actions it would take if it could not continue to operate as a result of its financial difficulties. It took the view that public statements about the provider’s financial position would have affected its ability to implement its recovery plan and could have made market exit more likely.

And so again, it considered that the risk to continuation of study for current students outweighed other factors, such as the interests of prospective students, that might have suggested that publication of this information in a student protection plan was appropriate.

Again when asked to weigh up those secrecy concerns, the right of prospective students to see if they’re about to enrol in a provider that OfS reckons is risky is set aside – as OfS keeps everything quiet to try to give the provider a chance to survive.

And we’re not told whether students being subjected to what was doubtless a dramatic course portfolio review were happy with the steps taken to enable them to continue.

I can’t get an unemployment extension

In the second anonymous case study, a provider notified OfS that it was running out of cash. Reserves had been depleted to deliver a planned capital project and manage the impact of a shortfall in student recruitment, and it wouldn’t be able to pay staff within the next three months if it couldn’t secure new or revised borrowing or other funding.

Again, it’s not clear how or why this had only emerged then via a notification, but OfS swooped in to save the day – this time commissioning an independent organisation to review the provider’s plan and its management and governance arrangements. Over whether to reveal risks to students, it had that secrecy decision to make – and again, it chose to keep quiet:

We did not consider it appropriate to require the provider to include in its student protection plan the actions it would have taken if it could not continue to operate as a result of its financial difficulties. This was because the proposed specific condition would have provided a more effective mechanism to protect the provider’s students without exacerbating its financial challenges. We did not therefore require the provider to amend and seek approval for a revised student protection plan.

And on whether to reveal that it had imposed a specific condition of registration over the finances, again it chose to keep quiet:

We did not publish information about the imposition of the specific condition because we took the view that public statements about the provider’s financial position would have affected its ability to implement its recovery plan and could have made market exit more likely. At that time, we considered that the risk to continuation of study for current students outweighed other factors, such as the interests of prospective students, that might have suggested that publication of this information in a student protection plan was appropriate.

Naturally, following these interventions, everyone again lived happily ever after – described here as “the provider improved its financial position and is now subject to the same general monitoring and associated regulatory requirements as other registered providers.” But is that the end of the story?

Brother, I’d like to help you, but I’m unable to

In the accompanying press release for all of this, David Smy, OfS’ Director of Monitoring and Intervention, says that much of OfS’ work on financial sustainability is not visible at the time, and he intends these case studies to demonstrate the approach taken to protect students’ interests:

The nature of the OfS’s role means that formal regulatory action will always be in the spotlight, but these case studies demonstrate the collaborative approach we have taken in challenging circumstances, alongside the use of our formal regulatory tools.

That’s all well and good, but there is something strange about the regime that is emerging here. On the one hand, Smy reasons that OfS isn’t there to “prop up a university or college which is not financially sound” – but by keeping financial risks a secret, that’s exactly what it does.

Add to that a lack of external scrutiny over what OfS knew and when and whether it could or should have intervened earlier, and the repeated choice to protect the theoretical risks of current students over those of prospective students, and the danger for OfS is that it looks like it keeps things a secret because it fails to deliver sufficient transparency for students choosing a provider at the outset.

More to the point, OfS’s work on the risk of full-blown market exit continues to prioritise that particular kind of “risk to the continuation of study” over all others – like collections of modules that mysteriously disappear, whole pathways that go up in a puff of smoke, and entire campuses that can be just closed without the risks of that happening being clear or the mitigation steps being recorded as credible.

It’s inevitable when it’s OfS marking its own homework – but the whole area of student protection as provider finances tighten has never needed more scrutiny.

This article reads more like everyone in HE wants to know what everyone else is doing rather than a robust consideration of how institutional finances should be monitored and supported by a regulator. This approach by the OfS is consistent with other regulated markets. If organisations in regulated markets felt that they couldn’t discuss serious situations without them being made public then those dialogues would stop, there would be more surprises /collapses which serves no-one. There is an inherent assumption in the piece that students are due some higher level of protection, than say other “customers” or creditors. All HEIs produce and publish annual accounts, and therefore there is publicly accessible information for students to make judgements on financial sustainability of organisations (if they really want to…). Often these precarious situations require very careful negotiation in order to avoid panic and an otherwise avoidable collapse. Underneath this it is also important to remember the statutory duties that Directors (Boards and Accountable Officers) must exercise in these situations to protect stakeholders. Ultimately it isn’t the OfS’ responsibility to prevent market exits and their approach seems entirely what one would expect of a regulator…

It has long been the case that exposure of financial weakness precipitates the very collapse that behind the scenes negotiation can, and often does, prevent. This is true in all sectors. Averting banking crises are the highest profile, but even Kids Company might have survived if Ministers hadn’t bottled out in the face of intense media scrutiny and paid at least some of the promised grant that the trustees had been expecting.

‘Rescue’ in some form or another is usually preferable to institutional failure for employees, customers (students) and creditors. the last of these are often banks, whose confidence in the HE sector has been crucial for many decades (in terms of both support in hard times and in very low interest rates charged to the sector). In HE, examples of negotiation leading to a rescue go back at least as far as the then University College, Cardiff and its reverse takeover by UWIST (now Cardiff University), but include Wye College, Bretton Hall, London Metropolitan and more. Publicity is likely to have seen closure and serious student hardship.

Private discussion and negotiation is not synonymous with ‘secrecy’ – often (as here) a pejorative term

It is interesting to compare this case study with HEFCE’s account of its dealings with London Met (https://webarchive.nationalarchives.gov.uk/ukgwa/20130703230357/http://www.hefce.ac.uk/news/newsarchive/2009/hefcesdealingswithlondonmetropolitanuniversity/).

The OFS note skates over the fact that 164 (39%) of the providers on its register are not subject to its financial monitoring because, as FE or sixth form colleges, their finances are regulated by the Department for Education and its agents. This process is more public, in that DfE publishes any financial notices to improve that it sends to the college and also intervention reports written by the FE commissioner. The intervention process in colleges used to be more secret/private and, to support the point made above, there are definitely downsides from greater transparency in that airing financial problems in public hits confidence and therefore income.

DfE has increased its role as lender to colleges (including, under the 2017 college insolvency law, to the special administrator running them) and has probably ended up having to make a bigger loan because transparency has dented confidence than it might have been able to make in the alternative scenario under the old rules.