In the week of all weeks to bury bad news, HEFCE has gifted us a whopper. As previewed in this week’s Monday Morning HE Briefing, the council has released Financial health of the [English] higher education sector: 2015-16 to 2018-19 forecasts. While the report is listed as being merely ‘for information’, action is most certainly required by the whole sector – not just from those English universities covered by the scope of the report.

The forecasts were written before the result of the EU membership referendum, and therefore don’t have Brexit effects included in the modelling. Few think universities will be better off post-Brexit, and so the headline conclusions should be read with both the alarm that they inspire and perhaps an even more negative outlook for the future. And, because the forecasts were earlier this year, they haven’t priced in any further clamp down on international students.

The report’s headlines include:

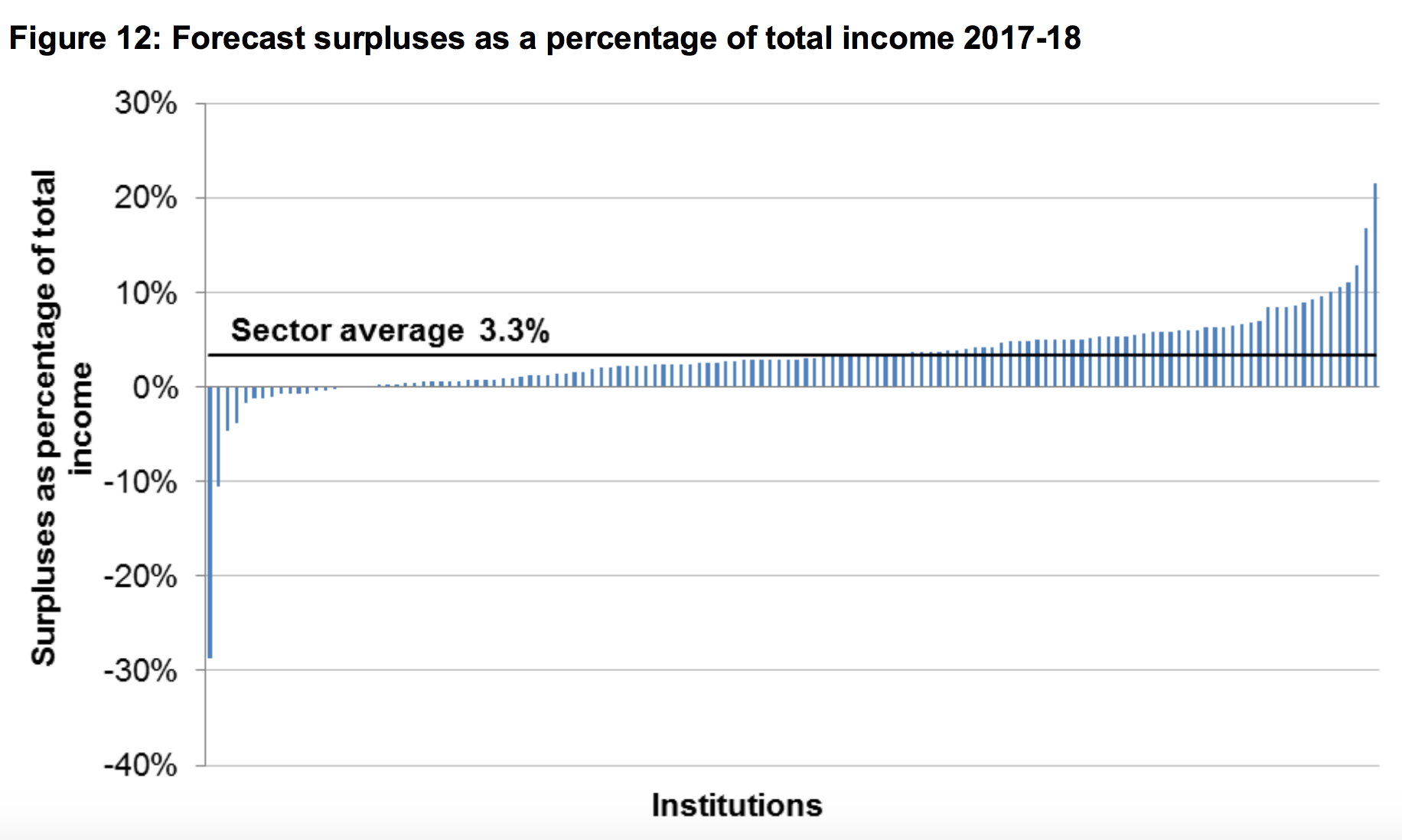

- University surpluses are projected at a minuscule 2.3 to 4.3 percent cumulatively across the period, masking wide variations from a deficit of 28.6 per cent to 21.5 per cent surplus.

- There will be more borrowing and falling levels of cash reserves. The number of days’ liquidity looks to fall from 127 in 2015-16 to a mere 83 by 2019.

- Total sector borrowing will reach £3.9bn by July 2019, and the sector’s total income should reach £32bn in the same period.

- Universities hope for an increase of fee income from overseas students (£4.8bn in 2018-19 versus £3.7bn in 2015-16), and to see growth in home and EU students of over ten per cent in the period.

- Singling out postgraduate home and EU students, universities are aiming for nearly forty per cent income growth.

- There will be significant capital spending, an average of £4.5bn annually.

- Pension liabilities grew by an eye-watering 45.8 per cent between July 2015 and July 2016, reaching a total of £7.2bn.

- There’s increasing volatility over the period, with a greater gap between the best and worst performers.

All of this makes for pretty grim reading, particularly for the institutions performing the worst. For example, the below chart shows how close to the wind some universities may be sailng.

There will, however, clearly be significant variability in the way exogenous factors impact upon individual universities, and these factors will also have their impact outside HEFCE’s purview.

The report identifies a list of serious threats to ongoing financial sustainability:

- The 18-year-old English population is declining.

- Brexit may have a severe negative impact on EU student recruitment, on staff visas and research funding.

- Degree apprenticeships may divert some students away from undergraduate programmes.

- There is the potential for further reductions in universities’ credit ratings, which would likely raise the cost of borrowing.

- There will likely be significant inflationary pressure on staff, operating and capital costs.

- The news on pensions is likely to get worse, with the largest scheme (USS, the Universities Superannuation Scheme) indicating a worsening deficit.

There is one very minor point which might be called a sunny upland, which is the potential for the weak pound to keep international student recruitment buoyant in the short term. In overly-polite terms, the report notes a certain level of ‘over-optimism’ in student recruitment projections. Cumulatively across the sector, these projections are not achievable. If you want a flavour of the seriousness, the report states that:

“Our financial modelling shows that removal of projected growth in overseas fee income over the next three years (2016-17 to 2018-19) would all but wipe out sector surpluses by 2018-19, with projected surpluses falling from £1,081 million (3.4 per cent of total income) to £56 million (just 0.2 per cent of total income).”

The report is damning, and the irony won’t be missed that it comes at a time when the role of the funding council in safeguarding the financial sustainability of the sector is being replaced by a ‘let the market decide’ approach. While the government has its oen logic for this approach and is implementing some measures to protect students in the case of ‘market exit’, it will come as a shock to universities that the oversight, guidance and practical – financial – support previously offered by HEFCE may no longer be available in their hour of need.

Indeed, it is new for HEFCE to use such strong and foreboding language about the overall state of HE. Previous iterations of these forecasts have been far more positive about the sector’s financial situation and have smoothed over cracks with reasonable rhetoric. But HEFCE is either no longer willing, or no longer able, to spin such a rosy picture.

The HEFCE report shows the grim state of affairs in which universities find themselves: the short-term diagnosis is one of stability – the 2014-15 numbers were healthy enough – but the prognosis is poor. Expect a need for some serious remedial action in board rooms across the land.

Find the full report here.

“7. No action is required: this report is for information”

LOL

Removal of overseas growth all but wipes out projected surpluses. Required reading then for the folks advising the PM

HEFCE has been producing these reports for years and they all include similar warnings. The report from 2011 noted that total staff costs were £12.1 billion in 2010-11. Five years later staff costs are £14.8 billion (para 50), which I calculate as a 22% increase over a period when there’s been a squeeze in this area in most of the rest of the public services.

HEFCE’s finance team is right to point out the clouds on the horizon (Brexit etc), to say that income may not rise in the next four years as currently forecast and also to note the wide variety between institutions but working in the English college sector I’m surprised to see surpluses of 2.3 to 4.3% of income described as “relatively small” (para 6b) and I wonder whether universities might need a different financial model that does not involve annual capital expenditure of £4.4 billion a year in the next four years – “50% higher than the previous four year average (para 6.9). Perhaps there”s a model involving fewer student residences, lower surpluses, tighter cost control and less pressure to keep raising fees. I realise this may annoy some of the 285,000 people working in HE (or the 306,000 due to be employed in four year’s time) but this site often discusses the lack of sustainability in the student loan system. There may, just possibly, be a connection to how the supply side in HE is set up.

Clearly not everything is rosy financially. Although universities have large landholdings (not discussed in the paper) and unrestricted reserves rising over the forecast period from £22 billion to £27.8 billion (para 87), it’s the rising USS pension deficit (predicted to rise from £5 billion to £10 billion, see para 82) which is the iceberg in this particular ocean for the older universities. Another argument for keeping staff costs under control is to tackle pension issues at source.