Do we spend too much time worrying about funding policy? You’re reading this on Wonkhe following the publication of yet another review of funding, so I’m guessing your gut response may be a no.

We’re all scrambling to work out how Augar affects institutional finances – I had a stab here. But how has the sector changed in size and shape since the arguably more substantial changes in 2012? The popular perception is that providers who can recruit have expanded and thus improved their bank balance. Others – struggling in a new competitive market – are beginning to find themselves in trouble. It’s a lazy generalisation that I know I’ve fallen into myself.

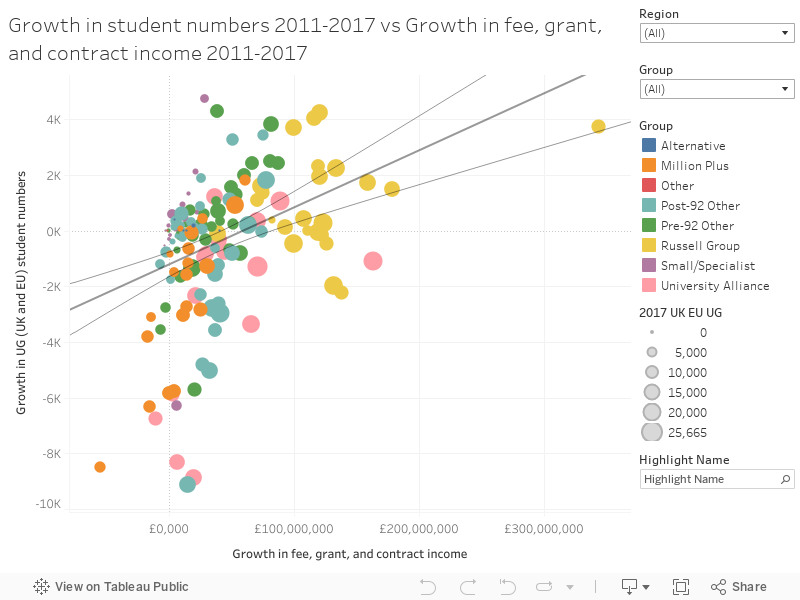

But the data – as data tends to – tells a much more interesting story. Here I’ve plotted the change in teaching income (tuition fees, funding council grants, and contracts) between 2011-12 and 2017-18, against the change in UK and other EU undergraduate numbers from the same period.

The size of the blobs relates to the total income for 2017-18, just to give you an idea of the relative scale of providers.

We see that the general trend is for financial growth, but you’d expect a correlation between student numbers and teaching income that just isn’t there. True, there’s no major undergraduate recruiters that are losing money – but a lot of those who have lost students have grown fairly substantially.

Who did well?

The Russell Group, and Coventry University, are powering out in front financially – but institutions as diverse as Aston, Harper Adams, and Swansea are matching them on undergraduate growth.

Those who lend to universities talk about a diverse income stream – what we are seeing here is gains by the Russell Group in international recruitment and post-graduate recruitment. Fees in these cases are not capped at all, and if you already have an in-built reputational advantage it would seem foolish not to make use of it.

But what of the many institutions that have lost home and EU undergraduate numbers over this time – are these being forced out of the sector by the invisible hand of the market? Institutions like Coventry, Oxford, Manchester, Manchester Metropolitan, and Sheffield Hallam are not struggling to recruit by any standards – some have become more selective, others have streamlined their offer.

I’ve eliminated the Open University entirely from this plot as an outlier. We all know what happened to part time study.

If you’d have asked David Willetts whether, in 2012, he expected this group of providers to shrink (on UK and EU undergraduate terms, at least) I very much doubt he would have answered affirmatively. The air war has always been about money following the student, and a demand-led change in the shape of the sector. For the students the UK government funds, this hasn’t happened.

For Wonkhe Podcast fans, we’re not seeing any kind of respectable correlation (R squared is a flaccid 0.15 – even looking at English providers only takes you up to only 0.16). I’ve plotted only providers in receipt of teaching funding – and where the data doesn’t exist, I’ve not plotted it.

You can also do some interesting things with UCAS application and accept data from the January releases (which doesn’t include offers, but you can bodge that in from the equalities dataset if you squint a bit), which gives some impression of the extent to which universities are forcing growth in the absence of increased demand, or letting increased demand be leveraged into selectivity rather than numbers. The app/acc ratio is not very meaningful in isolation – Oxbridge is only about 4 to 1 – but the changes are interesting.