Postgraduate study often passes below the radar of current debates in higher education.

Augar, for instance, has little to say about this part of the sector (for better or worse). Meanwhile, the absence of a centralised admission system for masters and PhDs preserves them, at least, from ongoing debates around post-qualification admissions, conditional unconditional offers, and so on.

Yet things were not always quite so placid.

A PhD proposal

Back in the halcyon days of 2014, postgraduate study was briefly a topic for the ballot box as George Osborne announced student loans intended to revolutionise the support for masters and, eventually, doctoral degrees. In fairness to the former Chancellor, the latter arguably have made a revolutionary change, marking the first time government finance has been universally available to any eligible student accepted to study for a doctoral degree (one thing the Student Loans Company won’t ask to see is your research proposal).

The hypothesis behind this original contribution to student finance was simple. The loans were intended to meet a demand for doctoral qualifications that was “outstripping supply” whilst increasing support for lifelong learning more generally. The question now is, do they pass examination?

Results chapter

The doctoral loan was introduced for new students commencing in 2018-19. The recent HESA release for that year means that at least some of the data on the loan’s impact is now available to write up. But the results seem mixed.

The number of students embarking on the first year of a doctorate increased by 5.5 per cent between 2017-18 and 2018-19, when the loans were first made available.

This is a bigger increase than in any recent year (2016-17 saw an increase of 2.5 per cent and 2017-18 an increase of 3.2 per cent). However, it’s nothing like the impact seen for the masters loans, which increased entrants to eligible courses by 31 percent between 2015-16 and 2016-17.

There are many potential issues with the masters loan (including those outlined on Wonkhe by Michelle Morgan) but it’s fair to say that they did dramatically increase participation in postgraduate study.

So, how surprised should we be that the doctoral loans apparently haven’t?

More data needed

The government’s consultation on the doctoral loan scheme – its literature review, if you will – received responses from universities, sector groups and individuals. But no specific attempt was made to measure the views of the people to whom the loans would be offered.

Research carried out by FindAPhD can begin to address this knowledge gap, being the first survey to examine the intentions, ambitions and views of people considering a PhD.

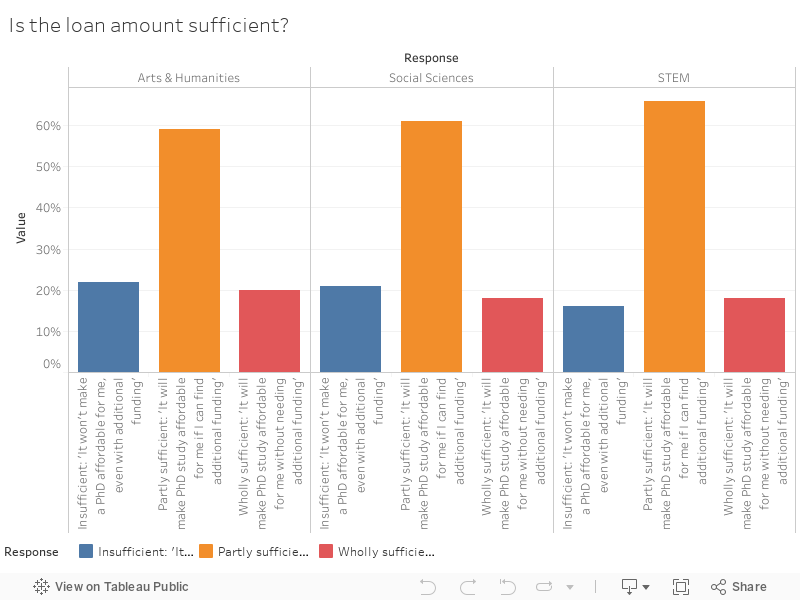

Amongst other things, we asked prospective students whether they thought the loan amount (£25,700 for the potential 2019-20 entrants we surveyed) was sufficient and how much difference it might make to their decision to study a PhD.

For simplicity, we grouped responses into broad STEM, social science and arts and humanities subject areas. The responses to the loan value were as follows:

Unsurprisingly, few people think a loan of £25,700 is sufficient to entirely fund a PhD.

However, over 20 per cent of social science and arts and humanities students feel that the loan is wholly insufficient and “wouldn’t make a PhD affordable, even with additional funding”. These are the subject areas in which – broadly speaking – students are more likely to be studying without full funding and for whom the loan is, in principle, a more attractive and useful option.

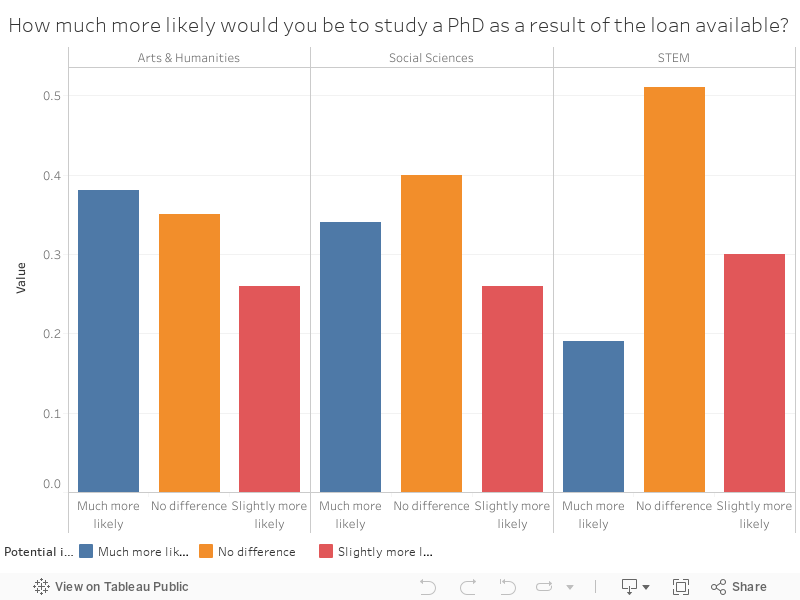

Non-STEM students are more likely to study a PhD as a result of the loan being available:

STEM students, on the other hand, are comparatively indifferent to the loan.

None of this is hugely surprising, but it could still be a concern. What the survey results seem to confirm is that doctoral loans have much more limited appeal in some subject areas, whilst those students who will avail themselves of this student finance aren’t necessarily convinced by it.

This matches my own experience, working in IAG for prospective postgraduates. I’ve heard students express surprise at the apparently arbitrary value of the loan (which, once fees are covered, leaves little more than £10,000 for living costs over three or more years) as well as confusion at the apparent lack of parity with UKRI funding; it’s one thing to take on yet more student debt, but understandably irksome when said debt leaves you with far more limited resources than fellow researchers who avoid it altogether.

Minor corrections?

The doctoral loans were introduced in response to relatively flat UK PhD enrolment. A 1.3 percentage point change suggests they haven’t succeeded in altering this.

A revise and resubmit decision feels unlikely, three years into the scheme’s existence, but minor corrections could be a possibility – particularly as the current government is clearly interested in reconsidering research policy and adjusting funding for priority areas.

There has also been a welcome increase in attention to the pressures faced by research students. Our survey reveals that the majority of prospective students are already concerned about the impact of a doctorate on their mental health, and more than a third expect to work over 40 hours a week – a situation that added (and potentially ineffective) student debt is highly unlikely to improve.

If the scheme (and wider funding landscape) is re-examined, that process should pay attention to the views of people considering a PhD as well as the data for those already doing so.

It would be interesting to see variations in take-up of the loan and responses to whether it made a PhD affordable by socio-economic background. We know from work on undergraduate support bursaries that having additional income whilst studying closes retention and completion gaps for students from low income groups. Are there more doctoral students from low income backgrounds under this regime than otherwise (as there are under Masters loans)?

Thanks Colin – I agree, and I’m sure we’ll get that information from DFE in due course, as per the Masters degree PGL. We didn’t ask questions about socio-economic background in this iteration of our survey, though we did separately ask whether students intended to work for additional income during their studies and were surprised (concerned, even) to see many planning to do so whilst also expecting a very heavy time commitment for their PhD. You can read more about that in our full report.

I suppose perception of the loan may be different to a bursary – but that’s assumption and anecdotal experience at this point.