How do UK politicians present fiscal and macroeconomic competence to the world? Through the public finance statistics based on the national accounts. Cutting the “deficit” and slowing down the growth of “debt” have been the central targets for governments of the last decade. They present a political narrative based on these targets and ask the electorate to judge them against that test: “to return the public finances to balance at the earliest possible date in the next Parliament”.

Simon Wren-Lewis complains about “media macro” – whereby broader questions about what led to the last financial crisis and how best to lead a recovery are traduced by targetry. Simplistic discussion about whether the deficit will be higher or lower under certain proposals crowds out reasoned policy.

And there is a further problem with targeting statistics in such fashion. It ignores questions about the composition of the headline figures. What exactly is the deficit?

In general, the deficit is captured by Public Sector Net Borrowing (PSNB), which measures the excess of total government expenditure over income. References to “government borrowing” and “the deficit” are therefore typically synonymous: we are talking about a shortfall that needs to be covered by money from elsewhere, borrowing that adds to the stock of debt.

But not everything that requires cash outlay counts as expenditure. And this is where student loans enter the scene. With an increasingly large place on the national balance sheet, they are attracting more attention in so far as they begin to distort the headline statistics significantly.

What is this quintessence of dust?

The government is now issuing roughly £16billion of tuition fee and maintenance loans annually, but this figure is not classified as expenditure. Instead, these loans are classed as “financial transactions”, which means that what gets counted as spending are the balance write-offs when they occur – in the main, decades after the loans were first issued.

This offers an enormous presentational boon for today’s government. That £16billion sits outside the deficit target for the time being (unlike grant spending on teaching or maintenance) and the costs of the current policy are only properly recognised in the mid-2040s. It is not just that loans are preferred to grants, because some repayments are projected to come back, it’s that the current accounting conventions make it seem as if loans are surplus generating, when (in real terms) they are not.

Based on national accounts cash figures, the Office for Budget Responsibility now predicts that repayments for this year’s cohort of borrowers will amount to £18billion in total and that £30billion of accumulated interest will be written off. Although those figures might make it look like the government expects to make £2bn over the following three decades and more (£18bn of repayments exceeds £16bn of outlay), this interpretation ignores what it pays out to finance the creation of loans. Once the government’s own cost of borrowing is factored in, the OBR claims that “total outlays and financing costs are expected to exceed total repayments for this cohort by £9.7 billion”.

It is important to pause here and stress that the government acknowledges that loans are subsidised and are expected to be expensive in the long-run. It lends the money to students through its Student Loans Company and it collects repayments when they come in. It has not asked someone else to disburse the cash with the promise that a future government will pick up the bill. All that’s at issue is when the costs are recorded. But given the centrality of the statistics to the political narrative and “media macro”, when costs are recorded has life beyond that paper exercise.

Is not this something more than fantasy?

Unfortunately, this is only the start of what the Office for Budget Responsibility (OBR) has called the “fiscal illusions” associated with student loans. Alongside yesterday’s publication of its annual, long-range Fiscal Sustainability Report, the OBR has published a working paper detailing its dissatisfaction with the current treatment of student loans in the national accounts.

[W]e use the term ‘fiscal illusions’ to refer to situations where fiscal aggregates (accounting measures of the budget deficit or debt) do not reflect the true fiscal implications of the transaction taking place. The illusion can be due to size – where the recorded flow is too large or too small – or timing – where flows are recorded at a very different point in time (past or future) to when a tax or spending decision was made. The treatment of student loans in the UK public finance statistics generates both sorts of illusion.

OBR, Student loans and fiscal illusions (July 2018) (para 1.6)

It’s a basic aim of accounting that the costs of decisions should be captured as transparently as possible, when they are made. As outlined above, the current treatment of student loans fails on that score. Matters are made worse because the government is able to record the interest accruing annually against outstanding balances as income, even though it’s almost all projected to be written off in 30 years (that £30bn figure cited above). This benefit to the deficit is not repayments made against interest, but the increases recorded in what is owed to government by borrowers (interest receivable, not interest received).

OBR, Economic and Fiscal Outlook, March 2018

Chart 4.5: Interest and dividend receipts: student loans versus other sources

The above chart, taken from the OBR’s last Economic & Fiscal Outlook (March 2018) illustrates the scale of this illusion. Since post-2012 loans arrived – with their real rates of interest – we can see a sharp jump in student loan interest “receipts”.

In 2017/18 this amounted to £3.2bn and meant that the government finally hit one of George Osborne’s original targets. By 2022/23 it is projected to reach £7.5bn. The OBR elsewhere derives a more complicated assessment of the overall problem:

The illusion grows steadily from 0.6 per cent of GDP (£12.8 billion) in 2018-19 to 0.7 per cent in 2022-23 (£15.7 billion) … roughly equal to the margin by which the Chancellor was meeting his fiscal target in 2020-21 in our most recent forecast. (para 5.9-5.10)

The perversity of this situation can be illustrated with the following thought experiment. Were the government to introduce a year-long moratorium on all student loan repayments, the deficit would benefit in the short-run. Repayments go down and long-run costs go up but there would be more interest accruing against outstanding balances – hence more income today!

This observation combined with the deferral of write-off expenditure explains why Theresa May’s costly decision to raise the repayment threshold on post-2012 loans from £21,000 to £25,000 per annum can be consistent with deficit reduction. As long as the interest accruing is roughly the same, there is no short-run hit to the deficit, despite the massively increased long-run costs. The additional expenditure only turns up in the form of write-offs, thirty years and more down the line.

Illusions and Identities

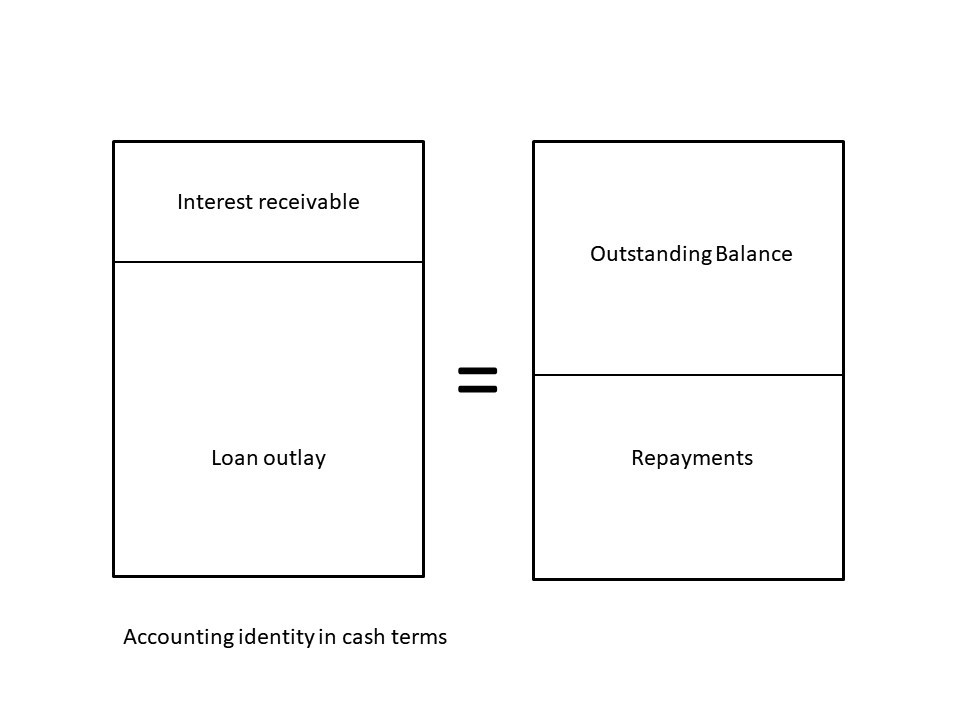

This treatment of interest and write-offs is intimately connected – and results from – the classification of student loans as “financial transactions”.

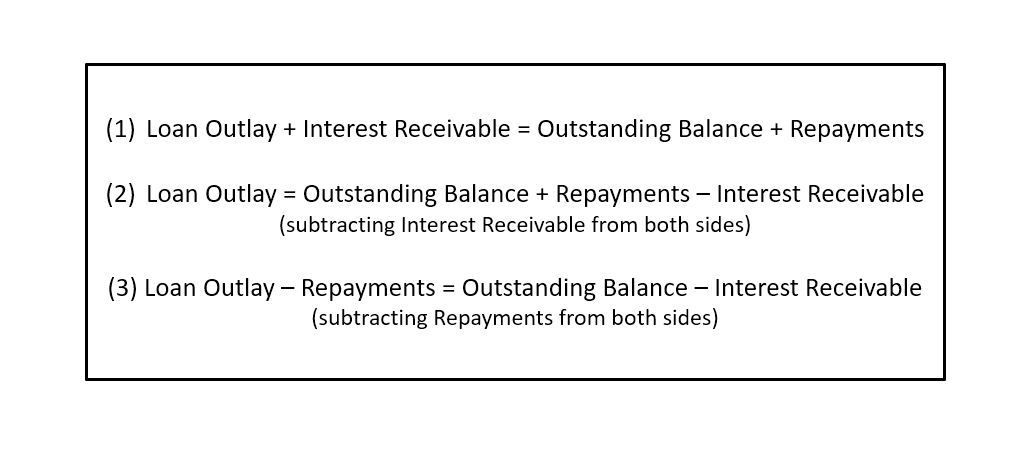

In cash terms, there is an accounting identity. For any specific loan: outlay plus interest receivable must equal outstanding balance plus repayments.

If outlay or interest increases, but repayments stay the same, then the balance increases to make up the difference. If repayments reduce or increase, while interest or outlay stays the same, then again the balance must respond in equal and opposite direction.

As a result we are able to do some simple algebra:

In our final equation (3) either side can be taken to define the cash loss on loans issued (allowing for the fact that the government’s costs of borrowing is already being recorded separately in the deficit). One could either treat outlay as expenditure and repayments as income or treat interest receivable as income and the write-offs of outstanding balances as expenditure. When the account is finally closed, the cash totals would be identical. But before then, the differences in timings and amounts are stark.

For the first option, outlay would score as expenditure when the loans are issued (spending upfront), with repayments (income) coming over the following years. In contrast, the current treatment of loans uses the second option, which flatters the deficit until the interest being recorded as income is offset by write-offs at the end of the loan period. There is no difference in long-run costs, but here presentation is everything.

Were we look at a graduate tax with identical cashflows, then we would have to use the left-hand side. For loans (financial transactions), we get to use the right-hand side.

And for standard loans that makes sense. The essence of commercial loans would be misrepresented by the left-hand side. Even with interest-only loans, annual repayments match interest. And on standard loans write-offs are not planned, but arise when debts go bad. But our income contingent repayment loans are such that annual repayments are always below interest accruing and large write-offs are a policy principle.

Once we move from a single loan issuance to a rolling programme with an ever-growing “book”, the fiscal illusions loom large.

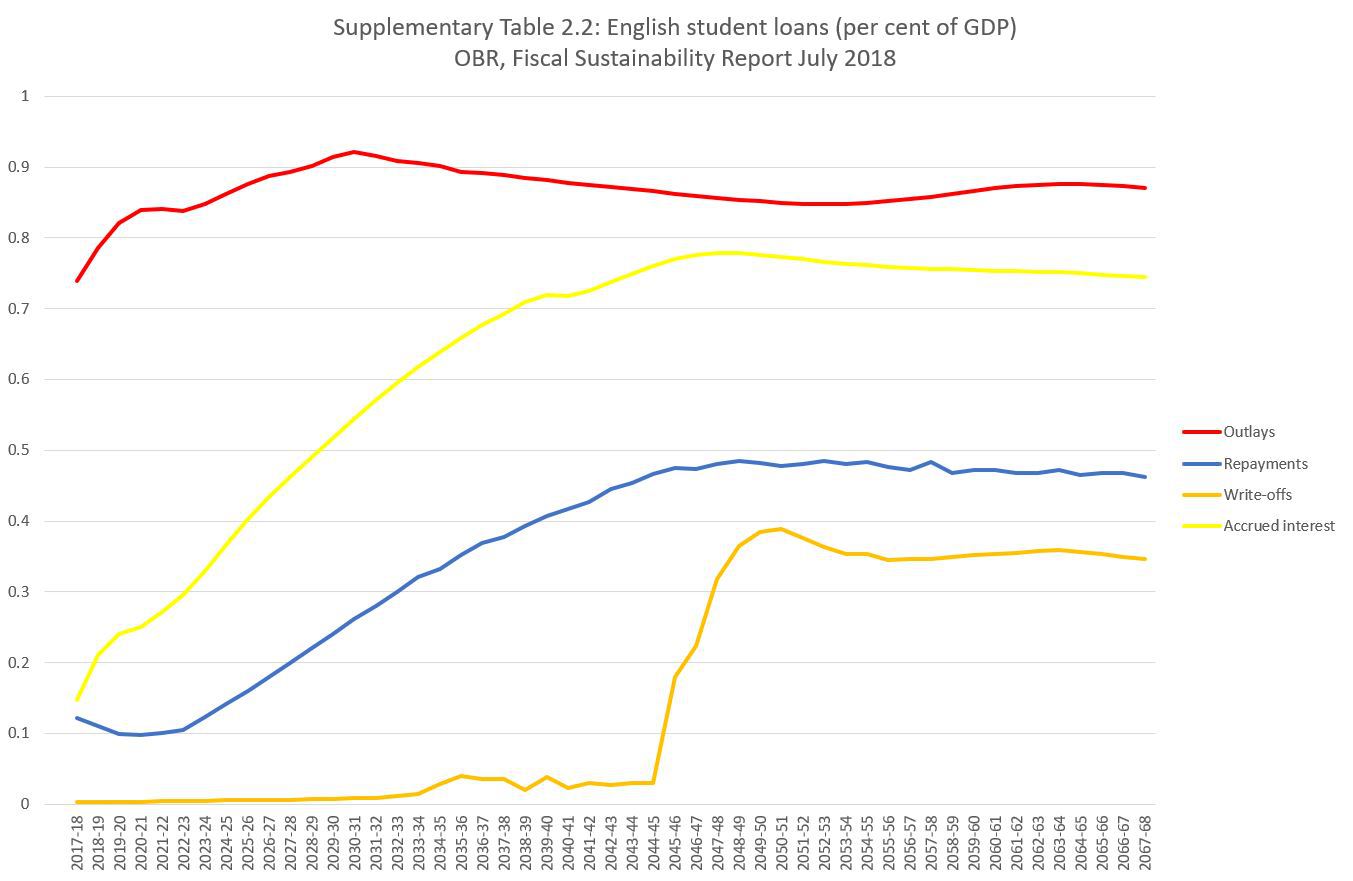

In the chart below based on the latest long-range OBR forecasts, loan transactions are plotted annually as a percentage of GDP (currently £2,000bn pa so that 1% is the equivalent of £20bn).

Supplementary Table 2.2: English student loans (per cent of GDP)

OBR, Fiscal Sustainability Report July 2018

Compare the red and blue lines. Each year’s outlay is always greater than annual repayments from all existing loans. Expenditure would always be above income: the loan scheme loses money and this comparison using the left-hand side of the equation above reflects that fact, though in the early years the scheme would look more expensive than it is.

Now compare yellow and orange. Accrued interest is always greater than repayments and always greater than write-offs, even when the latter finally arrive in the 2040s. But note here that the sign of our equation is reversed: income is always greater than expenditure. The policy write-off of one cohort is always less in-year than the interest accruing on the balances of all open accounts. This makes the loss-making loan scheme look surplus-generating: so the deficit always benefits from this illusion. (Factoring in the debt interest paid by the government makes both alternatives worse, but still leaves the financial transaction presentation much better off).

OBR summarise this problem in a key paragraph:

[W]hen these write-offs begin they are more than offset by the interest capitalising on the larger loans taken out by later cohorts. The write-offs do mean that the deficit is flattered to a smaller extent (0.4 per cent of GDP in 2050-51), but they do not reverse the illusion as they do when considering a single cohort. This means that so long as the student loans system continues in its current form, the fiscal illusions associated with new cohorts of loans will outweigh those that are reversing for cohorts reaching the point where write-offs begin.

This pyramid of fiscal illusions means that the deficit will always be flattered despite the system barely breaking even in cash terms and costing significant amounts after the interest cost of financing the loans is included … . (my emphasis)

OBR, Student loans and fiscal illusions (July 2018) (para 3.17)

The Office for National Statistics

The national accounting treatment for loans is well-established and governed by European System of Accounts (ESA). It is the responsibility of the Office for National Statistics (ONS) to prepare the UK figures. Yesterday, ONS also released a report. “Looking ahead: developments in public sector finance statistics” is the first in a planned annual series detailing “major pieces of methodological work” likely to have “material impacts on the fiscal aggregates”.

A third of this report is given over to the recently announced review of its treatment of student loans following parliamentary committee reports this year calling for changes. The ONS accepts that “the current recording over-simplifies the underlying economic substance of these loans”. The specified treatment for commercial loans is clear, but the decision to treat student loans in the same way is likely to be altered. This requires work with the ONS’s international partners to extend current guidance adequately.

Chiefly, the ONS have now spotted that a key ESA definition for “what constitutes a loan” may be failed by income contingent repayment (ICR) loans: “There is an unconditional debt to the creditor which has to be repaid at maturity.”

First, we know that outstanding balances are written off at “maturity”, not repaid. Second, income contingency may constitute a conditional debt: you only have to repay if you earn over a specified amount.

From what has gone before we can see that there is a strong desire for ICR loans to continue to be recognised as loans, but with some revision to the official guidance. Removing ICR loans from financial transactions entirely would mean reverting to the left-hand side of our equation: having initial outlay count as expenditure. This would make loans appear much more costly than they really are, another illusion.

Alongside that rejected possibility, the ONS outlines three other alternative approaches, including bringing forward the projected write-offs as an expenditure item today, either for the whole loan issuance or those loans which are not expected to be repaid. (There are some intricacies to be navigated here which I have discussed elsewhere.)

OBR has modelled three of these proposals along with two of its own. Confusingly two different proposals are modelled by ONS and OBR as “Approach 2”. The ONS’s Approach 2 – which involves removing the interest illusion – seems the most feasible, but it would not involve recognition upfront of the cost of the policy in the way that is desired by the OBR.

An aside: as national accounts operate with cash figures, it is not possible to take the “RAB charge”, a net present value, from departmental accounts and plug it in here. Similarly, the government’s cost of servicing its debt is already scored separately in the deficit as expenditure and so any attempt to represent long-run cost upfront would need to avoid double-counting. And that’s not to mention the practical hurdles of using estimated figures that then need to repeatedly revised over the years.

It is not possible here to detail and analyse all the various proposals put forward by ONS and OBR. But the crucial questions are:

- Will HE appear to be more costly today as a result of these changes?

- What will it mean for the scope of the current HE review?

- Will Theresa May’s threshold largesse now have to register as spending today in the national accounts? (DfE have been granted an additional £14.7billion this year to deal with the revaluation of new and existing loans, but this departmental budgetary allocation doesn’t figure in the national accounts).

ONS indicates that it is “hopeful” that an agreed treatment can be found by December. If the new treatment is complex, then implementation may not be established before financial year 2019/20. In any case, if what does and does not count as spending is altered at that point, then it makes sense for the post-18 review timings to shift in order to accommodate this development.

What warlike noise is this?

In coverage today, The Times declaims that this ONS review has wrecked the “Brexit war chest” and will leave Hammond’s fiscal rules “in tatters”. It is important to view things a bit more calmly: the long-run cost of loans will not be changed by this development, how and when that cost is recognised will.

The paper suggests that Hammond will have to implement a “new standard”. Loan write-offs are capital expenditure; should projected write-offs be brought forward the deficit could be repositioned in terms of the Current Balance (Current Expenditure minus Income) rather than PSNB (Total expenditure minus Income). There is less scope for change if the interest illusion is removed as that is income, but this strikes me as the key illusion to eliminate.

There is an opportunist argument for the status quo, which would be adverse to spending being presented differently. No one in the sector or government will be too keen on HE suddenly appearing more expensive. But the current treatment is not robust — that is now officially recognised — and we shouldn’t forget how generally unpopular the fee-loan regime is.

We shouldn’t want fiscal illusions, and we definitely don’t want such illusions determining policy. Whatever the short-term conniptions, it is important to remember that the root of these issues is “short-termism” and “targetry”. In that context, the unreasonable sway of accounting treatments have arrogated reasonable policy of its sovereignty, and even drawn us into what outsiders (and some insiders) view as madness. Hopefully the HE review can benefit from a sea-change: alternatives that had been ruled out for being too costly become much more feasible once the presentational advantages of loans are removed.

Thank you once again, Andrew, for helping me get my number- phobic brain around complex financial ideas!

Very nice and profitable article!

You make some good points about how to understand student loans in the national deficit that I never thought about.

thanks for sharing!