Across the sector, there is deepening concern about the finances of universities.

Industrial action over pay and workloads has shifted from an occasional “act of god” to a permanent fixture; restructures and rounds of redundancies resulting in reduced programme portfolios are announced almost every week; and concern is growing over the pace and rate of international recruitment as a way to plug the growing gap between income and costs.

On the front page of the Guardian a couple of weeks ago, vice chancellors warned that the current funding model for UK higher education is “broken”, prompting the Department for Education in England to point out that universities are independent from government:

This means that universities decide their business models and oversee issues such as admissions, staff recruitment and pay.

But in some parts of the higher education sector, things don’t seem quite so tough.

You can find the statutory accounts of a particular sort of private provider of higher education on Companies House, and once you’ve looked at several, you will start to see a pattern of very successful growth in the last few years.

A typical example of one of the larger providers might have turned over c.£50m in one year – all from course fees. Costs may be £10m or so in wages plus several hundred thousand pounds paid to its highest-paid directors and overall profits posted at £20m. Then £10m or so might then be paid out in dividends. Nice work if you can get it.

Despite the fact that this sort of provider will likely be delivering mainstream undergraduate and postgraduate programmes from major name universities, you won’t find them on the Office for Students register.

Their finances can’t be found in HESA figures; they’re not subject to the regulator’s public interest governance principles; and applicants can’t find how well they do on student satisfaction or graduate outcomes. And the individuals that own them are getting rich off the back of the public student loan system.

So what’s going on here?

This group of private higher education providers are growing rapidly in number, expanding in size and broadening the number of partnerships with registered universities that enable them to deliver higher education. And that £50m figure in fees is the sort of turnover you can expect to see after the franchising universities have taken their cut.

I’m not talking here about FE providers operating franchised courses for universities, and nor am I talking about the significant number of small and specialist providers on the register that might focus on the performing arts, or theology, or a particular science – some may even be for profit. I’m talking about a group of providers that tend to offer business and health courses, usually franchised from universities, operating in large urban centres. And, as we have discovered, are using sales techniques that most of the HE sector would not recognise.

The Oxford Business College was the focus of a recent feature in the New York Times headlined “‘Pass Him’: How a British For-Profit College Made Millions.” The article said that the college and others like it “make millions, largely by recruiting immigrants,” noting that they operate “in an opaque corner of the British education system.”

It raised questions over how students are recruited, the level of oversight from regulators, and the academic standards applied to both admissions and outcomes.

But how opaque is this area? And should we be concerned about the money, or the way students are being recruited – or is this merely a sign of the times?

Pull up to the bumper baby

Last year a friend of mine was strolling through a Midlands shopping centre and came across an interesting pull-up banner.

“Claim your £15,000 funding today” said the headline, which said that you could get a “degree in many fields”, that “no formal qualification” was needed and that you could study for just “two days a week”. Its funding pages stressed that prospective students could access loans of up to £15,000 – and that students could “contact one of our counsellors to give you best advise [sic].”

I was wondering which university was recruiting in this way – but a visit to its website revealed that it wasn’t a university, but rather a domestic agent – which I later found was recruiting staff on Facebook to sell what officially are full-time courses into specific communities.

Potential sales staff were told that the role involved selling in venues like shopping centres, that it was a “very easy product to sell”, and that preferred applicants would benefit from having “door to door” sales experience.

Meanwhile, in Emma Bubola’s NYT story:

Join a university without any qualification and get up to 18,500 pounds,” one advertisement on Facebook reads, listing no school, only a phone number and the money figure, which is about $23,000. Dozens of similarly anonymous posts appear on Facebook groups for Eastern Europeans in Britain. “Do you want to study at the easiest university in U. K.?” asks another ad. “Do you need additional income?”

Then a month or so ago, I was idly scrolling through TikTok when for whatever (presumably algorithmic) reason I was offered an advert that featured a man, seated at a desk, who said the following to camera:

I have an amazing opportunity for all of you guys. So if you are aged between 18 to 55, and you have never studied at university before, our company UACB can help you get back into education with some of the universities that we work with.

You don’t need any previous qualifications to study. Classes are two days a week, and four hours per day. So in total only eight hours a week. Classes are flexible and can be done alongside a full time job. If you have children, you can take your classes during school hours, and the universities are extremely flexible.

Also, whilst studying, you could get up to 15,000 pounds per year paid directly to you from Student Finance. You don’t need any previous qualifications. And if this is something you’re interested in, get in touch via the form below and we can help.

I thought that the £15k claim was interesting. Was it referring to postgraduate funding? Or maybe it meant other aspects of maintenance funding besides the core loan – a comment below asking about the money was responded to with:

Student finance maintenance loan, plus grants such as the: Parent learning allowance, Adult dependent grant and special support grants.

The Department for Education’s guidance on advertising HE courses doesn’t talk about agents at all, international or domestic. Neither does the CMA guidance on students and consumer protection law. But there are now plenty of these domestic agents operating – and presumably, they’re not working for free.

A search for “higher education funding” in the TikTok app brings up multiple links that list agents promoting law, business and health courses without a provider. One leads students to a WhatsApp mobile number for more detail on courses that its videos suggest offer significant career and salary benefits. Another lists a large number of university partners and a large number of programmes – just not the satisfaction or outcomes that might be associated with those programmes.

Some would argue that the nature and content of advertising higher education on social media, in shopping centres or door to door – especially when the focus often seems to be on the cash value of the maintenance support available from the state or the relatively low demands placed on students to attend – is a problem.

Others argue that doing so is OK, and a good way of reaching students who otherwise might not have considered university.

Either way, the NYT piece suggests it works:

…college recruiters walked immigrant neighborhoods, knocking on doors or stopping people in shopping malls, selling the merits of a business-school education and adding a surprising offer: Get paid to enroll. “Money, money, money,” said Stefan Lespizanu, a former recruiter for Oxford Business College. “Everybody was saying, ‘Hey, push the money.’”

The question is partly about whether the advice – especially when it’s advice that is ostensibly about a long term financial commitment – is accurate and fair in a situation where the advice and information around student loans is not regulated in the same way that other loans are. But the question is also about what is being advertised, and how.

A bridge to sell you

In theory there are strict rules governing advertising anything, let alone three year higher education courses. Anyone selling something online or even via a pop up banner is supposed to behave in a way compliant with standards governing advertising and affiliate marketing in the UK – most notably the CAP Code and The Consumer Protection from Unfair Trading Regulations or “CPRs”.

One aspect is that any commercial relationship between a person/entity promoting a product/service must be disclosed. Another is that it’s supposed to be clear what is being sold, and who the ultimate supplier is. One case required commitments that any communications would:

…include a prominently displayed statement which would be unavoidable to the average consumer, that the promotion has been paid for or otherwise remunerated.

That’s why, in the BUILA Good Practice Guide for UK Education Agents Partnering for Quality, agents are told that being mindful of the regulations involves being:

… honest about the commercial relationship you have with your educational institutions, ideally through a signed contract with them. You do not need to state the value of your commission, just that you receive a commission for helping a student to enrol at that institution and that that pays for a defined set of services you will provide the student.

But the BUILA code – which also involves standards in offering objective course information and providers carrying out due diligence and mystery shopping activity on agents – is about international agents, not domestic ones.

And very few of the over 50 agent websites, YouTube videos and other material I’ve seen appear even to be partially compliant. Many don’t list the universities being advertised, some advertise the franchiser but not the franchisee, some offer incorrect or out of date information about student finance, and hardly any of them disclose that commission is being collected by the agent.

Most feature photos of attractive students and glittering facilities from image libraries rather than the campuses and courses they promote. Many suggest their motivations are about matching students to the right courses – often without revealing the single or short list of providers they’re collecting commission from. Almost all are keen to promote the student loans available to applicants.

I’m looking at one now that has a string of “success stories” that involve helping students get into “the university of their dreams”. Each of the photos of students accompanying the stories show up on a reverse image search as being from stock image libraries. And the actual programmes listed on the “courses” tab all come from a single, for-profit franchised-to provider that is running degree programmes for one of four large universities.

In 2020 the Office for Students began a review of admissions that promised to interrogate the practices of international agents – and Home Secretary Suella Braverman has launched a fresh look at their tactics as part of changes to immigration rules. But we’re not aware of any focus on what seems to be a growing group of agents operating in the UK that are recruiting domestic students.

If nothing else, this largely unnoticed and unregulated industry deserves some scrutiny from regulators and/or policy makers. Just as we are concerned with lettings agents as well as landlords, it feels like we ought to be concerned about what these agents do, how they do it, who they do it with, and the amount of money they make when doing so.

And crucially, if we are to assume that the reason that this type of recruitment tactic is being deployed is that it reaches disadvantaged students, many would argue that it is even more important that accurate and impartial information is on offer to those applicants both from those doing the selling and those doing the regulating.

Making good choices

In the DfE guidance on transparency in advertising, the stated aim is to ensure that any potential applicant to a higher education programme can use data to inform their decision making. It’s an aim that’s also very much a part of the Office for Students’ work – making sure that prospective students “have good information to guide their decisions” through initiatives like DiscoverUni or the TEF.

In fact, combining good and accurate information with minimum threshold levels for continuation, completion and progression – regardless of the entry qualifications, value added or social background of applicants – are the two central ways in which the regulatory system is supposed to protect the interests of students. It’s how the sector is able to assure itself that where a student fails, either in the short term or long term, that’s on them rather than the provider in that partnership.

On franchising, some years on from launch it is still the case that OfS’ promise in the regulatory framework – that the subcontracting a provider does will be listed in its entry – is missing. But interestingly, buried in the Office for Students’ B3 outcomes data – which got an update back in April – we are now at least able to see more than we could in the past.

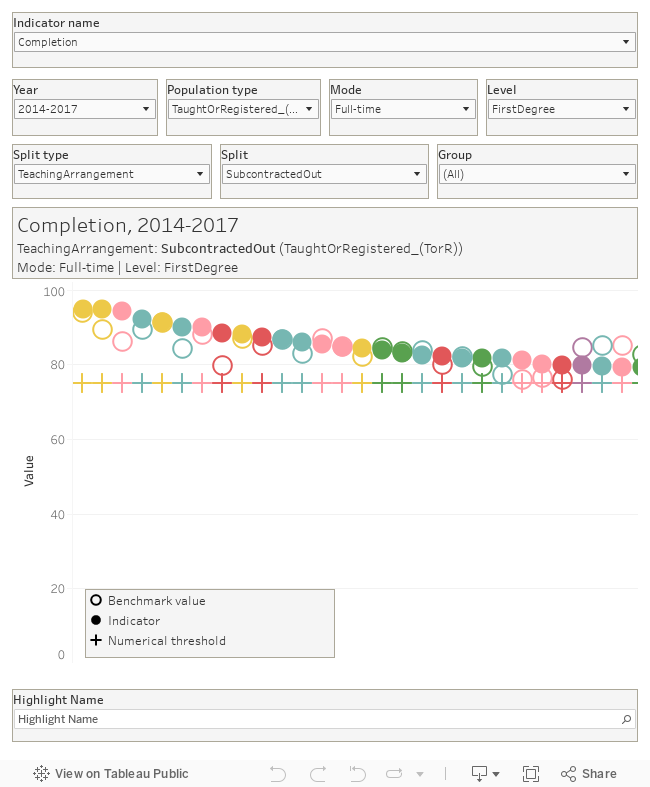

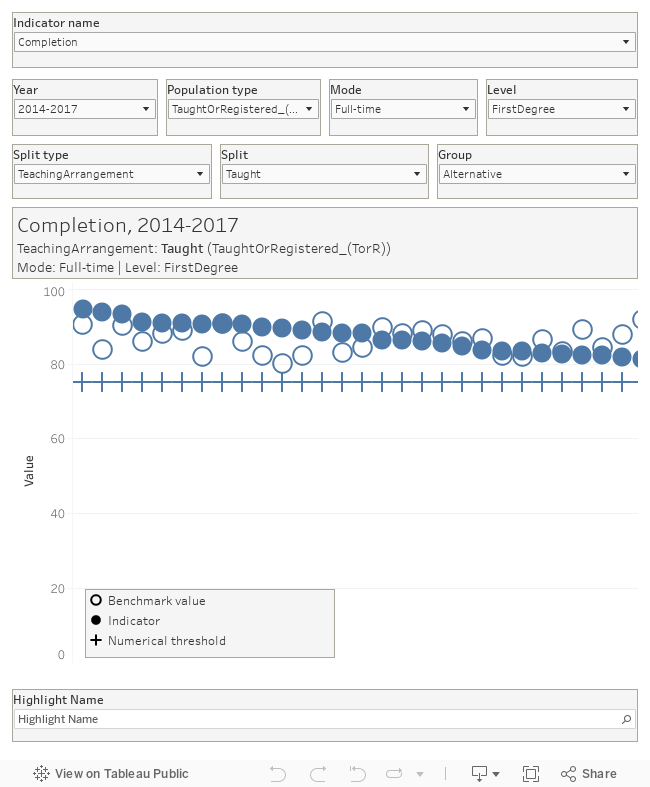

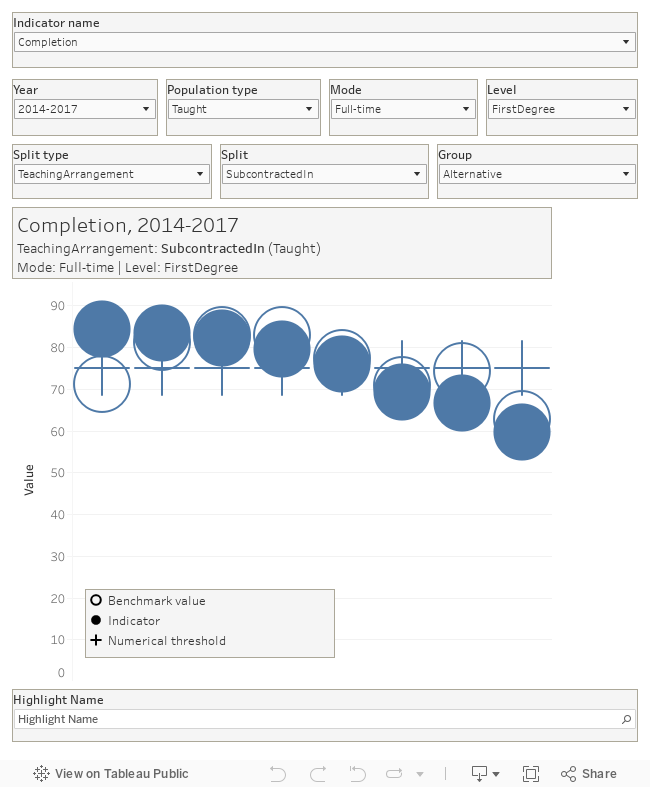

The first iteration of the data gave us some detail on the performance of registered for-profit HE in the three outcomes measures. Now we have some split data on the performance of the provision that is subcontracted from one OfS provider to another – from the optic of both the franchiser and the franchisee.

Here my colleague David Kernohan has built a data viz which lets us explore the OfS B3 (outcomes) data in more detail. For our purposes, we are able to see the performance of providers on all three key measures from four perspectives:

- All of the registered students with a provider, both those who are taught by it and those franchised out

- The performance for the group that is franchised out

- All of the students at a provider that are taught by it, both those registered with in and those franchised into it

- The performance for the group that has been franchised into it

The year drop-down reminds us that OfS uses “smoothed” figures covering multiple years. Mode and level are what you think they are; and split type and split cover the splits that you’ll be familiar with (like ethnicity or subject area) and the franchising options outlined above. If you are having an explore yourself, note that splits are variable by “population type” (taught or registered, or just taught) – and there’s also a filter allowing you to examine various common groupings of providers.

Below the surface

If we take full-time, first degree undergraduates, we can first see the overall performance for the provider that does the teaching. Filtering out FE providers and specialist provision, that gives us a list of for-profits whose outcomes are below thresholds as follows:

| Continuation | |

|---|---|

| Threshold | 80% |

| ICON COLLEGE OF TECHNOLOGY AND MANA | 64.7% |

| NELSON COLLEGE LONDON | 66.7% |

| BLOOMSBURY INSTITUTE LIMITED | 66.8% |

| GLOBAL BANKING SCHOOL | 69% |

| MONT ROSE | 69.6% |

| RICHMOND, THE AMERICAN INTERNATIONAL | 72.7% |

| LONDON SCHOOL OF COMMERCE & IT LIMITED | 72.9% |

| BRIT COLLEGE LIMITED | 72.9% |

| ARDEN UNIVERSITY LIMITED | 73.8% |

| NAVITAS UK HOLDINGS LIMITED | 75% |

| UCK LIMITED | 76.7% |

| WALTHAM INTERNATIONAL COLLEGE LIMITED | 78.4% |

| RNN GROUP | 79% |

| SAE EDUCATION LIMITED | 79% |

| LONDON SCHOOL OF SCIENCE & TECHNOLOGY | 79.4% |

| Completion | |

|---|---|

| Threshold | 75% |

| BLOOMSBURY INSTITUTE LIMITED | 50.8% |

| ARDEN UNIVERSITY LIMITED | 56.8% |

| GLOBAL BANKING SCHOOL LIMITED | 59.7% |

| RICHMOND, THE AMERICAN | 60.5% |

| BPP UNIVERSITY LIMITED | 62.8% |

| RTC EDUCATION LTD | 66.7% |

| LONDON SCHOOL OF SCIENCE & TECHNOLOGY | 68.3% |

| BRIT COLLEGE LIMITED | 69.3% |

| NELSON COLLEGE LONDON LIMITED | 72.4% |

| SAE EDUCATION LIMITED | 73.5% |

| Progression | |

|---|---|

| Threshold | 60% |

| NELSON COLLEGE LONDON | 38.1% |

| BRIT COLLEGE | 38.2% |

| ARDEN UNIVERSITY | 39% |

| LONDON SCHOOL OF SCIENCE AND TECHNOLOGY | 40.4% |

| MONT ROSE COLLEGE | 48.5% |

| REGENT'S UNIVERSITY | 51.6% |

| LONDON SCHOOL OF MANAGEMENT EDUCATION | 52.4% |

| BLOOMSBURY INSTITUTE | 57.8% |

These providers would likely make both value-added and WP contextual cases for these results, as Bloomsbury did in its legal battle with OfS a couple of years ago. But we might well ask the question if OfS is looking at them at all, when the regulator’s “boots on the ground” approach is cloaked in secrecy and focused on providers with larger cohorts as they provide the bigger overall risks.

From an applicant point of view, many of the programmes at these providers are either too new or too small to show up properly on DiscoverUni – and these providers don’t seem to be in a hurry to telegraph their institution level performance for the three metrics.

Get a degree from a renowned UK university

Next we can use DK’s chart to see the private providers’ overall performance on franchised in provision – which usually carries the imprimatur (and sometimes the data of) the university that subcontracted the programmes.

This time you’ll see that OfS has supplied sector level performance for franchised in provision too – and in each of the three cases the overall sector performance is hovering dangerously close to the allowable threshold level of performance.

And that means that while some providers are above that threshold, some are below it. Again, filtering out the FEC and specialists, those below are:

| Contracted in FT, FD, UG | |

|---|---|

| Continuation | |

| Threshold | 80% |

| Sector | 80.2% |

| GLOBAL BANKING SCHOOL | 69% |

| LONDON SCHOOL OF COMMERCE & IT LIMITED | 72.9% |

| BRIT COLLEGE | 72% |

| NAVITAS UK | 75% |

| WALTHAM | 78.4% |

| LONDON SCHOOL OF SCIENCE & TECHNOLOGY LTD | 79.2% |

| Contracted in FT, FD, UG | |

|---|---|

| Progression | |

| Threshold | 60% |

| Brit College | 38.2% |

| Mont Rose College | 50.1% |

| Regent’s University | 51.6% |

| Contracted in FT, FD, UG | |

|---|---|

| Completion | |

| Threshold | 75% |

| Sector | 78.6% |

| Global Banking School | 59.7% |

| RTC Education | 66.7% |

| Brit College LTD | 69.3% |

Again, this is data applicants almost never see in this form, and we don’t know if any regulatory boots have been near these providers’ ground.

There is an interesting problem in the above figures, by the way. OfS splits out the data for students subcontracted-to providers on the register and a “sector” total, and you might have assumed that said sector total is… the total of those providers.

But in the “sector performance” figure above, students franchised out to providers not on the register are included. So when we say “here are the private providers performing below the threshold”, we can’t include unregistered ones – because while OfS has the data, and includes it in the franchising from figures, it doesn’t publish it in the franchised to numbers.

This all means, by the way, that a regulatory system designed to only allow access to the loan book that has two categories (approved and “fee cap”) can be entirely bypassed by a private provider as long as it can find a university willing to franchise some provision to it.

It also means that a provider in the “approved” category can in fact run programmes charging the upper fee limit of £9,250 as long as a university cab be found to take responsibility for its outcomes.

More means worse?

Next, we can see things from the point of view of the franchising providers. This is interesting because it might be that provision franchised out has worse outcomes than that delivered directly – something applicants are rarely told.

Much of this may be franchised to FECs and specialists as well as generalist private providers, but below threshold we have:

| Contracted out FT, FD, UG | ||

|---|---|---|

| Continuation | ||

| Threshold | 80% | |

| Subbed out | Taught | |

| UNIVERSITY OF WORCESTER | 29.7% | 89.1% |

| ST MARY'S UNIVERSITY | 39.1% | 84.3% |

| UNIVERSITY FOR THE CREATIVE ARTS | 53.9% | 87.7% |

| UNIVERSITY OF NORTHAMPTON | 64.4% | 88.9% |

| WRITTLE | 71.1% | 87.9% |

| UCLAN | 72.3% | 86.7% |

| BIRMINGHAM CITY UNIVERSITY | 72.7% | 90.3% |

| LONDON METROPOLITAN UNIVERSITY | 73.9% | 77.8% |

| LEEDS TRINITY UNIVERSITY | 75% | 88.9% |

| THE UNIVERSITY OF LEICESTER | 75% | 94.8% |

| Contracted out FT, FD, UG | ||

|---|---|---|

| Completion | ||

| Threshold | 75% | |

| Subbed out | Taught | |

| LONDON MET | 58.2% | 75.6% |

| THE UNIVERSITY OF EAST ANGLIA | 67.1% | 93.5% |

| ROEHAMPTON UNIVERSITY | 67.6% | 79.5% |

| THE UNIVERSITY OF WARWICK | 68.7% | 96.4% |

| UNIVERSITY OF YORK | 72.2% | 96.3% |

| ANGLIA RUSKIN UNIVERSITY | 72.5% | 85.3% |

| Contracted out FT, FD, UG | ||

|---|---|---|

| Progression | ||

| Threshold | 60% | |

| Subbed out | Taught | |

| UNIVERSITY FOR THE CREATIVE ARTS | 41.4% | 58.4% |

| KINGSTON UNIVERSITY | 41.7% | 71.2% |

| THE UNIVERSITY OF EAST ANGLIA | 42.2% | 74.4% |

| UNIVERSITY OF CHESTER | 43.3% | 68.6% |

| UNIVERSITY OF THE WEST OF ENGLAND | 50% | 75.2% |

| ROEHAMPTON UNIVERSITY | 50.9% | 63.1% |

| TEESSIDE UNIVERSITY | 51.3% | 73.3% |

| UNIVERSITY OF BRIGHTON | 51.4% | 74.4% |

| UNIVERSITY OF NORTHAMPTON | 58.4% | 70.8% |

| STAFFORDSHIRE UNIVERSITY | 59.1% | 67.4% |

[Full screen] (or as an alternative view)

Of course the percentages hide that the populations in each case can be quite small. But there’s no escaping that nationally there’s a circa 10 percentage point gap on all three measures between taught directly and subcontracted out:

| Sector: FT, FD, UG | ||

|---|---|---|

| Taught | Franchised out | |

| Continuation | 90.9% | 80.2% |

| Completion | 89.3% | 78.6% |

| Progression | 71.6% | 63% |

Some would argue that the WP-focussed nature of the recruitment in much of this activity will necessarily deliver worse outcomes but still a strong value-added. Others might retort that the idea of WP is the mixing of those from different backgrounds – not the posh kids at the campus university and the poor kids in an office block on the outskirts of London or Birmingham.

For universities grappling with the freeze to the unit of resource, rising costs, and unpredictable student demand, franchising provision through private partners can present itself as financial good sense – with a bonus for boosting access as well.

But arguably, a university topping up both its access figures and budgets through this kind of work, only for the evaluation outcomes to be worse, misleads applicants. As Emma Bubola notes in the NYT:

Many of the partnerships are new, and it is difficult to determine whether they help students land higher-paying jobs after graduation. The data, in general, is murky.

And so, as Bubola points out, that means for providers like the Oxford Business College, applicants can’t actually see the real performance for the provider they’re enrolling into:

Regulators do not conduct checks on partnership deals, and academic data is not broken out by franchise agreements, making it hard to tell how students perform. No public data exists on how many students each partnership has or who the partners are. The Office for Students said on Thursday that it was working to improve partnership data to help improve regulation.

Discover the data

Meanwhile, Discover Uni, provided by the Office for Students on behalf of the whole of the UK using the Unistats dataset, is a real mess when it comes to new, franchised, validated, satellite campuses, or small courses.

Sometimes Discover Uni aggregates out by saying things like “data displayed is from students on other courses in business and management”, but doesn’t say whether it means other courses in business and management at that franchised to provider, or in the university doing the franchising from.

And despite CMA guidance making clear that students should get information on who they are contracting with, pages like this – on the “official source” of course information run by the regulator – don’t mention the franchising university at all.

These problems with presentation and the way in which they aggregate back to bigger data sets (see the bottom of this page for an explanation) have the effect of often sending signals with unwarranted clarity to a prospective student – about the sort of satisfaction or outcomes they might reasonably expect if they enrol there, for that.

Come to interview, bring your passport

All of this may be fine, but what of the actual recruitment processes – and the academic standards on the programmes that support the outcomes?

In the NYT piece the claim is that even applicants who plagiarised answers on admissions tests were given a second chance or, in at least one case, put forward for admission, according to internal messages among the interviewers, who tested the applicants’ English.

He copied and pasted his answer from an online source,” one interviewer wrote in a text message to his supervisor. “Pass him,” she replied.

And as Bubola notes:

In an October memo about fraud risks, England’s higher-education regulator, the Office for Students, said that partnership agreements were at risk of exploitation. “Students may be registered without appropriate checks that their language qualifications and skills are genuine,” it wrote. Students may be pocketing living-expenses loans, it added, “without any intention of meaningful study.”

When I applied for a programme at a different provider off the back of that shopping centre banner, I was invited to go to interview, got given the interview questions by the agent, and was even sent a list of suggested answers.

When I went to the campus, a receptionist in the “admissions” team seemed keen to see my passport – and even keener that I set up a Student Finance England account – all before I could even have a conversation about the course. Answers to questions that I posed on outcomes were vague. And I deliberately attempted to flunk the written assessment – but got the following message on WhatsApp the following day:

Well done James. You have passed the interview and assessment. More than 55% student decline on this important stage. College is waiting for your passport. Please provided us it asap.

These are not the only questions, of course. We haven’t scratched the surface of what is being provided on the margins that the various sets of accounts suggest – what sort of facilities or student support is on offer here. It’s often hard to tell which policies apply where, and whether things like hardship funds or cost of living initiatives on offer in the franchising universities are reaching these providers. Maybe these providers are simply very efficient, delivering great services while still able to return big profits to their owners. The point is that from either an applicant’s point of view, or from looking at the data, we don’t know for sure.

Whether we’re talking about recruitment tactics, the profits being made by some private providers, the available information to applicants or the quality assurance and enhancement regime that operates across English higher education, there are real questions here about what is being done and how, as my colleague Mark Leach argues on the site.

They’re questions that the sector and its regulator in England should address quickly – before a fresh wave of reputational damage comes.

++++++++

On the way courses in England are advertised, an OfS spokesperson said:

Prospective students should have access to good quality information, advice and guidance to help them apply for a course which suits their needs and ambitions. Universities and colleges – and any agents they appoint to act on their behalf – quite rightly have the freedom to decide how best to market their courses. In doing so, they should ensure they are meeting the OfS’s regulatory requirements around consumer protection, as well as consumer protection law more widely.

A HEFCW spokesperson said:

Our Quality Assessment Framework sets out how we assure ourselves that the quality of education, or a course of education, provided by or on behalf of regulated institutions meets the needs of those receiving it. This includes, as baseline requirements, that providers meet their obligations under consumer law, as set out by the Competition and Markets Authority, and that they align with the Expectations, Core and Common Practices of the UK Quality Code. We work with the other UK funding Bodies to support the Discover Uni site which brings together data and information based on other sources.

++++++++

We amended this article on June 13th to reflect that where B3, TEF and A&P indicators refer to registered students (including when incorporated into the “taught” or “registered” population view) they are reporting on all students registered at the provider in question, inclusive of those subcontracted out to registered and unregistered providers. Outcomes and experiences for students subcontracted to unregistered providers are included in TEF assessments and benchmarks this year – but only in relation to the assessments and benchmarks of the student’s registering provider. Where OfS dashboards or data released refer to “sector” this is consistently defined as “OfS registered providers” – so any student who is either taught or registered by an OfS registered provider is included throughout any/all of the sector totals.

I am not sure that this is surprising. An additional concern for me is whether there are providers with higher than expected outcomes that might be trying to avoid scrutiny by doing some ‘interesting’ things behind the scenes. The OfS is even less likely to notice them as their dashboards won’t highlight them as a risk.

Well this is all a little depressing, not least because it’s a lot of deja vu. Many of the issues hinted at here are the same issues that came up in 2013/14. There was a relatively robust response within the regulatory and legislative architecture at the time.

The article asks if regulators boots have ever been on the ground at the providers mentioned – which is exactly what the Public Accounts Committee was asking BIS and HEFCE a decade ago. The response was to set up a joint unit (which I jointly led) and I can confidently say hand on heart that in a year we’d visited every “alternative” provider up and down the land (yes, even those in Scotland, Wales, and Northern Ireland) that were directly claiming student support, some more than once as needed. We also saw action being taken, regulatory action in todays parlance, with providers seeing their designation suspended or limited in some cases.

So this is all possible to manage and manage closely and carefully, and I believe it proved to be effective, and I know many of the colleagues in the independent provider sector thought the same. It doesn’t have to be a murky corner of the English HE system as could be inferred from this and the NYT article.

One of the potential drivers of franchise activity was of course the student number control, which persisted in APs until 2018, despite being abolished before that in HEFCE funded providers. Therefore there was a clear incentive for providers to seek (both the franchisee and franchisor) such arrangements – and indeed I was in more than one meeting with providers (with my boots on their ground) where the lightbulb came on when this became obvious to them. But validation agreements were messy, and we’ve heard sector stakeholders particularly on the independent provider side highlight how problematic they’ve been. They are sadly sometimes entered into without full due diligence, or, more importantly, the level of necessary ongoing diligence from the validating institution. It’s this latter point that is crucial, and again I have seen many a time where this has been kicked down the road or into the long grass to the detriment of all concerned.

I’m hopeful that any response to this is sensitive and proportionate. Provider context is important, but so is maintaining quality and standards. But in the past we’ve seen knee jerk reactions that risk chaos, and behind all of these numbers there are real people, real students, who are studying at these institutions and trying to so their best. Let’s hope some proper focus is, once again, given to this area.

Rob, are you still following this thread? Has anything positive happened in the last few months since this article ?

I think there is a real danger here and the facts provided justify a major and immediate investigation by OfS.

By all means phone me if this is easier/ 07973192712

Brilliant that you’re looking into this as this is such a dark corner (actually much bigger than a corner) of HE. I had a couple of interactions with institutions which offer franchised/validated degrees. One was beautiful, small, doing excellent work with students who wouldn’t normally access higher education. The other – a corporation staying out of any OfS registers, NSS results etc. You wouldn’t know they exist but they have thousands and thousands of students. Great profits but at high cost to staff and students. Practices you wouldn’t see at any university or provider which is on the OfS register. Quality is not a consideration in any activities.

And somehow, this and other similar places exist. Sad to see what students are getting for their tens of thousands of pounds. Makes me want to leave the sector altogether knowing that this is allowed to go on.

I normally am a bit sceptical about OfS approaches but truly hope they’ll start looking into these matters more seriously. Students and staff deserve better.

Dear WONKHE

As an academic who now works in the private sector, having previously worked for 20 years in a Russell Group and Post ’92 HEI’s, this article challenges my values and principles, and I am tired of the witch-hunt instigated by some of the sector who chose to get into bed with some unscrupulous providers without proper attention to due diligence. Now those providers have cast a dark shadow on the alternative sector, which makes me sad. The article NYT cites concerns relating to practices at Oxford Business College. Please note that all private providers are not the same.

Regardless of the provider standing in the world of HE, our colleagues at WONKHE need to remember that the sector for many years has been about ‘bums on seats’ and £££ that it brings (and don’t get me started on the covert efforts of HE’s up and down the country to raise their NSS).

Last Friday I attended a celebration for our successful level 6 students and Alumni. I was completely moved, as was the Lord Mayor of B/ham, by the stories of resilience, and newfound empowerment from students who would have never even got a foot over the threshold of the rest of the ‘not for profit’ HE sector.

Great that you are shining a light on this hidden corner of HE. Would also be worth showing, in student numbers, the size and recent growth trajectory of some of these providers – I expect eye opening in some cases. The big question being, if such providers are able to attract thousands, or in some cases, tens of thousands of students, what is the gap in the market that they are addressing? Let’s hope it’s not people without the necessary preparation for HE study.

https://feweek.co.uk/contracts-risk-for-provider-after-ofsted-finds-students-who-never-studied-with-the-firm/

But what has DfE and OfS done to providers such as Waltham International College who were exposed to have fictitious students by fe week and Ofsted. They are still working with Leeds Trinity University and OfS registered but badly exposed by Ofsted. Hassan Ashraf is the Director of WIC, Surein Rheeder is Principal, Parvez Jugon is Vice Principal and Rajib Mustofa is Academic Manager. Is law going to address colleges like WIC?