What are tariff groups and why do they not matter?

David Kernohan is Deputy Editor of Wonkhe

Tags

Maybe it is something to do with the cold weather, but a lot of people over the last couple of weeks have been asking me about university tariff groups.

Specifically, people want to know who is in each group – who is a high tariff provider and who is a low (or even no) tariff provider. You see terms like this used in reports and data releases all the time but the actual membership of these groups needs to be derived from suspicion and insinuation on behalf of the reader.

A tariff in this context is simply the average number of UCAS points held by UK domiciled first year entrants to a university (where tariff points are available). UCAS has a handy tariff calculator if you are interested in exploring this wild world further.

UCAS doesn’t publish a list of universities by average tariff – neither (in the open data collections, at least) does HESA. The only official publication I know of comes alongside the annual Department for Education Widening Participation in Higher Education statistics. You need to download a table marked “tariff groups.csv”.

But why would you do that? Stepping back for a moment, the entire idea of an average provider tariff is absolute nonsense. Different courses at each provider attract different tariffs, so at least some of the “average tariff” of a given university must be derived from the mix of subjects it offers. There is also a national dimension – because Scottish entry qualifications are dealt with generously in the UCAS tariff calculation there are (officially) no low tariff providers in Scotland.

For me, it makes lots more sense to look at tariffs at a subject level – it’s what underpins the British Academy work on cold spots in arts, humanities, and social sciences. So with the kind help of HESA, I’ve plotted some of this data.

First up, here’s a list of tariffs by subject – I’ve used CAH2 as a level of resolution, and you can also filter by region and nation (ILTS1). The dots represent the average tariff for 2022-23 entry for that subject, the small lines illustrate the difference between that subject area’s average and the average tariff for that provider.

By default we are looking at allied health – I’ve added upper, lower, and middle terciles to approximate the familiar high, low,, and medium tariff groups. Note that this only applies to the subjects in question: the bands will move if you change the filters.

You can see that the University of Plymouth, the University of the West of England, and others not traditionally considered “high tariff providers” sit near the top of the list here – illustrating that subjects do really matter when it comes to tariff.

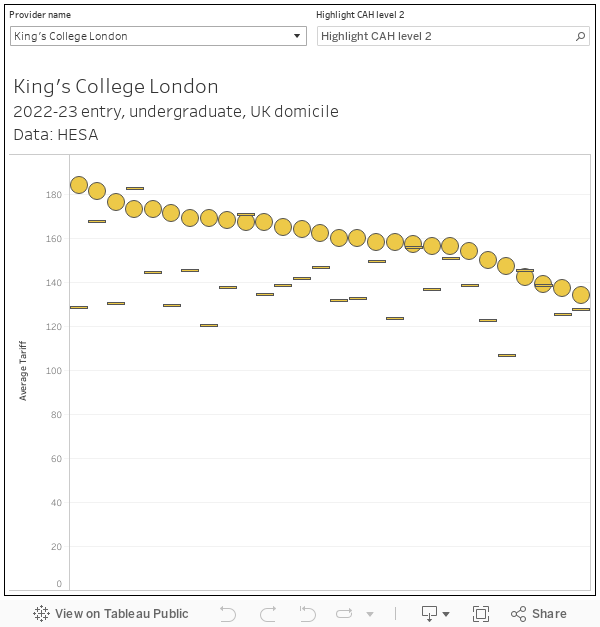

It’s also helpful to look across an individual provider. This chart shows the tariff by subject area at each university or other institution – the dots show the actual 2022-23 tariff, the lines the average tariff for that subject area.

If we look at King’s College London, for example, we can see that average subject area tariffs vary by around 60 points (more than an entire A level at grade A*) with computing having the highest tariff, and sport sciences the lowest. Notably medicine is not the highest tariff subject there (though it is in most providers) – indeed KCL has a below average tariff for medicine this year.

Why might this be? Well, KCL does a lot of excellent work in outreach, and may well be making contextual offers for some courses. Though this, for me, is a very good thing indeed (if you believe that one sweaty afternoon in a school gym is the perfect and eternal measure of academic potential, please take a ticket from the machine and wait by the door until your number is called) such equitable admissions policies have the side effect of making your tariff look lower. There is a case to be made for defining “tariff” as “how much a university loves formal examinations”.

Another point to remember is that these groupings are only valid for one cycle – if a university dropped entry tariffs to fill spaces left by declining international recruitment (to take one example) they may find themselves in a “lower” tariff group in years to come.

Note: some providers do not permit onward use of data outside the usual open data tables, these are not shown here. Rounding applies, which means results may differ slightly from other more sophisticated datasets.

While I accept there are many issues with a whole provider tariff based classification and that it only tells you about one aspect of a provider’s provision it’s one of those things where something is better than nothing. Dumping all providers in one pot is useless and provides very little insight so something is needed, there is an excellent publication from the OfS on this which explains their typologies which are pretty sensible (but then I would say that), you can find it all here https://www.officeforstudents.org.uk/media/905cacf5-a733-4e21-b49f-67aad785e610/provider-typologies-2022_dec2022-update.pdf. Of course if you have a better solution to classifying providers I’d be the first to support it.

Is something always better than nothing, Richard? If the ‘something’ is partial, and potentially misleading, I’m not sure that’s true. It appears to be quite a popular argument with OfS (“well, it’s something, and it’s the only thing we’ve got”) but I’m yet to be convinced that this is a sufficiently strong position. Even more to the point: having identified a “better than nothing”, people tend to think that’s enough, and stop trying to improve it to get to the status of “possibly quite useful”.

I don’t have a terribly strong view about tariff groups, but there are more legitimate questions about which data gets used, and how, than is acknowledged here, in my opinion

Hi Richard. As it happened we had a go at building one a few years back – I even tried (with the support of most sector agencies) to convene a working group to get this sorted in a consistent and data-driven way, I believe there was one significant sector hold out who insisted on going it alone but I can’t remember who that was.

The publication you mention was quite good (I wouldn’t go as far as excellent) but it was last updated two years ago and quite a lot of things have changed since then in the data. Also OfS seem to have stopped using it, which has arguably made things worse.

If you are serious about wanting to come up with sensible and defensible provider categorisations owned by the sector and used by everyone (including algorithms to auto-update them year on year) I’d be up for that, as would many others in the sector and media. As I say, most sector bodies are keen to be involved.

This is a great resource for deep diving but I have a question about the data.

Am I correct in thinking this is reported data on the actual tariffs students joining a 1st year programme have? How do universities that facilitate access to HE/have a social mission fit here (you note KCL medicine above)? i.e. are/where are Foundation Year and Access to HE routes (which inherently would have low ‘tariffs’) incorporated or does the data solely show tariffs for those entering via the traditional school > sixth form > A’Levels > 1st year pathway?

Good question Marc. This is all UK domiciled students for whom tariff data is available entering the first year of undergraduate study in 2022-23.

So if you have tariff points and you are starting your first year undergrad (level 4) you are in the data. This will include people who progressed via a foundation year, but as the FY itself is not tariff bearing we get instead the highest tariff (mainly because nobody can agree what level a FY is!) bearing qualifications: generally those used on entry to the FY the previous year.

However, the averages will include Access to HE (as that is tariff bearing), and other entry qualifications such as BTECs, AQA technical, the international bacc, and T levels. Also unlikely things such as music qualifications at grades 6, 7, or 8.

Thanks David. I do love the data you and WonkHE produce and always find it useful.

The above might explain a few things – like one of your examples above offers a specific BSc degree with an FY and non-FY option. The MINIMUM tariff for non-FY is 112 (to 128) but the AVERAGE tariff for the subject area in the data is 100. Without knowing the % progressing and numbers constituting the 1st year cohort it would be hard to be clear on this, but it seems a reasonable supposition the FY intake are a factor in that data.

Looks like further data would be useful but difficult to collect and analyse. In this data though, some institutions that have used FY provision to meet their social mission and/or increase student intake may render with a lower average tariff than they actually offer for pure 1st year entry. Equally some institutions without FY/Access to HE may have stated entry tariffs but reduced them in practice. Would need to compare to historic data to fully understand the picture, and even then it will be subject to interpretation.

Suspect a lot of staff in a lot of institutions will be examining and producing their own narratives on this!

Just to flag I looked at some of that stuff (including the available UCAS data of various sorts on tariff) in an article specifically looking at pharmacy courses recently. You also see some course level data via the unistats release, and I know I have plotted that a few times (usually around results day) It is fascinating stuff, and something I hope to dive further into in months to come.

David – I am not sure how your data back your argument. With few exceptions, like the Nursing subject you picked as an example, the distribution of institutions is very much as one would expect. Largely Russell and pre-92 typically on top followed by post 92s and others. See for example Law, English, Politics etc

As you correctly point out there is variation within institutions so there is no surprise that KCL top subjects have a significantly higher average tariff than the lower. Yet KCL scores (significantly) above average in the overwhelming majority of the subject it deliver. So being in the top quartile for tariff points in the large majority of subjects should suffice to classify the institution as high tariff

Indeed there are some subject areas that have narrow sector tariff ranges, students are typically local to the area (e,g, Nursing) or attract students with very diverse qualifications that make them look a bit like “anomalies” but I don’t think it changes really the fundamental principle of the tariff classification.

We need to use the tariff classification as a practical tool that helps data analysis not a labeling of some other value.