As per Wonkhe’s Monday morning scoop, Secretary of State for Education Bridget Phillipson has announced that the maximum undergraduate fee and the maximum maintenance loan for 2025–26 in England will be allowed to rise by forecast inflation (OBR, RPIX, Q1 2026) of 3.1 per cent.

It means that the headline £9,250 fee will rise to £9,535 for standard full-time courses (£11,440 for full-time accelerated courses and £7,145 for part-time courses). The cut to the headline max fee for foundation years which we spotted in last week’s Budget has also been put in writing – £5,760 for standard full-time courses, and £4,315 for part-time courses.

Lower fee rates will still apply for those delivered by approved, rather than approved (fee cap) providers. It’s hardly worth saying this, but there will be no link between fee levels and the outcomes of the most recent Teaching Excellence Framework (TEF), despite the legislative cover for this still being on the statute book.

For graduates, there will be no difference in monthly outgoings as a result of these changes. As currently, around 30 per cent of graduates (those with the lowest lifetime earnings) will not repay loans in full.

And although many will conflate the rise in fees with the very real concerns about student hardship, graduates – not students – repay loans. This package overall represents limited but welcome good news because of the increase in maintenance loans – although the failure to update the threshold over which we ask parents to chip in continues to blunt any increases on the maintenance side.

It’s also worth noting that the announcement of rates for fees and maintenance usually includes the same percentage uprating for PG loans and max Disabled Students Allowances – it’s notable that neither are anywhere to be seen in today’s announcement. One to watch.

In the commons

Phillipson’s statement was pretty much a greatest hits of the mood music issued so far on the sector – removing barriers to opportunity, recognising higher education as vital to the nation’s culture, economy, and global reputation.

She remixed the “look at the mess we found” thing for universities, talked of the “neglect” that left universities under-resourced and students struggling (and international students feeling undervalued), and reiterated the decisions on the “refocusing” of the Office for Students.

In theory, two announcements were made – the first on fees and maintenance, which included a “more efficient delivery at a lower cost is necessary” line on carrying forward the foundation years cut.

The second promised “proposals in the coming months”, which we are told will cover:

- Linking investment with major reform across universities and public services – growing and strengthening higher education’s role in the economy, communities, and the country

- Spreading opportunities to disadvantaged students by expanding access and improving outcomes

- Universities adapting to technological advancements

- Support for adult learners through increased flexibility for retraining

- A commitment to elevating teaching standards

- Ensuring all students receive good value for their investment

- Driving national growth by attracting global talent

- Collaboration with Skills England, employers, and further education partners to deliver necessary skills

- World-class research to create good jobs nationwide.

- Universities embedding themselves within local communities – civic anchors and integral parts of local life, moving away from being perceived as “ivory towers.”

- A renewed focus on efficiency, ensuring effective use of funds supported by students and taxpayers. Preventing wasteful spending and justifying top executives’ (that’s VC to you and me) pay

No surprises there – a mixture of what we’ve heard in the manifesto and since, and feels like someone has run their finger down Universities UK’s Blueprint index page to tick the boxes.

To the extent to which the increase may not be enough – and to the extent to which some providers are being helped quietly – there was no public announcement. There’s also no sign of Sharia-compliant loans.

Both the opposition response and questions from MPs brought the usual rag tag of “when I was a student” or “I have a university in my constituency”.

Of note, the question from Rachael Maskell (York Central, Lab) yielded a commitment to set expectations of universities working with local authorities over housing supply, and the one from Luke Meyer (Middlesbrough South and East Cleveland, Lab and former QAA staffer) brought a commitment to work with OfS on quality issues.

Vikki Slade (Mid Dorset and North Poole, LD) thought that courses offering 8 hours of contact time ought to be cheaper. Phillipson’s intro had discussed “promises not being kept”, and again we got a commitment to work on those issues with OfS “in the coming months”.

Fee increase – institutional impact

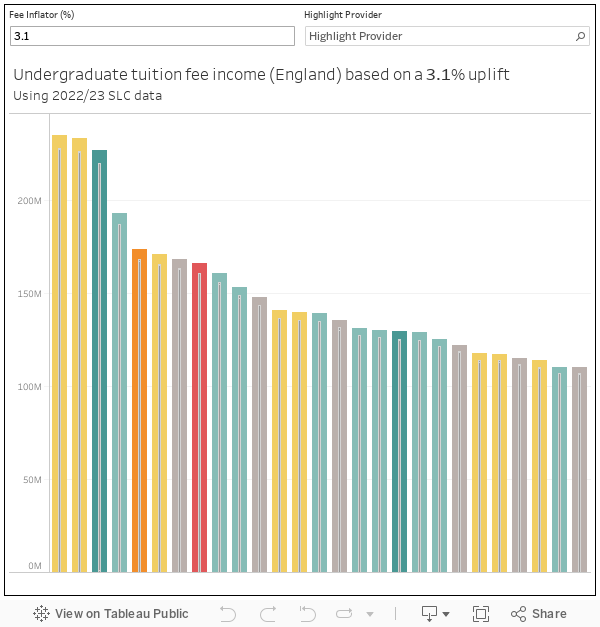

In all, the fee uplift of 3.1 per cent represents around an additional £300m of undergraduate tuition fee income – as against £10bn worth of fee income and £49bn total income in 2022-23.

It’s not possible to directly break down the exact value of the increase by provider, but we can use 2022-23 undergraduate fee income from the Student Loans Company to give an indication of what is involved. For most large providers, the increase is equivalent to between one and two per cent of total income.

As an inflationary uplift the impact of this rise is to maintain the spending power of fee income at current levels. It halts additional pressure on university finances next year – but we should not be expecting universities to have additional spending power next year to invest in salaries, maintenance, or student support.

And of course this doesn’t take into account the extra costs in the employers’ national insurance rise, nor the cut in fee income that many will face via the cuts to foundation year fees.

For this dashboard, we’ve have modelled by default a 3.1 per cent increase in undergraduate fee income – you can see the impact of other levels using the box at the top left. You can highlight providers of interest using the box on the top right, and when you mouse over one of the bars you are able to see 2022-23 tuition fee income levels alongside fee income as uplifted, and total income in order to calculate proportional impact.

Fee loans [Full screen]

It also assumes that everyone will be able to increase their fees for all students immediately. Some providers may not have mentioned fee increases for continuing students in their contracts at all, and others may have committed only to increasing fees for new students. A messy patchwork of approaches has emerged in Wales since its max fee increase earlier this year.

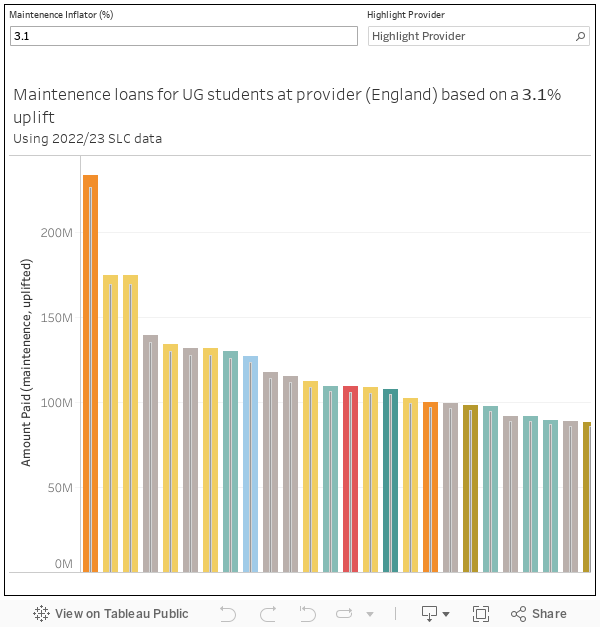

Maintenance by provider

The amount of maintenance loans that undergraduate students can access is determined by family circumstances, living arrangements, and whether or not the provider they study at is based in London. Aside from that geographical impact, the choice of provider of course has no impact on access to support.

Because maintenance loan access is in itself an indicator of disadvantage, it does not track fee loans as you may expect. If you plot maintenance loans by provider you can get a sense of this – providers that take a particular interest in recruiting from economically disadvantaged groups will see a larger volume of maintenance loans allocated, while places that recruit from well-to-do groups will be recruiting students that will be able to access less loans (or may choose not to take up what they are entitled to.

This dashboard works in broadly the same way as the one above, but shows the volume of maintenance loans paid to undergraduate students.

Maintenance by provider [Full screen]

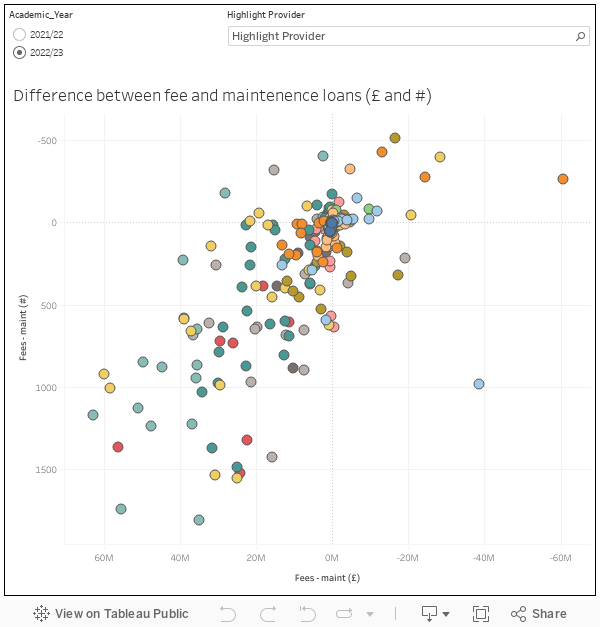

One continually puzzling artefact of this data release is the question of the small number of providers where more students access maintenance loans than access fee loans (to the extent that the value of maintenance loans significantly exceeds the value of fee loans made in a given year).

If you think about it, such a phenomenon makes very little sense. Some students do not take any loans at all for religious reasons (and because fifteen years on the government still hasn’t come up with a Sharia compliant loan system), some are from backgrounds advantaged enough to be able to pay for fees and living costs up front. Many more will take out fee loans, but will either have very limited access to or choose not to take out maintenance loans because of a higher parental income.

The mystery graph [Full screen]

We’re interested here in providers in the top right quadrant – where the number of students taking out fee loans is lower than the number of students taking up maintenance loans, and the value of fee loans is lower than the value of maintenance loans.

The impact of an across the board increase in loan amounts is consistent across the sector. It makes it even more important that the government and regulators can be sure that every penny of this very limited additional income is supporting legitimate students in accessing high quality education. Questions such as those posed in this chart, and concerns around the quality of provision delivered via academic partnership, need to be urgently addressed.

It might be worth emphasising that the reduction in fees for Foundation Years is for ‘classroom-based’ subjects only. There is a list of what those are on the DfE website.