With this being the season for UCAS data, and various prognostications being offered on the fate of the sector as a result, following last weeks first analysis, we thought it was time that we took a detailed look at the UCAS cycle – what it is, what we know about it, and how to understand the underlying trends.

Our visualisation allows you to take an in-depth examination of institutions or groups over two years (2016 entry and 2017 entry), and includes exclusive data from our friends at Hotcourses that offers another angle on the changing popularity of institutions.

The absolute basics

When a person wants to study at a higher education provider, she would (usually) apply through UCAS by mid-January of the year she wants to start. For some courses and some institutions, there are later (or earlier) application deadlines – and UCAS Extra may allow for further applications later on. After receiving an application, the institution may then decide to make an offer (generally in the spring), which may be accepted (as a main or insurance choice) in the early summer and is generally conditional on expected qualifications being obtained. If the exam results are what the applicant hopes, she gains a confirmed place in August, and starts her studies in September or October.

But not all of her cohort would have followed the same route. Some people, either by deliberate choice or due to unexpected exam results, enter a process called Clearing. Here the process is much quicker, with application, offer, acceptance and placement all happening over hours and days rather than weeks and months. This happens straight after A-level results day in mid-August – and is the reason mid-August is a bad time to call a university about anything else.

How do applicants decide where to apply? There’s a number of places to get more information about institutions – Hotcourses’ WhatUni site is one of these. We feel the data they hold might be a decent indicator of the level of demand for information about a university, and thus a good proxy for the level of interest in each provider. In reality, of course, each decision to apply, accept and offer or take up a place is made drawing on a uniquely personal mix of data, prejudice, aspiration, fear and avarice.

Into the data

By looking at data from each of these points across both cycles we can see the beginnings of a number of trends – and we can see how interest data (like we have used from Hotcourses) is giving us an early warning. The first five tabs offer a view of a particular point in the cycle, or derived value (showing the whole sector by default). The last tab (“Cyclical Change”) is really for looking at an individual institution, and trying to make sense of how things are changing overall.

Note that this shows institutions where we have data from UCAS and Hotcourses – so omits Northern Ireland, and we’ve left out the University of East London because of anomalies in their data that UCAS are currently working to fix.

And one important thing to remember is the very different environment in Scotland. With student number caps still in place, it does not make sense to directly compare institutions on both sides of the border. Scotland is turned off by default in the sector-wide visualisation – it needs to be looked at separately.

Applications

The headline is that the Russell Group of institutions are generally seeing growth between the two cycles, other institutional groups are tending to see less applications. The Hotcourses data (shown here as a colour gradient between dark blue for lots of interest over the cycle, orange for less) looks to be a good predictor here, with a lot of blue at the top of the graph.

For all the talk about supporting student choice as a consumer drawing on detailed data from a diverse sector, it seems that actual students are choosing the same kind of things as they would have chosen in previous years. Of course – and as we will see – these institutions are now able to meet that interest.

Selectivity

With simple arithmetic (applications minus offers) we get a sense of institutional and sector strategy. Simply put, more offers are being made. Higher up the graph we see institutions turning away thousands of applicants – at the bottom we see institutions making offers to nearly everyone that applies.

It’s important to understand that this says nothing about academic standards – institutions in many cases will be positioned in such a way as to primarily receive applications from those who are academically capable of following the course. Others, especially the more popular ones in Hotcourses terms, may see a huge number of “aspirational” applications from people unlikely to get the required grades.

Again, as you might expect, the Russell Group institutions are more selective by this measure. But the difference isn’t as marked as you might expect – for example London South Bank is far more selective – by this simple measure, at least – than Imperial College.

[edit: there’s been a couple of requests for a proportional measure of selectivity, I’ve added a simple “percentages of offers accepted” as a new tab.Still plenty of delights and surprises to find in that view.]

Non-mainstream placement

Much of this activity (calculated by subtracting June deadline placed applicants from all placed applicants) can be put down to one activity – Clearing. A word that has lost any stigma it once held, only Cambridge placed all students from June applications in 2017 – and in 2016 every single institution placed students from applications made after the June acceptance deadline.

Here I’ve used Hotcourses data from the month of August in each cycle – you can see that it’s still a pretty good predictor but is less perfect – and smaller institutions like UHI don’t suit this model at all. Million Plus institutions tend to place more students later in the year, as you would expect from institutions that work with greater numbers of students from a wider range of backgrounds. But, again, there are outliers – Sunderland takes less students outside of the main cycle than York.

Acceptances and unaccepted offers

A difficult data point to make sense of, acceptances measure the attractiveness of an institution to students, and institutional discernment in making offers. Half strategic decision and half marketing effectiveness, a high number of acceptances here ensures that a relationship between prospective students and their chosen institution has already begun.

Clearly – with a simple numeric measure – large institutions will accept more than smaller ones, making this graph a measure of size as well. But it is notable how well the Hotcourses data predicts acceptances… a lot of blue at the top of the graph and orange at the bottom.

Subtracting offers from acceptances is a lot more interesting – offers that have not been accepted speak of students who decide to go elsewhere once they have an understanding of what is on offer to them. What’s notable here is a number of larger Russell Group institutions being rebuffed at this stage. This would generally suggest high expectations of academic performance that are not met. On the other hand, Oxford and Cambridge manage to accept more students than they make offers to.

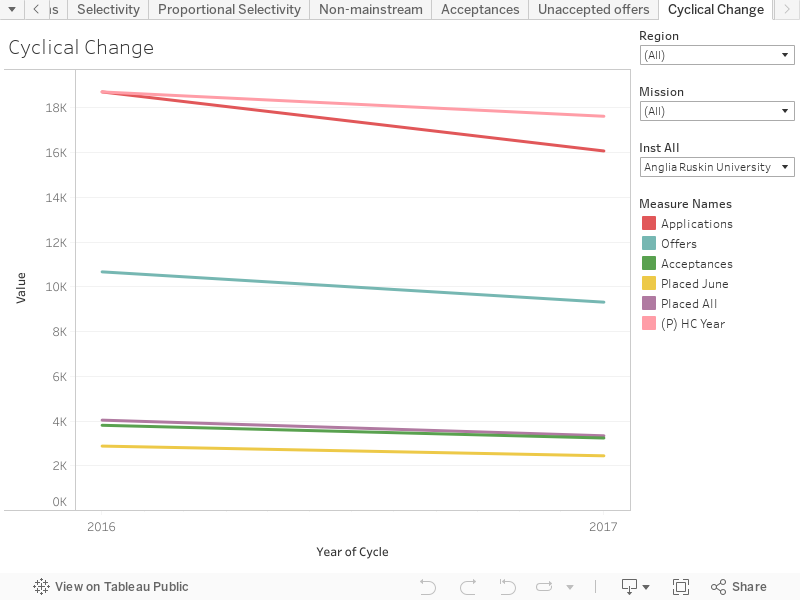

Cyclical change

I’ve plotted this to allow you to take a more detailed look at individual institutions, but if you select “(all)” institutions you can see regional, mission group, or sector summaries by using the other filters. The Hotcourses line shows the proportion of interest shown in that institution (or group) compared to the rest of the sector over those two cycles – it is plotted on another (hidden) axis, and the values you see are proportions.

LSB has 18,050 applications and makes 9,275 offers (‘WonkHE selectivity’ = 8775′)

Imperial has 8,945 applications and makes 3,530 offers (‘WonkHE selectivity’ = ‘5415’)

This means LSB give offers to around half of their applications. Imperial give offers to around 40% of their applications. Imperial get 2.5 applications per offer place vs. about 2 for LSB.

In absolute terms, LSB are certainly turning away more applications than Imperial – because they get more – but that isn’t the same as being ‘selective’. And I’m not sure your description of the data is accurate either – especially with an arithmetic y-axis. Imperial are lower than LSB, but aren’t making ‘offers to nearly everyone that applies’.

Fair point Martin. It’s an artefact of the way we’ve looked at the data. I think this approach was interesting as it let you see in real terms where large numbers of students were applying unsuccessfully. This is selectivity as experienced by the student, which is slightly different than selectivity as practised by the institution. A proportional rendering would be interesting for the reasons you suggest and will add one to the visualisation when I get a moment.

Can you add in an offers-per-application measure? Would make for an interesting additional comparison.

Oooooo – and all this but over the last 3 cycles perhaps? I have all the requests 🙂

@David @Martin – I’ve added a Proportional Selectivity tab for your data interactivity pleasure.

Looks good – thanks.

Would it also be possible to see ‘Proportional Acceptances/Rejections’ i.e. % of offer holders who accept/reject? It would be interesting to see which institutions appear to be improving/getting worse at establishing and maintaining a strong relationship between applicant and institution to boost their acceptance rate.

What does the hotcourses data show?

Is it pageviews or some other interaction with the site? And is the value for each provider an absolute one, or a proportion of something else like the total interest across all providers?