On 1 January 2018 the Office for Students took over the regulation of higher education in England from its predecessor (the Higher Education Funding Council for England (HEFCE)).

One little discussed impact of this change was an avalanche of university borrowing that has dramatically shifted the priorities and risk profile of English higher education.

Terms and conditions

As late as the 2017 memorandum of assurance and accountability between HEFCE and higher education providers, the regulator had the right of veto over university financial commitments over a certain level. If you wanted to borrow money, and you were talking “serious money” in relation to the size of your provider, the regulator needed to sign it off.

That year written approval was required where total financial commitments exceeded six times the average adjusted net operating cashflow (ANOC) from July – or where the provider was assessed as being “at higher risk”. The year before, it was required when borrowing crept above five times the (six year) average EBITDA. And back in 2006 it was required for borrowing over 4 per cent of income.

The levels may have shifted over the years but the principles remained the same – to ensure that providers in receipt of public funds offered value for money, and were fully responsible for the use of these funds. These broader requirements were set out in detail:

HEIs must apply the following principles when entering into any financial commitments:

a. The risks and affordability of any new on- and off-balance sheet financial commitments must be properly considered.

b. Financial commitments must be consistent with the HEI’s strategic plan, financial strategy and treasury management policy.

c. The source of any repayment of a financial commitment must be clearly identified and agreed by the governing body at the point of entering that commitment.

d. Planned financial commitments must represent value for money.

e. The risk of triggering immediate default through failure to meet a condition of a financial commitment should be monitored and actively managed

At some point during the transition from HEFCE to OfS, all this was scrapped.

The missing consultation

If “at some point” sounds uncharacteristically vague that’s because the decision was murky even by higher education policy standards. The requirement was in the 2017 memorandum – it wasn’t in the OfS 2018 “terms and conditions” of funding, or any of the registration or information requirements, or the regulatory framework. The shift was never consulted on, it wasn’t in the Green or White paper, it was never discussed in parliament. It just kind of happened.

In Wales, there are still requirements to get borrowing above a threshold signed off based on the 2017 Financial Management Code – however your (individual provider) threshold is built into the formulae of your financial forecast template. Thresholds are never published, but Medr may occasionally drop you a note to tell you what yours is. Which is nice.

In Scotland things are (slightly) more straightforward: there is a threshold over which SFC’s formal consent is required. It’s not a concrete figure but a calculation to determine whether the total annualised cost of the borrowing exceeds 4 per cent of total income (according to a university’s last audited statements) or would exceed by 4 percent the estimated total income for the year in which the borrowing begins – whichever one is the lower.

As things currently stand in England the explanatory sections on the D conditions of registration set up definitions of financial viability and sustainability. Viability is the interesting one here – for OfS purposes it means there is no reason to suppose the provider is at a “material risk of insolvency” (being unable to pay debts as they fall due) for the next three years. This clarifies that OfS does expect to know about borrowing (“have regard to” in fact) – and even suggests OfS would expect to be able to speak directly to lenders:

It will be for the provider to ensure that the OfS is fully informed as to its financial facilities, and it will be expected to consent to the OfS making direct enquiry of the finance provider if requested to do so. The OfS may draw inferences from a failure to provide such consent.

This approach to university borrowing can also be seen in the transition provisions that existed as OfS effectively carried on as HEFCE while it began to register existing providers – a commentary to the required audited data included the need for universities to include information on:

Whether the provider is planning to take any loans from a bank, shareholders, directors or anyone else and, if so, information about these plans (how much is it planning to borrow, when will this be taken out, when will it be paid back, what will it be used for) and whether it will affect the provider’s viability or sustainability.

A very good year

This shift did not go unnoticed by universities, so 2017-2018 became a bumper year for university borrowing – with banks, private funds, and the bond markets all displaying an appetite for access to (then) underleveraged, secure, and low risk UK higher education.

The 2017 HEFCE financial health publication noted that:

At the end of July 2017, the sector reported borrowing of £9.9 billion (equivalent to 33.1 per cent of income). This is £980 million higher than the level reported at the end of 2015-16, which was £8.9 billion (30.7 per cent of income).

By 2018 OfS as reporting that borrowing would reach £12bn by “year 2” (2017-18).

At the end of Year 2, the sector reported aggregate borrowing of £12.0 billion (equivalent to 36.8 per cent of income), a 21 per cent rise of £2.1 billion compared to Year 1. Forecasts show that borrowing is projected to continue to rise in absolute terms over the four forecast years, reaching £13.3 billion by the end of Year 6.

In the last quote, “year 6” is 2021-22 – the projection of aggregate borrowing was (as usual) on the low side. That year’s financial health report pegged it as just over £14bn.

OfS, of course, could have decided to apply specific conditions of registration if it was concerned about borrowing at a particular provider. It still gets information on what universities are borrowing, and on what they plan to borrow in future, via the annual financial return (and there have already been rumblings about an increase in the amount and frequency of provided data). It could have stepped in to moderate the boom in borrowing since it took regulatory control of the sector – it did not.

The morning after

But the time of plenty has clearly passed – affordable finance is simply harder to come by, and the terms of existing borrowing (set during a more confident era) have often been renegotiated. The 2024-25 aggregate external borrowing is projected to be £13.3bn, and this for a much larger sector. And even the sector’s own (generally optimistic) forecasts suggest that it will drop further in years to come.

This is very much the hangover after the party. The easy money simply isn’t there for the sector to borrow – all that remains is the improvements it paid for (hopefully in useful, tangible, things like estates and infrastructure), the repayments, and the interest.

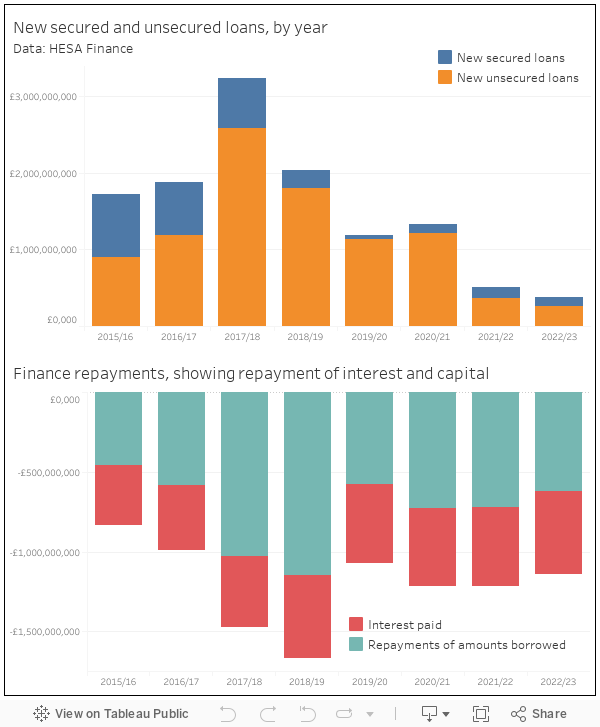

You can see that in the data (Based on what I know about what has happened so far I don’t think this includes stuff like bonds, so the figures are illustrative rather than precise) – the big peak in unsecured loans was in 2017-18, the academic year that restrictions came off (the smaller peak in 2020-21 represents the government backed Covid loans).

You can also see a peak in repayments in 2018-19: clearly many providers decided that with the brakes off, the easiest way to proceed was with short-term revolving credit. More worryingly for sector finances, interest repayments remain at 2018-19 levels even though borrowing has declined sharply – an impact of a rise in interest rates following a long period of near zero inflation.

A legacy of loans

In essence some of the blame for the current financial crisis faced by the sector can be attributed to this little-scrutinised decision to remove borrowing safeguards. Though estates (especially) benefited from this gold rush, the entry of UK universities into the world of private placements and bonds has left a legacy that will take decades (and hundreds of millions of pounds cut off the top of sector finances, and increasingly arduous restrictions on university activity within covenants) to reckon with.

And these controls on university activity hit in numerous ways. As Philip Augar’s review noted, way back in 2019:

Universities’ expansion has been partly funded through debt and financial arrangements known as ‘sale and leaseback’. The former includes bond issues and bank borrowing; the latter involves universities selling student accommodation for cash upfront, sometimes committing to provide specified numbers of rent-paying students to the new owner.

A failure to meet challenging recruitment targets has a multiplier effect if you factor lender requirements into the equation.

Was the removal of controls over borrowing the single most important regulatory act of the modern era? For those able to raise money in this way, it supported huge improvements in university estates and infrastructure. It provided the capacity that has underpinned recent growth – though not as much growth as we saw in the 90s and 00s, when a far greater proportion of capital came from the state.

It’s at least arguable that for many larger and better known providers the amount of indirect control over their actions that has been ceded to investors via covenants linked to borrowing. has driven the dash for growth at all costs. If you’ve worked in a university during this period and feel like things have changed, this could be why.

And it gets worse if you think about the aggregated risk across the whole sector – not least because the arms race of expansion forced the majority of the sector to seek private finance at roughly the same time. The numbers in the chart above are indicative – but even so show a sizable liability that could have a huge impact on the way providers behave. It’s the roots of the sector-wide dash for growth that the regulators have expressed concern about – but thus far the impression has been given that it is just empire building. It is survival.

The next few years

There is no easy fix. Though I think most of us believe that the government would step in in the event of provider failure – to protect the student interest certainly, and possibly to protect the local interest – what would happen to outstanding debts across multiple providers in these circumstances is less clear. It is entirely likely that a loan becoming due for full payment due to a breach in covenant conditions would itself be the cause of provider failure.

In the bad old days, when the government was a significant source of both capital and recurrent funding for most universities in England, there was a thing called exchequer interest – a complicated and little-discussed aspect of public funding that means that assets purchased with public funds should revert at least in part back to the public. Exchequer interest as a consideration for capital investment has largely been replaced by lender interest – in the event of a provider collapsing large parts of abandoned campuses (which, of course, have been paid for by public funds in the sense that it is income from fees that has funded repayments) would revert to lenders.

These buildings and this equipment would immediately lose a lot of value, which is one reason why lenders like to renegotiate rather than repossess. If you think about it, a large teaching block in the middle of a thriving campus is a clear asset – without the campus it is a liability that needs to be repurposed and maintained.

So if you ever see the government stepping in to save an anchor institution, recall that private finance has an interest in seeing campuses continuing to throng with students. It’s a funny way to preserve the future of the sector, but we live in peculiar times.

Meanwhile FE colleges have been taken into the public sector and can no longer borrow at all, even though they provide significant amounts of tertiary education.

Removal of college ability to borrow was another decision made without consultation or impact assessment

Two years later, it makes it a lot harder for colleges to expand their construction training provision to meet demand and need

Perhaps one of the reasons why OfS abandoned the tight limits on borrowing maintained by HEFCE was its desire to grow the number of alternative providers many (most?) of which have turned out to be for-profit providers. Their business models depend on a degree of leveraging that would be unacceptable in a ‘public’ institution. So, if the old HECCE controls had been maintained, the OfS would have been accused of curbing ‘innovation’. If this is – partly – what happened, it would be an example of the alternative / for-profit provider tail (with a small number of students overall) wagging the mainstream / public provider dog (which provide the bulk of students in the system). Quality is another example.

Not sure that the HEFCE constraints on borrowing were as ‘tight’ as suggested. I served on its Board in its dying days and recall debt proposals for Us XYZ being pretty well waived through – my comment at the time was that we were watching a slow train wreck being created! True, for the years I was on the OfS Board no approvals for borrowings were required. As for the bankers triggering a U’s insolvency, I doubt it – the debt can be endlessly ‘restructured’ and anyway no bank could be certain how much a U’s assets/buildings might be worth in a fire-sale…

OfS (and DfE) possibly didn’t think.enough about the 2018 rule changes but didn’t the big expansion of university borrowing take place earlier in the 2010s and aren’t the biggest deals mainly in the bigger, academically selective universities? Back when HEFCE did have rules to approve borrowing, it approved quite a few. Here’s a article from 2018

https://www.ifre.com/story/1516984/uk-universities-turn-to-private-market-as-debts-rack-up-dhp0nmdjz5

Many HEIs would also have thought that UK UG fees would rise, at least by some inflationary measure and maybe in relation to a TEF rating, such that repaying loans would have been easier.

Where public sector meets private sector, it is the private sector that tends to win and even more so with financial deals.

When interest rates on borrowing are1%, taking out big loans looks like a good move but when the rates hit 5% it does not. The details for repayment arrangements are also critical. People / organisations with interest only terms, with no capital repayments over several years are taking big risks. However, it is often the case that the people who made the original decisions have moved on, leaving the next incumbents to clear up the mess or go bust.

It is not only Universities that are in this position, so too is the entire Government.

This change was always meant to work in tandem with the cap removal to turbocharge ‘market behaviour’ in the sector. It certainly did so, both in terms of ‘growth at all costs’ as mentioned in the piece, and in terms of the balance sheet logic of the sector’s behaviour since. And now look at how these decisions in a globally anomalous borrowing context with artificially low interest rates and a bunch of (temporarily) free money sloshing around must be paid for, and the resulting debts serviced. It comes down to the fundamentally (and fundamentalist) misguided assertion that higher education can and ought to be a service market at the tender mercies of lender capital like everything else in the UK.

It would be interesting to see Wales Scotland and England separately as that would indicate whether the peak in borrowing was related to the regulatory change in England, or other factors, principally historically very low long term interest rates. Repayment rates are bound to remain stable, you generally don’t take long term finance and pay it back quickly. Borrowing will often have been to fund investment to enable growth, so I think the causation in the article is the wrong way round, any “dash for growth” is likely to be the implementation of plans to grow that included borrowing for infrastructure. All other things being equal, successful universities will always want to grow and do more of the things they believe in, so if you remove restraints such as student number controls, universities with the ability to recruit more students will do so, hopefully partly growing the market, but also at the expense of competitors.

It’s an interesting article, but I feel it’s missing some important context. First is that the sector would have been inundated with analysis pointing to a significant demographic upturn, necessitating investment in infrastructure to accommodate. 2018 would also have been about 6 years after no increase in tuition fees, meaning that capital investments were best financed through borrowing – which was at historically low rates.

The former HEFCE ‘limits’ where always a trigger for engagement rather than an absolute limit. Governing bodies are responsible for the financial management of their universities. If the regulator stipulates borrowing thresholds it weakens that responsibility by potentially being handed regulator approval for borrowing that the university can’t afford. A better approach might be to sharpen governor liability in the event of insolvency.

The increase in borrowing, and its liberation from English regulator oversight, has in effect funded the massification of HE, along with so called ‘off-balance sheet’ financing deals for student accommodation. People are quick to express shock horror at the increase in borrowing, but without it participation rates would be at 1980s levels (<20%).

Another interesting question, for another day, is how will providers cope when the balloon repayments of bonds and private placements become payable. The underlying assumption is that they will simply be re-financed, made all the easier by the real terms erosion of debt liabilities by inflation. But what if lenders are less receptive to the HE sector, or interest rates materially higher? You can have a sympathetic and commercial conversation with your bank relationship director if you have a bank loan. Bond holders on the other hand don't generally seek a relationship and bonds as instruments are much more unforgiving.

This is not only an issue of finance but also of governance. University councils (who have to sign off on large capital projects) are often effectively chosen by University Executive Boards. There is therefore no proper accountability when pro-vcs put forward their pet projects. There was no proper business plan when the SPARK building was approved in principle by Cardiff University’s Council in 2013/14. As an academic member of Council I forced a vote on this but was outvoted 30 to 1. Cardiff University thus acquired 100 million pounds of debt and a great white elephant of a building. This is at the root of Cardiff uni’s current financial crisis and moves to turn Cardiff uni into Cardiff UINO (University In Name Only)

It’s pretty tenuous to say that universities can borrow without restrictions and further then that this is the cause of financial stress of the sector. The article focuses only on regulatory restrictions, not on any business plans or due diligence that lenders would provide, or the availability and pricing of capital in the market, and as one poster above also mentions, the governance (or lack thereof) of institutions, committees, and also the individual fiduciary duties of those holding director roles. this article as an example, does seem to reflect a tendency to blame something external (eg de-restriction) rather than acceptance of responsibility for internal governance and decision making. The other side of this debate might be what would the state of the sector be if investment had been curtailed by heavy regulation…

It’s not like all of this couldn’t have been foreseen! Indeed, it was forseen. The Higher Education Commission report on Regulating Higher Education: Protecting Students, Encouraging Innovation, Enhancing Excellence in 2013 chaired by Lord Norton of Louth and Roger King was funded by PWC and made a series of recommendations to tackle these issues. One of the recommendations was the creation of an insurance scheme funded by institutions to encourage collective responsibility for any future institutional failure and to discourage moral hazard and to encourage prudential borrowing. The great and the good all contributed to this review through interviews. Regrettably in retrospect this aspect of the report was ignored and has now been largely forgotten. I remember discussing the report at the time with institutional leaders and let’s say they individually had no appetite for taking responsibility for the predicament of others. Ironically, it is some of those same institutions that now find themselves in that position.