Back in March the government commissioned an independent review into university spin-outs with experts set to “to identify best practice in turning university research into commercial success, in order to help the UK fulfil its ambition to become a Science and Technology Superpower.”

Commentators in the start up community have urged the government to “sweep away decades of bad practice.”

A lot to play for, then.

While the review was originally billed as reporting in the summer, Wonkhe now understands that its release is expected to coincide with November’s Autumn Statement. To help Wonkhe readers engage with the review we’ve taken a look at some of the big debates on university spin-outs.

Spin out

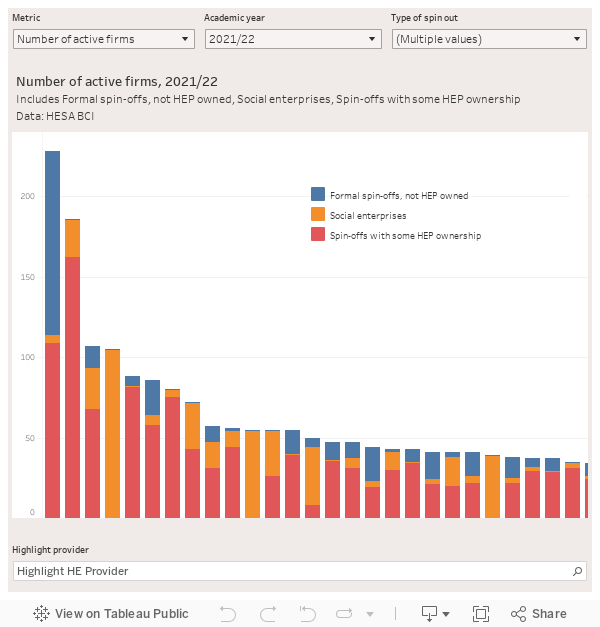

A university spin-out is a company that an individual, team or university themselves creates out of research they have carried out. There are currently an estimated 1,166 active spin-outs in the UK.

They come in all shapes and sizes across a range of disciplines but life sciences are the most popular programme family to be spun out. We’ve put together a chart of the number of active university spin outs using HESA data (owing to different methodologies and definitions numbers between data providers may differ)

The actual mechanics of moving from research, to founding a company, and through to getting an investor can be no more or less exciting than lots of other business transactions but equally it can be just as fraught.

Back in January the Financial Times reported the story of Bo Jing – the former University of Oxford student who was locked into a legal dispute with the university over unpaid royalties involving bio-tech start-up Oxford Nanoimaging.

In the words of England and Wales’ patent courts a key argument was whether “Oxford’s policies are unfairly weighted in favour of the university and senior academics, who may have contributed less to the detail of the work more than more junior researchers or inventors.”

The case became an exceptionally complex interrogation of patent law, contracts, and consumer rights, but in the end ruled that the university was entitled to royalties from Oxford Nanoimaging. The court carefully considered the extent to which a university can lay claim to intellectual property developed by their students, and in this case the judgement concluded that the university believed they were offering Jing a good deal when it came to a share of the intellectual property that was created.

The story illuminates one of the core debates concerning university spin-outs – what are the incentives for academics to try and build companies out of their research?

Spin wars

One motivation could of course be money. Most people don’t become academics for the pay but the commercialisation of research isn’t a bad way to make a living. The average deal over the past nine years has been just shy of £4m – however the proportion of this that flows to researchers can be less impressive by the time universities, partners, and anyone else with a legal claim to the intellectual property take their cut.

A report by Beahurst shows that in the last decade 1,130 university spin-outs have secured equity investment – external funding from whatever source in return for a degree of ownership – with a record of £2.73bn invested in 2021 declining to a not-insignificant £2.34bn in 2022. Oxa, a University of Oxford automotive spin-out company, secured £114m in December 2022.

However, as in the case of Bo Jing, there is an important debate on whether universities take too great a stake in their spin outs – an issue that dominates much of the spin-out business news. The mean university stake is now 17.8 per cent – down from 24.8 per cent a decade ago – but this is significantly higher than the average equity taken by US universities.

Academics should be fairly remunerated for their expertise and universities should be remunerated for providing facilities, expertise, infrastructure and the education that make spin outs possible.

Spin round

If the spin-out review becomes locked into an ever more detailed war of attrition on whether universities should be taking a 15, 10, or 5 per cent stake in spin-outs, it will be a lost opportunity to properly examine how the wider research ecosystem encourages academics to spin out companies.

Although in the end the viability of spin-outs comes down to money it takes an awful lot of work to build a spin-out in the first place. This isn’t just a matter of skill but a matter of incentives. Including whether universities have the promotion, reward, and remuneration processes in place that recognise the talents of academics that turn their expertise toward the commercialisation of their research.

There are of course external measurements of spin-out activity through KEF. However, this is not a reward mechanism either, and it is avowedly (and rightly) also not a league table. I’ve argued before that it is time to fund KEF and another benefit of doing so could be to disincentivise universities from taking such large equity stakes in spin-outs. If there was some sort of additional flat funding allocation based on spin out density universities would always be guaranteed some form of return on their investment, and the question of equity could become marginally less important.

The argument against remuneration is that effectively universities would be paid three times. They would be paid for the spin out equity, paid for KEF performance and by proxy paid through REF where spin outs are used to evidence impact. The question about money is therefore about how to measure performance. Measuring performance and giving all parties access to how to measure performance raises important questions on whether academics have the right advice from funding councils, academies, and universities in the first place. There is a related but supplementary question on whether there are then the processes in place to allow academics to move between industry and academia.

Finally, even with the right people supported to do the right jobs good spin-outs rely on a wider ecosystem of investors that are suitable for universities. This ecosystem relies on business but it can be more easily brought into existence through government fiscal policy.

In the end, a lot of the debate on spin-outs will come down to money. However, who the money ends up with at the end of a research, company building, and investment getting process, is the end result of sometimes decades of getting the right people together at the right time with the right incentives to build sometimes world changing things.

It’s in understanding the process, not just who gets what, where better fairer spin-outs can be built.

Being part of a very successful department when it comes to spinouts I’ve seen many Academic’s make significant personal sacrifices in the process that ultimately gets them a personal fortune, and more importantly for the University further ‘commercial’ research work. Not killing the ‘Golden Goose’ is key if the University wants to have a long-term income from a spinout.

When it comes to IP however I’ve seen Academic’s and more over Technical ACREL Managers ‘steal’ Technical staff’s ‘prior art’ so they can exclusively patent a newly developed process and equipment without including the Technical staff who actually designed the equipment several times. Until Universities prevent such theft many Technicians who’ve been affected won’t share their idea’s freely, thus limiting the potential for spinning out a company that would use those idea’s and techniques.