With most of the Clearing action over, this feels like as good a time as any to review how well English providers are performing against the tough recruitment targets they set themselves back in 2017.

We’re two years into a quasi-Stakhanovite four year plan – and there were some very ambitious numbers. As the Office for Students remarked at the time “the sector has made over-optimistic student recruitment forecasts – both nationally and internationally”.

Now that one of the two projected cycles is finished, and another is close to complete (with only a few students still in Clearing to recruit) we can take a half-way point measurement.

Oh dear…

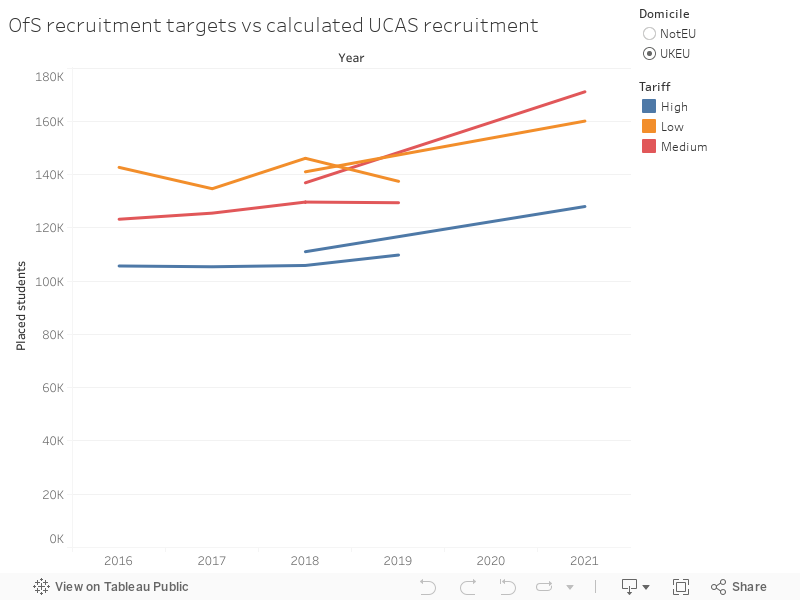

So just how far off the mark are each group? Quite substantially, it turns out. On many targets we’ve seen group recruitment go backwards. It is possible, perhaps, that the last two years will give them time to pull them out of the bag. But I’m not placing bets.

Predictions for 2018 have proved over-optimistic, to say the least. From what we can extrapolate from 2019 recruitment action, we are bravely entering the realms of utter implausibility. Had these been slight leaps I would have been there to listen to those of you about to leave me a comment to say “not everyone applies via UCAS” or “Brexit means EU students will count as non-EU”, or “in 2021 the number of 18 year olds returns to 2018 levels” or “do the OfS figures include postgrads” (I honestly don’t know on that last one) . But these are not slight leaps.

These projections come from regulatory financial reporting, so a lot of other projections – such as whether a provider has enough money to continue to exist or whether it can do all the things it has planned to do – are based on these numbers. A recruitment failure (and, honestly, what else can we call it?) generates a bleak prognosis for the sector.

Methodology

84 per cent of UK and EU students placed via UCAS (on day eight of clearing – which in the past has represented 97 per cent of placed students) have been placed at a provider in England. For non EU students, the figure is 88 per cent.

Again on day eight of clearing 36 per cent of UK and EU students have been placed in a “low tariff” provider, 34 per cent at a “medium tariff” provider, and 29 per cent at a “high tariff provider”. Interestingly the skew for EU students only goes in the other direction (26, 32 and 41 per cent respectively). For non-EU students the difference is even more stark: 10 per cent are at low tariff providers, 25 per cent at medium tariff providers, and 64 per cent at high tariff providers.

What I really want to show you is applications by tariff and institutional tariff. I can’t because UCAS doesn’t offer that data, so I’m going to use scaling on the figures I have got – and to do that I need a list of providers by tariff group.

Tariff grouping is not a formal or fixed idea, take any list of entry tariffs for higher education providers, and split them into three. But even though the composition of each tariff group will change over time (and method) I’m going to assume the share of the three remains static.

UCAS does let us see placed students by tariff and domicile, so we are going to take a flier and assume that the proportions set out above for day eight hold true for day 28. For previous years I’ve gone for a similar scaled approach to get England-only tariff splits. I know this isn’t perfect (the proportions of each tariff provider are not the same in each country) but as I have no idea how UCAS or OfS have done their split it is the best I can do.

Targets time

OfS gave us figures for percentage increase in recruitment over four years. I’ve used the increase over 2017 figures and divided by four, with the assumption that growth will be equal each year. This might feel like it ignores the projected demographic jump for 18 year olds in 2021 – but if you look closely at that you see that this is only a return to last year’s figures.

| UK and EU | UK and EU % | Non EU | Non EU % | |

|---|---|---|---|---|

| High Tariff | 22,619 | 5.2% | 27,154 | 19.5% |

| Medium Tariff | 45,546 | 7.7% | 15,262 | 19.1% |

| Low Tariff | 25,339 | 9.7% | 10,078 | 35.7% |

| Specialist | 21,379 | 15% | 3,420 | 15.7% |

Again, OfS did call this out at the time (as did everybody else). But two years in these targets have stopped being ambitious and have started to look silly.

The twist

It gets worse. As the more observant of you would note from the table above – OfS separated out “specialist” providers of all types – they have their own (equally ambitious) targets.

Because I don’t know how OfS has done this, I’ve just ignored the category in the plot. But look at the figures that are there, and imagine that we need to find another 5345 UK and EU students, and 855 non EU students each year. Ouch.