The Higher Education (Registration Fees) (England) Regulations 2019 (and the accompanying impact assessment) represent just the latest stage of a story that has captivated us here at Wonkhe since the inception of England’s new higher education regulator.

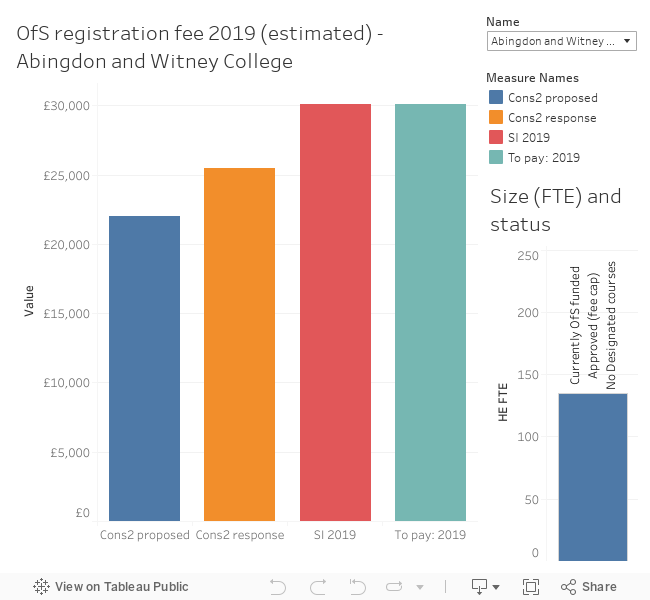

As expected, fees have risen sharply. Institutions are charged based on their student full-time equivalent (FTE) as before, there are discounts available for new providers, and “micro-entities” are exempt from fees. So, fully cognisant of the Board of the Office for Students’ (OfS) note of a risk of a “negative” reaction, here is approximately what your institution might be paying in 2019-20.

Just to talk you through that, the two pale blue bars represent the banding in the consultation (note that I have condensed these for ease of comparison) and the revised banding in the consultation response. The red bar is the raw figure that an institution would be liable for under the banding in the statutory instrument; the orange bar is my calculation of what each institution will pay after applying the “new providers” discount of 75 per cent in year one. The dark blue bar to the right shows the size of the institution in FTE according to the latest HESA data, and above I’ve shown whether the institution is currently in receipt of OfS funding and the type of registration it will hold for next year. Here if a provider is not currently funded by OfS but has registered for next year I have applied the year one discount.

[Update: An earlier version did not take into account s5(2)(b) of the SI, which states that institutions currently delivering courses designated for student support will not be eligible for the “new provider discount. For the institutions where data is available (177) only two institutions currently known to have registered with OfS will be eligible for the discount: The Minster Centre, and Christie’s Education Ltd.]

Data has been included for every institution where FTE data is available from HESA – some 177 institutions. Most of the remainder have previously been funded by OfS or had courses designated for student support – most are further education colleges or small, specialist, alternative providers. [Update 18/04: This now uses the OfS FTE student data, released on 18 April]

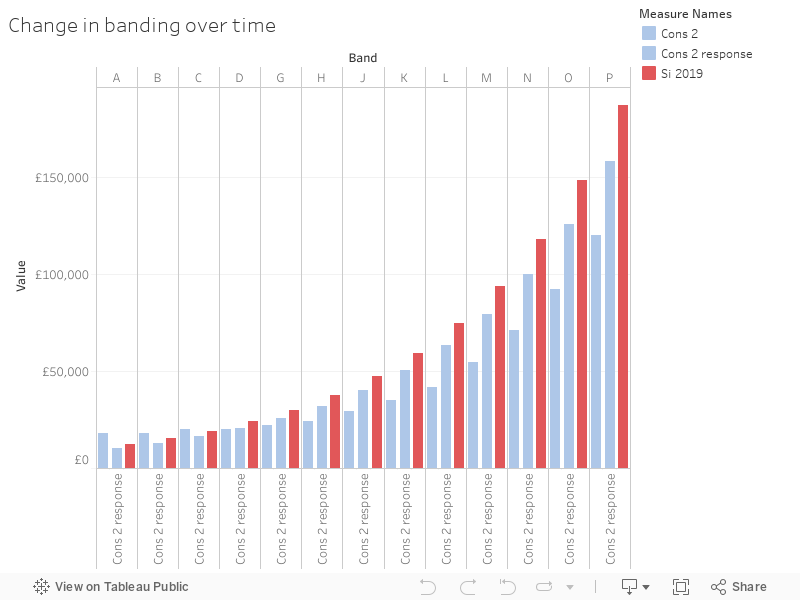

Here’s how the fees attached to each band have changed since the consultation.

The cost of the OfS?

The accompanying impact assessment has for some reason been carried out using the previous estimated fee banding. What is of interest to us here is the calculation of OfS’ running costs for 2019-20. Previously this was estimated at £26.2 million; it now stands at £27.2 million. The Department for Education (DfE) has been working to get that figure down, taking on the costs of the student information programme (£500k) and the cost of Prevent (not given) from government funds. Also, importantly, DfE will cover the costs of both the micro-entity exemption and the new provider discount at a stated value of £0.8 million.

DfE continues in its brave tradition of making ridiculous estimations of the total number of registered institutions – plumping for the risible figure of 464 for 2019-20 from which they expect the OfS to raise £26.3 million. There are currently 332 providers registered with OfS – the 177 I have FTE data for will raise £18.5 million between them.

Table 4 of the impact assessment suggests £26.3 million in expected subscription fee income from OfS in for the next academic year, based on payments by those 464 institutions.

We only have reliable HESA FTE data for 177 of the 332 institutions that have thus far registered. From those institutions the OfS is going to raise £18.5 million from subscription fees – so the question is whether the remaining 140 or so plus any others we don’t know yet about will be able to raise £7.4 million in (net – remember that costs discounts and exemptions are covered by DfE, and total £0.8 million) subscription fees.

The question remains why we do not have FTE student numbers for more than 140 providers, most currently funded by OfS – if we did we could at least make a stab of answering this question as to whether sufficient funding will be raised. OfS does have FTEs for 2017-18 used for calculating institutional funding tucked away in their grant tables, which would offer a usable proxy. However, unlike HEFCE, OfS does not provide the data on a single sheet for the whole sector.

There may be other ways to this data, and I will update this post as I discover them.

Table 8 is interesting, giving a breakdown of the fte of the ‘468’ – that interesting number of providers that DfE are using – apparently on the basis of OfS projections.

It’s right to note that at the last OfS Board it was reported that the initial resgistration process would be largely complete by the end of February, with a 100 more being processed. OfS must be expecting a last rush from providers whose focus is on tier 4.

Table 8 shows the number of micro providers – including 48 with fewer than 25 students.

I think the graphic (shown in old money!) would be better with notes rather than coins 😉

There have been 57 college-to-college mergers since the first HE white paper that proposed OfS (back in 2016) plus 23 sixth form college academy conversions. This has reduced the number of colleges who’ll be on the register by 1 August 2019 though it will have an uncertain impact on fees because a college with larger HE provision will simply end up in a higher fee band.

Over £1m for each one of OfS’ 26 KPIs. Consistent with bureaucracy and a top heavy organisation.

so – for small providers, the cost for each student is around £200. For universities, around £4-5 each. For small providers, about 3% of their total income. For universities, 0.2%. Cost looks a little different from that perspective.