In 2021-22, around 51,000 full time undergraduate students in England took out maintenance loans but not fee loans.

In cash terms this is £281.2m worth of maintenance loans, an average of £5,510 for each of these students.

As a proportion of all loan borrowers, those taking out maintenance loans stand at around 4.2 per cent of all students (up from 3.5 per cent in the previous year). This is a sharp rise following a decade during which this proportion fell and represents a potentially significant increase of 21.4 per cent over the previous year.

Who doesn’t take out loans?

Some six per cent of full time undergraduates domiciled in England did not take out fee loans in 2020-21.

The accepted wisdom is that there is a single clearly defined reason that this may happen: a person has access to other financial means (personal or family wealth, or an alternative Sharia-compliant source) to pay fees directly.

These are the people that you would also expect to be among the 9.6 per cent that do not take out maintenance loans – and for similar reasons. Either they could cover their living expenses up front in the same way as they covered their fee loans, or access to this form of loan was inaccessible for religious reasons.

There’s not a commonly understood model of why a student would take a maintenance loan only. And there’s certainly no theories around as to why these numbers are rising.

Where are these maintenance only students?

The closest we can get to spotting where these students are studying is by identifying providers where

- There are more students that have maintenance loans than fee loans

- The total value of maintenance loans is greater than the value of fee loans

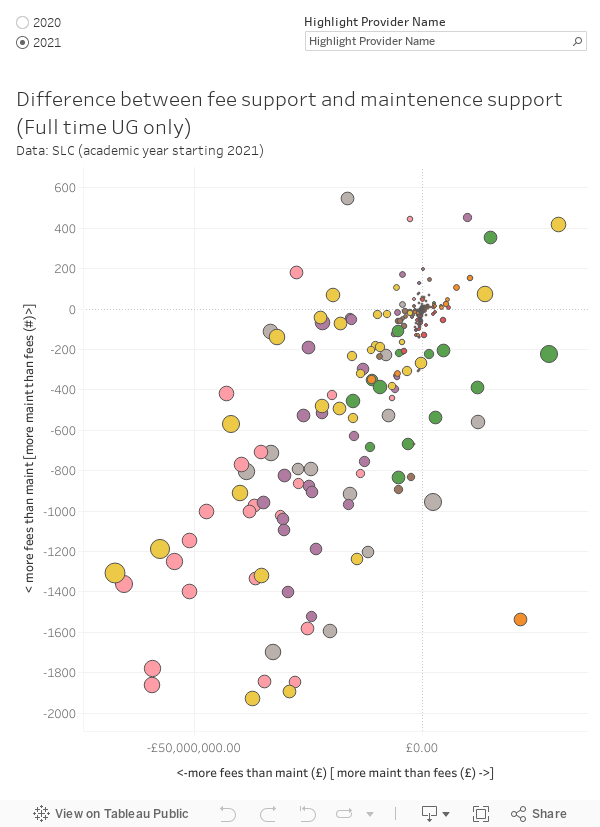

Here I’ve done this for the largest (full time, undergraduate) population for the most recent available year of SLC data. The providers we are interested in are those on the top right (and to an extent, on the top left).

This chart shows us the difference in numerical (vertical axis) and financial terms (horizontal axis) between fee loan and maintenance loan payments for each provider accessing the English system of student support. The size of the blobs shows the total number of students accessing loans at each provider.

So this chart is not precisely showing us where students with maintenance loans but not fee loans are. But it is showing us where they might be.

The right hand side of the horizontal axis (based on a comparison between the value of fee and maintenance loans) could show a situation where tuition fees are low but most students are eligible for (and take out) the full maintenance loan.

On the vertical axis (comparing the number of students with fee loans and the number with maintenance loans) you can see providers that are traditionally more likely to recruit students from well off backgrounds towards the bottom (showing a higher fee loan take up compared to maintenance loans). The providers above the zero line are those where the number of students taking out maintenance loans is greater than the number of students taking out fee loans (for full-time, undergraduate, courses).

What this emphatically is not is a smoking gun – there’s no evidence that any provider, or any institution teaching students registered at any provider, is systematically supporting people in obtaining undergraduate maintenance loans in breach of eligibility requirements – it is certainly interesting enough to think about what else might be happening.

Why would you take out a maintenance loan and not a fee loan? Indeed, how would you do that?

Free money?

If you are staring at your student loan balance in disbelief, you may be surprised to remember that in terms of borrowing the student maintenance loan is one of the most attractive borrowing options out there. Payments are linked to your income (so you’ll have no contingencies to plan for if you have a spell out of work), the interest rates have always been competitive (and are becoming more so), and the value of the loan is written off at some point in the far future.

If you compare that to an overdraft or a personal loan you can see why the idea of borrowing money off the government on these terms is an attractive one. Unlike the fee loans (which are used only to pay tuition fees), maintenance loans can be used for just about anything you fancy. If you are offered one, you are probably going to want to take it.

Maintenance loans are, of course, designed to support you during undergraduate study – and they don’t do a particularly good job of that. Most students, even those eligible for the full loan, need an additional source of income to cover rent, food, and other essentials. The promises that some unscrupulous higher education agents make about “free money” tend not to mention this.

As Jim Dickinson has related you might see a figure of around £15k on offer – an unusually optimistic scenario based on the maximum maintenance loan (usually £9,706 in 2022-23 for those living away from home, rising to £12,667 for those studying in London) plus grants like targeted parent learning allowance (up to £1,915), adult dependent grant (up to £3,354) and special support grants (possibly including childcare grants and the disabled student allowance).

None of this, to be clear, is free money. It is money that needs to be repaid, and is made available to (barely, on a good day) support the costs you incur while studying. But what if you could take out a maintenance loan and not have to worry about the fee loan, or indeed attending university at all?

The official version

Eligibility for student finance in England is dependent on a number of factors. Some are fairly straightforward – you need to be studying an eligible course at an eligible provider. Some seem straightforward until you think about them: you generally need to be a UK or Irish citizen or have settled status (but there are numerous exceptions – such as by refugee status or the amount of time you have been resident as a non-citizen). And there is one that can cause surprises – you can only get eligibility for student support for the length of your course plus one year, minus any previous years of undergraduate study.

Student Finance England offers a few instances where you might be eligible for a fee loan only – for example if you are ordinarily resident in a British overseas territory. It does not offer any examples of where you would be only eligible for a maintenance loan. It is possible that someone would choose to pay fees up front (thus avoiding a fee loan) but also choose to take up a maintenance loan, but it is very difficult to imagine a set of circumstances in which this decision would make financial sense. The whole point of paying fee loans in advance is to avoid the lengthy repayment period – why would you then voluntarily incur similar repayments for a maintenance loan?

And, to be frank, if you are paying anything in advance you probably have family or personal means. If you are well off enough to make a £9,250 down payment every September you can probably afford rent.

So, the set of circumstances in which students might take out maintenance loans but not fee loans are very limited and make little financial sense. And yet the data suggests more and more students are doing so. So what else might be going on?

Mind on your money

It all goes back to stuff we covered back in the pandemic about the precise moment someone becomes a student for the narrow and specific purpose of becoming liable for various loans from the Student Finance England.

When a student completes the process of course enrolment, and are confirmed by their provider as being registered on their course, they receive the first part of their maintenance loan. The fee loans starts later, after the statutory cooling off period. And it is only at this point a student becomes liable for fee loan repayments.

Like with any other contract, higher education providers must operate a cooling-off period – a chance to consider whether the contract is right for the student, lasting any time between two weeks and one month, depending on the provider – before the student becomes liable for a tuition fee. But it is possible that any student leaving their course during this cooling-off period, could have received maintenance support but wouldn’t be liable for tuition fees or fee loans.

For a lot of reasons it makes sense that a person can access a maintenance loan at the point that their provider confirms them as registered (usually the “start date”). That’s when your accommodation fees are due, that’s when you might need to buy books, or season tickets for transport, or one of those freshers week tickets that you get a flyer for.

And it also makes sense (as well as being a legal requirement) that providers operate a cooling-off period between this date and the point at which a student becomes liable for that term’s fee loan. It’s fair that you get a chance to try what you have paid for before you decide it wasn’t what you paid for.

Another date to keep in mind is the SLC attendance confirmation date – usually the Thursday before each payment date, so for a traditional start of term this would be the Thursday before the third Wednesday in October. As we learned during the pandemic, this can often be (but is not always) the day in which you first become liable for your fee loan.

All of this means it is possible (although in practice difficult) that a student could:

- Be confirmed as a student and receive that term’s maintenance loan.

- Start the course

- Leave the course before they become liable for that term’s fee loan.

Money on your mind

There is a contingency mechanism for reclaiming loan overpayments from students who notify SLC that they are leaving their course – either permanently or temporarily. SLC reassesses the amount of loan you are eligible for, and asks you to repay any surplus (it will even set up a repayment plan for you). If you return to your studies later on, the overpayment will be returned to your student finance payments – so there is a gap in that you don’t need to repay straight away.

The situation with student fee loans is different – no matter how many days after the cooling off period you remain you pay 25 per cent if you leave in term one, 50 per cent in term two, and 100 per cent in term three.

But this system has a hole – a reliance on the SLC being notified when a student withdraws. As we already know, withdrawing from a course isn’t a single yes-no decision and is more of a journey – a student may participate less, move away, miss assignments, not respond to messages, and only then admit that they are not participating. Calculating how many days of learning – or what proportion of the course has been completed – isn’t easy, and it is usually the provider that ends up notifying SLC of the withdrawal.

There are monetary incentives for both the student and provider to take time in letting the SLC know that the student is no longer on the course. If this can be expanded beyond the first term – “ah, well, they didn’t come back after Christmas” – then the provider gets to keep the first term of fees and the student keeps the first maintenance payment entirely. The 2014 “cashpoint colleges” scandal worked a little bit like this – low quality provision and low attendance, with money available for both providers and “students”.

But students taking maintenance loans only doesn’t help the provider at all (unless there’s some kind of deeply unethical kickback arrangement going on). It’s much more likely that students or agents advising students are taking advantage of these small loopholes and the vagaries of institutional administration and franchise agreements, remaining in the liminal state long enough to access and spend the maintenance loan but not to become liable for the fee loan.

It’s something that providers (and, frankly, the regulator) should be keeping an eye on. And the rise in the numbers of students in this impossible situation should be a warning sign for SLC and the Office for Students that something untoward may be going on.

Is there a correlation in the providers in the top right hand corner being those with recently expanded franchise work?

A fascinating question. It is possible that reporting down the line from teaching to registering provider and then on to SLC is more difficult, especially early in the life of an agreement.

I don’t see any huge puzzle regarding why students would take out maintenance loans without fee loans. I can easily see a scenario where reasonably well-off parents would be happy to pay for their child’s tuition, given that it’s a fixed cost and not at all affected by the child’s choices around accommodation, lifestyle, etc. Meanwhile, as the child remains responsible for the above, they’re told to pay for it out of their own pocket, which would normally involve taking out a loan.

An interesting model – would you agree that this is more likely to happen at providers above the line on the chart than below it?

But don’t children of reasonably well-off parents only get a small maintenance loan anyway?

Another great article and very topical. It’s fascinating to follow the Guardian College Cash scandal article (referenced above) and find that many of these institutions featured are still operating today. Even more surprising is that the individuals who are directors of these colleges often appear to be directors at other (private) colleges according to Companies House. There appears to be very complex matrix management structures.

First thoughts about the graph is that the correlation assumes that all providers are charging the max fee levels – this may not be the case for small franchise provision or franchise agreements with FE colleges. Equally, providers may just choose to charge less than the cap. Fee waivers and scholarships could also play a part.

There is an interesting correlation that Global Banking (in the upper right) have courses accredited by both Suffolk and Leeds Trinity (also both upper right). Fees are £9,250 but Global Banking are in the registered category meaning they can only access the lower fee threshold (£6k) via SLC unless they are on a franchise agreement, although this would mean that the students would then belong (and be reported) by the franchiser. Assuming they are working on the validated model with the lower threshold via SLC whilst charging higher fees with a privately funded component, it would explain the discrepancy between maintenance and fee income. The link with Suffolk and Leeds Trinity could just be coincidental.

So the probable difference in fee levels is why the chart also shows the difference number of students claiming each type of loan registered at the provider. If a provider had lower fees and catered primarily to students who qualified for larger maintenance loans you would see them in the bottom right quadrant – as students in receipt of higher maintenance loans would be less likely to have access to the funds needed to pay fees directly.

Thanks David. I was thinking more of a registered (not fee cap) provider. If a student was accessing the lowest maintenance payment of circa £9k per year, they would only be able to access £6k for tuition fee support due to the registered status of the provider. If tuition fees were above £6k (as if often the case) the student would have to self-fund the difference but this self-funded component would be invisible in your dataset.

The £3k discrepancy between the tuition fee loan and the maintenance payment could explain the variation in maintenance monies collected by students compared to tuition fee monies received by providers.