The last two weeks have been a tuition fees wonk’s dream and nightmare. The political class is more eager than it has been since 2010 to debate university funding. Every commentator and their dog has had a take on fees: good or bad, progressive or regressive, sustainable or short-term.

Much of the debate so far has focused zealously on the merits of the current tuition fee funding system: £9,000 tuition fees, the (second) abolition of maintenance grants, and the freezing of the repayment threshold. Yet the first cohort of these students only graduated in 2015. They are still very early in their careers, and the ‘repayment effect’ on their pay packets will take some time to be felt on both their incomes and the Exchequer.

But what of the slightly older cohort of millennials; those who began university study between 2006 and 2011? This ‘middle’ cohort of £3,000 fee payers – between £1,000 and £9,000, is often forgotten in debates about the impact of tuition fees.

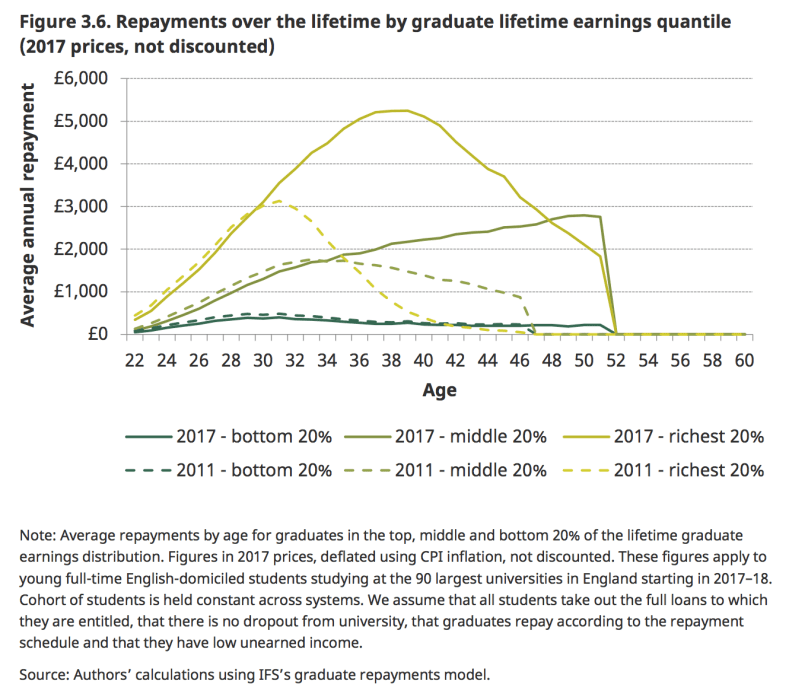

But as last week’s IFS report shows, it is this generation – and disclaimer alert, I am an aggrieved member – who are beginning to feel the collective bite of student loan repayments. Just take a look at the dotted lines on the below graph.

The first notable feature of this graph is just how similar the ‘2011 system’ (£3000) and ‘2017 system’ (£9,000) graduates’ repayment patterns are up until graduates’ early thirties. In fact, the 2017 system repayment patterns are slightly more generous in your twenties than the 2011 system. It would have been even more so, had it not been for the repayment threshold freeze of the past few years. £9,000 fee paying graduates only really begin to feel the bite compared to their elders when they get into their thirties, while £3,000 fee payers will begin to feel their repayments ease around then.

Most significantly, this ‘peak repayment’ point for 2006-11 system middle-class graduates is, for those who entered university aged 18, right now. £3,000 graduates will today mostly be aged between 24 and 29.

The middle earning quintile of graduates from this generation will now be paying roughly £1,500 per year on average in student loan debt; the highest earning quintile nearly £3,000. Post-election polling has suggested that it is this generation of graduates, as much as current students, that turned out for Labour in June: 58% of 25-34-year-olds backed Corbyn’s party.

There is some irony here, given that it was a Labour government who introduced £3,000 fees. But the majority of the generation in question are far too young to remember the 2004 fees controversy. In any case, Corbyn’s leadership has virtually turned Labour into a completely new party. Corbyn, of course, was one of the many Labour rebels for that infamous 2004 vote.

We know that students themselves are only partially driven by tuition fees as a voting motivator, but there is much less research into the behaviours of graduates who are paying their fees off. Given that loan repayments are a deduction from the pay slip just like any other tax, there’s good reason to suppose that such deductions irk graduate voters like any other tax burden. Many graduate millennials who earn less than their graduate baby-boomer parents might find themselves paying more tax as a result of loan repayments. No wonder they’re (we’re) annoyed.

Thus Corbyn’s (uncosted) hints before the election that he would seek to annul existing graduate debt as well as abolish future fees might have been significant. It’s revealing that Angela Rayner doubled down on this point yesterday. Still, most of the evidence points to fees being a ‘piggy back issue’ linked to wider discontents with the NHS, housing, and Brexit. Perhaps, if home ownership rates for people in their twenties and thirties were not at record low levels, there would be less political angst surrounding student loans? Is higher education funding policy now indirectly tied to the disaster that is British housing policy? Income contingency may not mean that debts are ‘crippling’, but that doesn’t mean they don’t slow (or prevent) saving for that first mortgage.

For the £9,000 fee paying generation, their time for real grievance will come. The height of their repayments will arrive much later in their careers – in their mid-late 30s – but also be much larger than for the £3,000 generation. Given the political shockwave that the current generation fee-paying graduates have created, there’s real danger for any government taking the £9,000 generation for granted going into a general election in 2027 or 2032.

If any cohort needs repayments ‘easing’ it’s pre-2012 students who pay 9% not above £21,000 (yet) but above £17,775. All the focus seems to be on the repayments of recent graduates but for someone who took a first degree on the pre-2012 loans and a PGCE this year on the post-2012 loans, I’m in the same overall massive debt burden but higher repayments to go with it – how can that be justified?

I also have a friend whose in a similar position who took a 7 year first degree on the £3k+ fees after withdrawing on the £1k+ fees. Not much difference in debt levels to current students but they have higher repayments like me, and also don’t have their loan written off until age 65! Crazy.

It’s the pre-2012 threshold that needs raising, not the post-2012…

See fig 3.6. Shocking. wonkhedev.jynk.net/blogs/forget-9… via @wonkhe

Forget £9k, it’s the £3k generation that matters (for now) wonkhedev.jynk.net/blogs/forget-9… via @wonkhe

Forget £9k, it’s the £3k generation that matters (for now) wonkhedev.jynk.net/blogs/forget-9… via @wonkhe

Forget £9k, it’s the £3k generation that matters (for now) wonkhedev.jynk.net/blogs/forget-9… via @wonkhe

Certainly looking forward to that loan write-off threshold 😉

tag:twitter.com,2013:887235690047688704_favorited_by_2273299381

well loved stories

https://twitter.com/Wonkhe/status/887235690047688704#favorited-by-2273299381

Those graduates who paid £3,000 fees from 2006-2012 are seeing their loan repayments peak right now ow.ly/kkrr30dwRWf https://t.co/mpr

Those graduates who paid £3,000 fees from 2006-2012 are seeing their loan repayments peak right now ow.ly/kkrr30dwRWf https://t.co/mpr

Those graduates who paid £3,000 fees from 2006-2012 are seeing their loan repayments peak right now ow.ly/kkrr30dwRWf https://t.co/mpr

tag:twitter.com,2013:887235690047688704_favorited_by_290481306

..

https://twitter.com/Wonkhe/status/887235690047688704#favorited-by-290481306

If home ownership rates for people in their 20s and 30s were not at record low levels, there would be less political angst surrounding loans

Those graduates who paid £3,000 fees from 2006-2012 are seeing their loan repayments peak right now ow.ly/kkrr30dwRWf https://t.co/mpr

The difference in the timing of payments is due to the lower repayment threshold (still used in Scot and NI) for the 2006-11 cohort.

I was at university from 2000-2004 under the £3k fee regime, but unfortunately lost most of my twenties to ill-health so have only started making repayments in the last 3 years under the Plan 1 schedule of 9% of gross earnings over £15,000. Yeah, £15k. Ouch. Not only is it hard to get a decent-sized mortgage with that level of deduction, but I’m pretty sure a lot of graduates in a similar position will also be putting off having children due to affordability concerns, so the demographic repercussions of this tax could be fast and immense.

I think the introduction of degree apprenticeships is a really positive move for the country and the sector, and my guess is 5 years from now this will be how the majority of students take degrees. Of course, the problem for the government will then be how to accommodate all those extra people in the workplace…