The 2021 Census showed that for the first time the average person in the UK was aged 40 or older.

We are a nation rapidly approaching middle age – and increasingly likely to need the flexibility to upskill or retrain at various points along the career path as a result.

This was one of the problems the lifelong learning entitlement was supposed to solve. It promised a radical rethink in terms of how we provide opportunities and incentives for people to learn across their lives.

It was supposed to provide not just an alternative pathway to a level six qualification, via more stand alone level 4 and 5 options, but an opportunity for reskilling or upskilling at a later point in people’s careers.

Supply and demand

Fundamental to the success of the LLE rollout is understanding the demand for these courses, not just the supply of them. We won’t solve the challenges of an aging population and rapidly changing skills and workforce needs unless we build a funding and qualification system that actually gets people through the metaphorical door – including accessing the new loans as they become available.

Polling from Public First however shows that there is a risk that those who would likely most benefit from new types of skills provision are unsure about whether or not they want to undertake it:

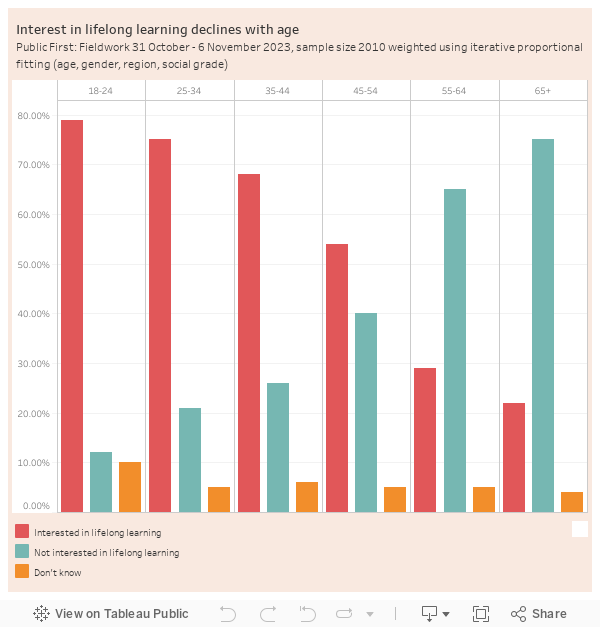

- Just over half (53 per cent) of people say that they are interested in lifelong learning in some form – but this interest lessens with age. Some 68 percent of 35 to 44 year-olds say they are interested in lifelong learning, dropping 29 per cent by the time they’re 55-64.

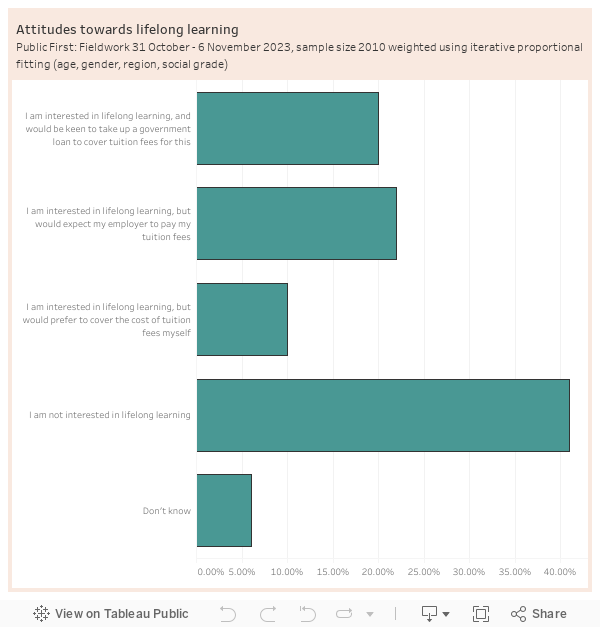

- Younger age groups are much more amenable to taking out a government loan to fund tuition fees, as the LLE proposes: 35 per cent of 18-24 year olds would be keen to take out a loan, compared to only a quarter (25 per cent) of 35-44 year olds, and only 12 per cent of those 55-64.

- Many would prefer that their employer paid tuition fees for lifelong learning courses rather than taking out a loan or self funding – something which has come up little in the design of the LLE so far.

- Only 37 per cent of those whose highest qualification level is at GCSE or equivalent say they are interested in lifelong learning, compared to 52 per cent with A level equivalent and 63 per cent of graduates – and those who have not already experienced higher education are much more reluctant to take out a loan to fund it than those who have a degree level qualification or above.

- There are also big regional differences. Around 39 per cent of respondents in London say they would be happy to take out a loan to cover lifelong learning – compared to an average of only 16 per cent across other regions in England (dropping to as low as 10 per cent in the North East)

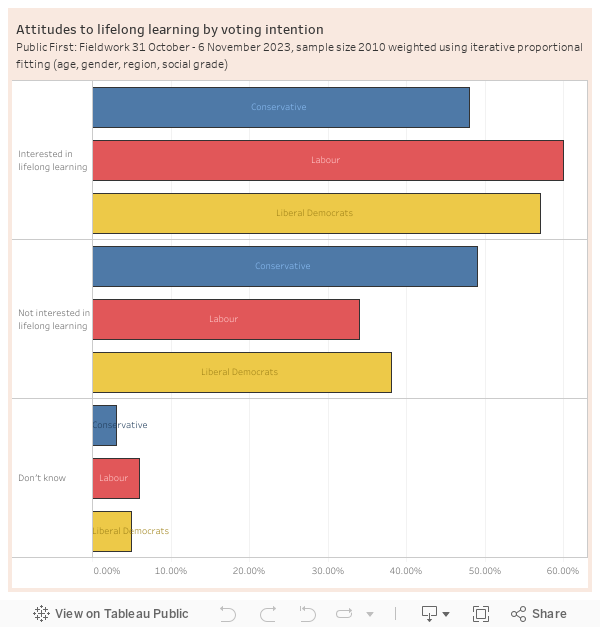

- There is relative consistency between social grade – and it’s clear that the factors driving difference of opinion are primarily age and previous education experience. As a result there is also a big political divide. So 52 per cent of those who voted Conservative in 2019 are not interested in lifelong learning, compared to 31 per cent of those who voted Labour. Looking to the next election, the idea of lifelong learning is much more popular amongst Labour and Lib Dem voters than Conservatives.

Target market

The polling shows that on the current trajectory for funding lifelong learning, we risk setting up a system with a lot of demand from the very people who have most recently been in education, are already highly skilled or who are already working for employers likely to invest in it.

This isn’t a surprise given the way our post-18 education system is set up. We currently have a model that is a bit like a long jump. You take a run up with education, hurl yourself into the world of work and see where you get before landing with a bump in the big sandpit of retirement.

As a result, changing careers or retraining already feels very risky for many. A recent study from the Learning and Work Institute shows that including lost earnings, it can cost up to £40,000 to retrain for a year. Most people don’t have that luxury.

What we need is a triple jump approach, gaining momentum with education at the beginning before hop, skip and jumping our way forward at different stages of life. It gets us further, we can adjust our course, and you might get a softer landing at the end.

If you believe, like we do at Phoenix Insights, that the reality is that many people will need to change careers over the course of their longer lives, then the demand for the LLE at present won’t tackle this challenge without a significant ambition to get those who would benefit most to take up the opportunity on offer.

Living for longer means we need to think differently about what you need and when at different stages of life. A decade ago we saw a big structural change in the way people save financially for their futures through the introduction of people automatically being enrolled in pensions. It has since become the norm for millions more savers.

Perhaps we need other defaults to help people prepare for their future and the changes it might bring. A cultural and systemic change to make lifelong learning the norm not the exception might be just the thing.

Polling from Jess Lister, Associate Director, Public First

Probably worth further unpacking the need for different kinds of professional learning – managerial, technical and inter-personal. The need for each may vary thru someone’s career.