Tracking the institutional impact of proposed OfS grant cuts

David Kernohan is Deputy Editor of Wonkhe

Tags

The Department for Education and the Office for Students had the combined bad grace to release a ministerial letter setting out recurrent and capital funding constraints for next year while I was on annual leave.

You’ll already be aware of Jim’s write up from the day it happened – what I wanted to do here (very much in catch-up mode) is to put some numbers on what this looks like at a provider level.

Any funding cut or reprioritisation is going to generate winners and losers. With such a lot of information in the public domain it is also fair to assume that those making the cuts are at least comfortable with their impacts on a local or area of provision level – if they were not, they would make different cuts.

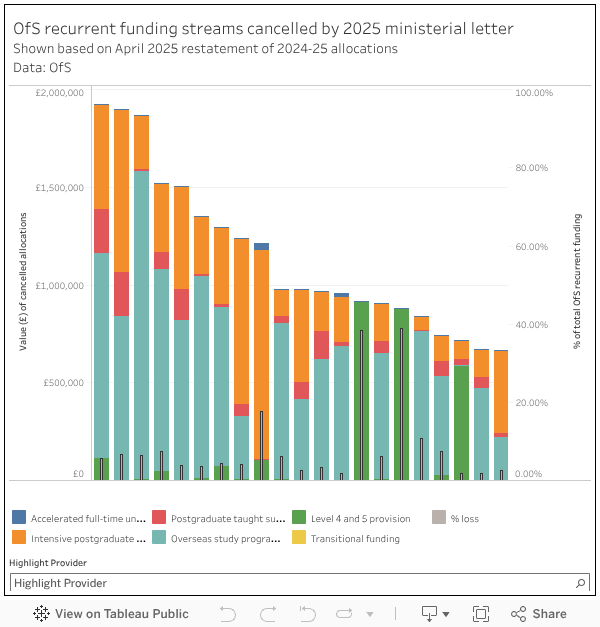

To start with we can look at the cuts to various funding programmes prescribed in detail by the minister.

Here we can see the value of the axed funding in the most recent (April 2025) presentation of the 2024-25 allocations. Larger Russell Group providers are hit in particular by the removal of the “overseas study programme” and “intensive postgraduate provision” supplements, but (as can be seen via the thin grey bars) this represents a small proportion of overall OfS income.

Of more concern is the impact of the removal of Level 4 and Level 5 funding, which as you may expect disproportionately hits providers of vocational and skills courses. For example, two large north eastern colleges (NCG and New College Durham) will lose nearly £1m each – which is more than a third of their total OfS income. The tiny (but very vocational) British Academy of Jewellery loses 44 per cent of OfS income because of this cut. There are many FE colleges and smaller private providers that will suffer here – even a small cut in funding represents a big proportional loss.

Only three providers see substantial income from the transitional funding for small and specialist providers who were not judged to be “world class” – though this £1m pot will be capped at £700k this year I’ve shown the full cut (which is surely the direction of travel here). In each case (Northern School of Contemporary Dance, Rambert School of Ballet and Contemporary Dance, Central School of Ballet) this income constitutes more than 80 per cent of direct OfS support.

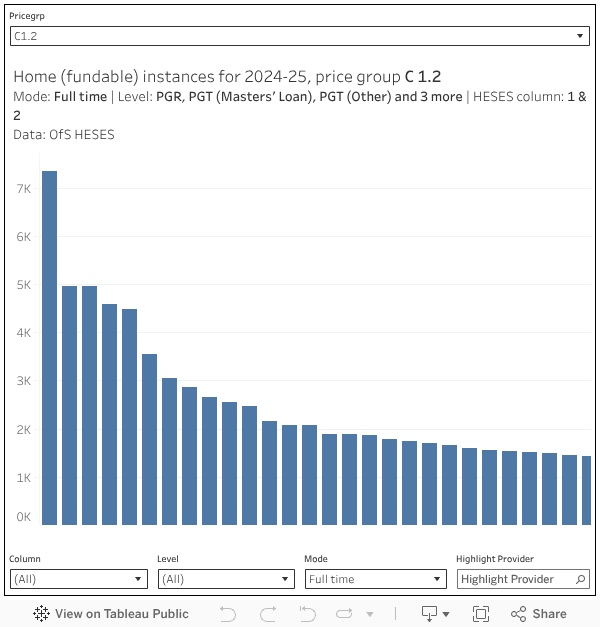

The removal of additional support for subjects in price groups C1.2 (the media and journalism provision that Gavin Williamson got so memorably cross about) will have a different set of impacts – the University of the Arts London standing to lose around a million pounds of OfS income, with a clutch of other modern providers not far behind.

The limitations of HESES data releases (seriously, OfS, you use FTE in funding calculations, why not release that as well as “instances”?) means that I’m basing this on full-time fundable home student numbers only – the actual totals will be higher when you include other modes.

I’m also not calculating the reallocation of this pot of C 1.2 funding (a hair over £17m allocated last time out) to provision in price group B (which was valued last time out at around £400m) – we don’t know all the details, and it is hard to imagine this extra 4 per cent making much material difference.

Though there is a lot of data in the public domain, we don’t quite have all the data we need to model the whole thing. In particular, we still (in 2025!) do not have data on the number of students studying via various types of franchise and partnership arrangements by subject of study. I have to hope that OfS does have this data, and would ask them very nicely to prioritise making a full open data release.

Franchise and partnership provision tends to be in business studies or the creative arts (both solidly ineligible for high cost funding) – so I would be surprised if a great deal of OfS funding flowed to franchisers in respect of unregistered franchisees in the hard sciences. But I suppose we shall see.