How can you get a maintenance loan and not a fee loan?

David Kernohan is Deputy Editor of Wonkhe

Tags

So here we are again.

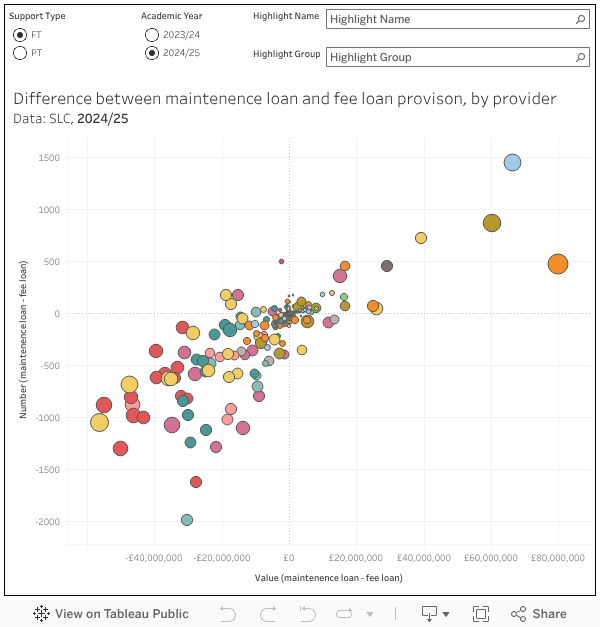

Every year, when the Student Loans Company releases data on fee and maintenance loans by provider, I track down instances where the students at a provider are drawing down more money in maintenance loans than in tuition fee loans – and where more students are claiming maintenance loans than tuition fee loans.

What does this show us? It is difficult to be sure.

For 2024-25 the maximum available undergraduate fee loan per student was £9,250 per year, which reflects the fees charged by pretty much all (Approved (fee cap) registered) providers providers who are able to charge it.

Maintenance loans are a different matter – the nominal maximum per student (outside of those living abroad as part of their course) was £13,348 at providers in London and £10,227 for those outside. In practice the antiquated design of the student support system means that very few students are able to claim these maximum amounts: you need to be from a household earning less than £25,000 a year to get the maximum, so the average loan paid in 2023 was £7,410.

This is why, even though the government talks about increases to the maintenance loan maximum as if this was putting more money into the pockets of students, in reality the amount of loan taken out is declining year on year.

So what would I expect to see in this plot – which lets us look at loan take up by provider:

The only legitimate circumstance where you can claim a maintenance loan without claiming a fee loan is where you are paying fees in another way. This is likely to apply only to very well off students (who can pay upfront), a small number of students who have their fees paid by employers, and students who cannot take up a loan for religious reasons. So, in most cases I would expect the number of students taking out maintenance loans to be no higher than those taking out fee loans.

Further to that, I would expect the number and volume of maintenance loans to reflect the socio-economic profile of each provider. If you disproportionately recruit well-off students they will take out less of their maintenance loan or not take out a maintenance loan at all – so the amount of loan taken out per student will be below the sector average. Conversely if you recruit less well-off students they are more likely to take closer to the maximum loan, so the amount taken out per student would be between the sector average and the maximum (though it is unlikely to be too close to the maximum).

That is not what we see.

The pattern reflects what we have seen in previous years – there are a number of providers where the number of students taking out a maintenance loan is higher than the number taking out a fee loan, and the total amount (in pounds) of maintenance loans is higher than the total amount of fee loans.

I’ve asked in various places, and I have still not been given an explanation as to why this happens.

One comment factor between the providers in this situation is that they are engaged in a large volume of franchise and partnership provision (so you see providers like Canterbury Christ Church University, Bath Spa University, and the University of Suffolk up towards the top left hand corner of the plot). But you also see Arden University, which has a large number of students but no franchise activity, up there – while you don’t see other providers with a big franchise population (like Oxford Brookes University).

One theory relates to students who leave their course at a point in their first year before fees become due but after maintenance loans have been paid – this is a very tight window (between enrollment, which triggers maintenance, and the tuition fee term one payment data) and is unlikely to explain a lot of the differences.

I’ve noted the average amount of each type of loan per student in each provider – Arden, Canterbury, Bath Spa, Suffolk and a few others have a substantially lower tuition fee loan per student, but it is difficult to find evidence of lower fees being charged by these providers (and anyhow, there are around 500 students or more at each getting maintenance loans but not fee loans).

So once again, I’d be interested to hear other explanations.

It is a shame that the OfS removed module results from the HESA return, as cross referencing those with the SLC data may well have shed more light in this area