Donelan returns with a way out of the student loans crisis

Jim is an Associate Editor (SUs) at Wonkhe

Tags

The latest to chip her oar in is pandemic-era universities minister Michelle Donelan, who told GB News yesterday of her big ideas:

The student loan repayment system isn’t working. I abolished real interest rates for new borrowers under Plan 5 so graduates don’t repay more than they borrowed in real terms.

What a deal!

But Plan 2 graduates are still being whacked with interest of over 6 per cent – higher than many mortgages.

Who could have caused that?

Plus, too many will be paying into retirement because their degree hasn’t led to a graduate job.

Yes, we’d not want people paying into their retirement.

In other words, they are being ripped off. And we need to face facts, many Level 4+ apprenticeships lead to stronger earnings than some degrees.

Sigh.

Oddly restrictive

As well as revealing that Dominic Cummings wanted to abolish the “laborious” Office for Students (OfS), Anthony Seldon’s Johnson at 10: The Inside Story describes the origin story of Plan 5 loans.

Officially posited as a response to Phillip Augar’s review of Post-18 fees and funding, it was really about then Chancellor Rishi Sunak’s “oddly restrictive vision”.

Despite much of the politics of HE of the period being driven by concerns about freedom of speech, Alison Wolf, who had been appointed to the No.10 Policy Unit to drive skills reforms, reveals that change was dictated less by culture than by finance:

Rishi had a driving ambition to reduce the cost of universities to the taxpayer and an absolute determination to reduce the [proportion of the] student loan book which was not paid back.

And he got his way. Slipped out quietly in a Parliamentary statement on Friday afternoon, on 28 January 2022 Donelan announced that the threshold for Plan 2 loans was to stay at £27,295. Pretty much nobody noticed:

Maintaining the repayment threshold at its current level, alongside the ongoing freeze in fees, will help to ensure the sustainability of the student loan system.

Then a month later her boss Nadhim Zahawi was thrilled to announce that he had delivered on the Conservatives’ manifesto commitment to address high interest rates by reducing interest rates for students … to RPI plus 0 per cent:

…ensuring that graduates, under these terms, will not have to repay more than they have borrowed in real terms.

How? By introducing Plan 5 – dropping the repayment threshold down to £25,000, and making graduates pay back for 40 years.

Substantial effects

In the resultant Spring Statement forecast, the Office for Budget Responsibility (OBR) looked at the measures – the freezing of maximum tuition fees, the freezing of the repayment threshold for Plan 2, lowering for new Plan 5, as well as the reduced interest rates for new borrowers and extension of the repayment term to 40 years for Plan 5.

It calculated that the measures would reduce public sector net debt by £3.7 billion by 2026–27, reducing public sector net borrowing by £35.1 billion over the period to 2026–27.

It said that the reduction in borrowing reflected the “upfront accrual of substantial effects on distant future cash flows”. In other words, by shifting more of the long-run cost of lending onto borrowers, the reforms would increase the recorded value of the student loan asset in the national accounts.

That allowed Sunak to fund an increase in the National Insurance Primary Threshold and Lower Profits Limit, a temporary cut in fuel duty, and various other cost of living measures, including a previously announced energy bills support package.

As such, while every other major change to student loan terms in the past where the cost had been pushed to graduates had resulted in increased upfront funding for universities and students, this time the Treasury had pulled off trousering the cash for other things. And barely anyone noticed.

Mulled whine

So Rachel Reeves might have been forgiven for assuming that a more modest package of threshold freezes buried in the budget would not be noticed. But the decision to leave Plan 2 interest at RPI plus 3 per cent while freezing the threshold again looks like it’s been the final straw.

Now we learn that Kemi Badenoch is “mulling a plan” to ease the student debt crisis “crippling millions of workers”. The Sun understands that Badenoch wants to “seize the issue as a vote-winner” while “rivals avoid it”. There could be a “cut in interest”.

What could that look like? Abolishing that hated “plus three per cent” on inflation for the interest rate for Plan 5 depended on two things – lowering the repayment threshold, and extending the term to 40 years.

The party would be brave to propose the former. But it might well do the latter – or at least offer graduates the chance to switch to Plan 5, or a version of it.

Doing so would instantly increase the value of the asset on the government’s books, and address the hated interest rate thing. But would the public, Plan 2 loan holders, and even Labour, fall for it?

That all comes down to the old “is it more like a loan or more like a tax” debate. The more it’s a loan – people pay loans back – the more regressive it is overall. The more it’s like a tax – the richest pay more to subsidise the “insurance” features for less successful grads – the more progressive it is.

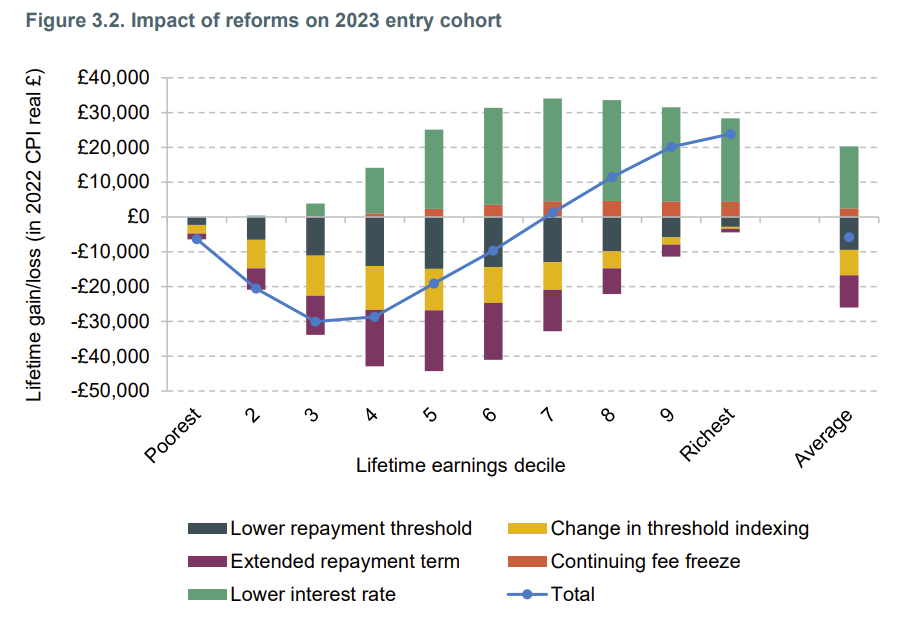

Here’s how the IFS characterised the switch to Plan 5:

As well as the Tories mulling over their position, No.10 is now said to be involved in talks with the Treasury and DfE to see if a sticking plaster can be found to get Plan 2 graduates out of the broadsheets.

A regressive sticking plaster is in one corner, and a more complex set of changes that retain the overall progressivity of a system is in another. Which will be chosen?

Whatever can be afforded and is more consistent with other students. Loans should not be used as a mechanism for equality of opportunity.

We need a politician to be far braver and stop young adults with lower Prior academic attainment from being mis-sold degrees that won’t do then any good and loans that are only going to blight their finances and cost the tax payer a fortune in loan write offs