If you’re a think tank as august as the Institute for Fiscal Studies what you say is taken seriously.

There’s a lot to commend in this morning’s report on the current and future state of sector finances – not least the expression of uncertainty that means an £11bn central sector loss scenario could be as low as £3bn or as high as £19bn.

That uncertainty itself is a worry. Planning for each of these scenarios, which will have an impact on different providers in very different ways, requires immediate action – but a different action is needed in each of these three indicative cases. And the variation of all plausible scenarios is, of course continuous within this range, not discrete.

Scenario planning

Before we dive into the detail I think it makes sense to spell out how each of these scenarios has been arrived at. This is a tabulation based on Annex A of the report.

| Variable | Optimistic | Central | Pessimistic |

|---|---|---|---|

| International and EU recruitment | -25% | -50% | -75% |

| UK undergraduate recruiment | 0 | -10% | -20% |

| PG recruitment | 0 | 0 | -10% |

| Accom/catering months at 0% | 4.5 | 6 | 7.5 |

| Pensions provisions | 0 | -25% | -50% |

| Long-term investment value | -5% | -10% | -15% |

All these scenarios share the assumption that accommodation and catering income for the rest of the year will decrease proportionately with lost recruitment. And the government’s recruitment cap has been modeled in each case as 25 per cent of applicants choosing to go to a higher ranked (CUG league table) provider than they would otherwise, up to a 6.5 per cent (forecasts assumed at the unsafe 1.5 per cent average – the figure refers to the average forecast for providers similar to those that do not have a forecast, not all providers) plus five per cent.

So how do we feel about these scenarios? They’re not bad, but I’d quibble about the low expected change in PG enrollment (surely an uncertain year is not the best time to do an expensive one year masters – especially one that is based in a lab). It’s the international numbers that do the most damage to the finances of international providers.

And if we assume university owned accommodation and catering has made no money since Easter (12 April) that’s just over four-and-a-half months till 1 September (the likely start date for contracts), making the optimistic scenario the most likely option by far.

It’s also worth unpacking the pensions provisions. IFS reckons that

The downturn in financial markets is expected to lead to large losses for defined benefit pension schemes, requiring universities to contribute additional funds to make up the deficit, and to recognise the net present value of these future contributions as a balance sheet provision.”

The central projection is based on emerging data from USS and the March 2017 valuation that underpins the 2019 accounts that were finalised on 31 Jan last year. It’s worth remembering that the 2020 valuation is expected “to paint a much more negative picture” of the health of the scheme

By provider

The £11bn central scenario is the basis for most of the analysis. This breaks down in two ways – by nation (£9.2bn in England, £1.1bn in Scotland, £0.5bn in Wales and £0.1bn in Northern Ireland), and by type of loss (£5.7bn of operational losses, £3.8bn on additional pensions provisions, £1.8bn losses on long term investments).

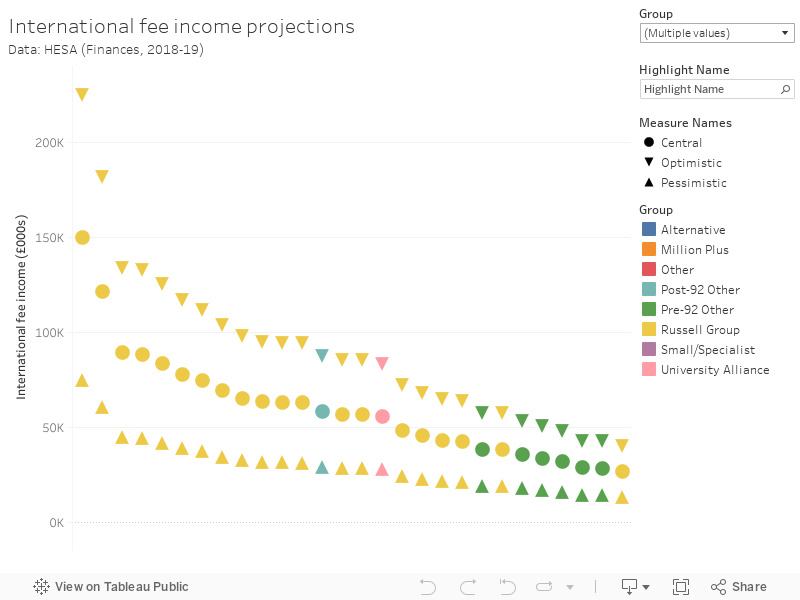

As above, it’s international student numbers that are the biggest predictor of the overall provider level loss – representing a large chunk of that £5.7bn in fees, and having a knock on effect on the rest (for example accommodation income). This means that the proportional level of historic international fee income is a decent indicator of the amount of damage to a university balance sheet.

I’ve plotted stuff like this before, so the above is just a rejig of what is already known from HESA Finance open data. If you’re observant you’ll spot that I’ve plotted international students not including EU students. This is important for a 2020 projection because this is the last year EU students are eligible for the home student support package in England – and to my mind the IFS should have used the EU numbers as a determining factor for home recruitment, taking a proportion of EU numbers off the home plus EU total before comparing to the cap.

The overall losses for each provider are compared to historic financial net assets (not liquidity, the report noting that government seems very keen on liquidity), drawing on a third-order autoregressive model estimated on net income data between 2015 and

2019, with pensions and investments handled separately. Again, as those familiar with HESA finance data will be well aware, a shaky balance sheet is not generally related to international student recruitment – most of the institutions at the tail end of IFS’s ranking (which – sensibly – is not published with provider names included, though it would be reasonable easy to figure them out) are not those disproportionately affected by international student recruitment dropping.

Designing a bailout

This leaves us with a moral conundrum around the design of any bailout. Do you address losses from international recruitment – which would direct funds to providers who have lost a lot of income yet retained solvency – or directly address the danger of solvency – targeting funds at historically financially weak providers who would be at risk?

In all there are 13 providers who would have negative long-run assets per student in 2024, mostly from the lower end of the CUG league table or specialist music and arts providers. There are some smaller institutions in there, though one has about 24,000 undergraduate students.

Bailing out just these 13 back to solvency would be cheaper (£140m rather than the £3.2bn that UUKs proposal – doubling QR and providing full economic costs for government funded research – would cost) but would be exactly the kind of bailout of struggling providers that DfE and OfS have set their faces against.

Another bailout proposal – adding £1,000 to fee income per student, would be quite expensive (£1.8bn) and would only return three of these 13 providers to solvency.

There’s a calculation of potential university cost savings too – IFS calculate that under the central scenario universities could save £0.6bn in total: £0.2bn by intelligently using the furlough scheme, and – more painfully – not renewing some teaching (£0.2bn) and non-teaching (£0.3bn) temporary contracts. Only 5 universities would claw back more than a third of losses in this way. The report does not model redundancies, suggesting that:

Redundancies are expensive, procedurally difficult for many universities, and could be associated with reputational costs, especially if academic staff were made redundant.”

In conclusion

The report concludes that the impact of Covid-19 (and, of course with the brexit impact on top) will

lead to substantial losses for the higher education system [though] the university system as a whole is well placed to shoulder these losses”

That last point is based on a calculation of a pre-Covid £9bn operating surplus and around £45bn in reserves, but it is noted that neither these assets or the expected losses are evenly distributed. The calculation of a whole sector position here is not particularly helpful – I don’t think anyone is anticipating providers pooling resources in this way in this age of (government mandated) competition for students and income.

Despite some jaw-dropping figures for sector losses, the risk is left where it has always been: with financially weaker providers – particularly those who have begun to grow their international student intake in an attempt to raise income.

We’ll likely find out soon what the government approach will be in these situations – debt restructuring, mergers, or a managed wind-down and teach out being three likely options. But the option for a bailout is there – either directly, or via a wider Augar-inspired reconfiguration increasing funding for courses below degree level. Many at risk providers would be well placed to benefit from such measures.

Couldn’t the issues for specialist art, music and drama providers be addressed by renewing the Institution Specific Teaching Allowance scheme, which assessed both the need and the educational case for extra funding?

I think the scenario regarding pgt, which i assume is home students here, is pessimistic. Higher education demand is counter cyclical. Weak graduate employment prospects are a major incentive to re enrol. Of couse this will mostly benefit particular universities and only some subjects.

Let’s not forget some universities have been reducing home admissions to make room for international students at higher fees. And to become more exclusive to boost tariff. Thus reducing WP targets. If you play such games the public will notice and might not be so sympathetic?

Rather than these at risk Universities closing I expect to se a number of takeovers – perhaps dressed as mergers to make them more PR friendly. Bigger universities get ‘off campus’ sites and student numbers, significant reductions in Admin staff and the opportunity to sell off land and buildings, often in or near town centres, where many of these struggling Universities started life as polytechnics.

When you hover on the icons in the plot, I think the labels in the box are the wrong way around. They’re the opposite of what the symbol key and plot suggest (i.e. higher number = optimistic).