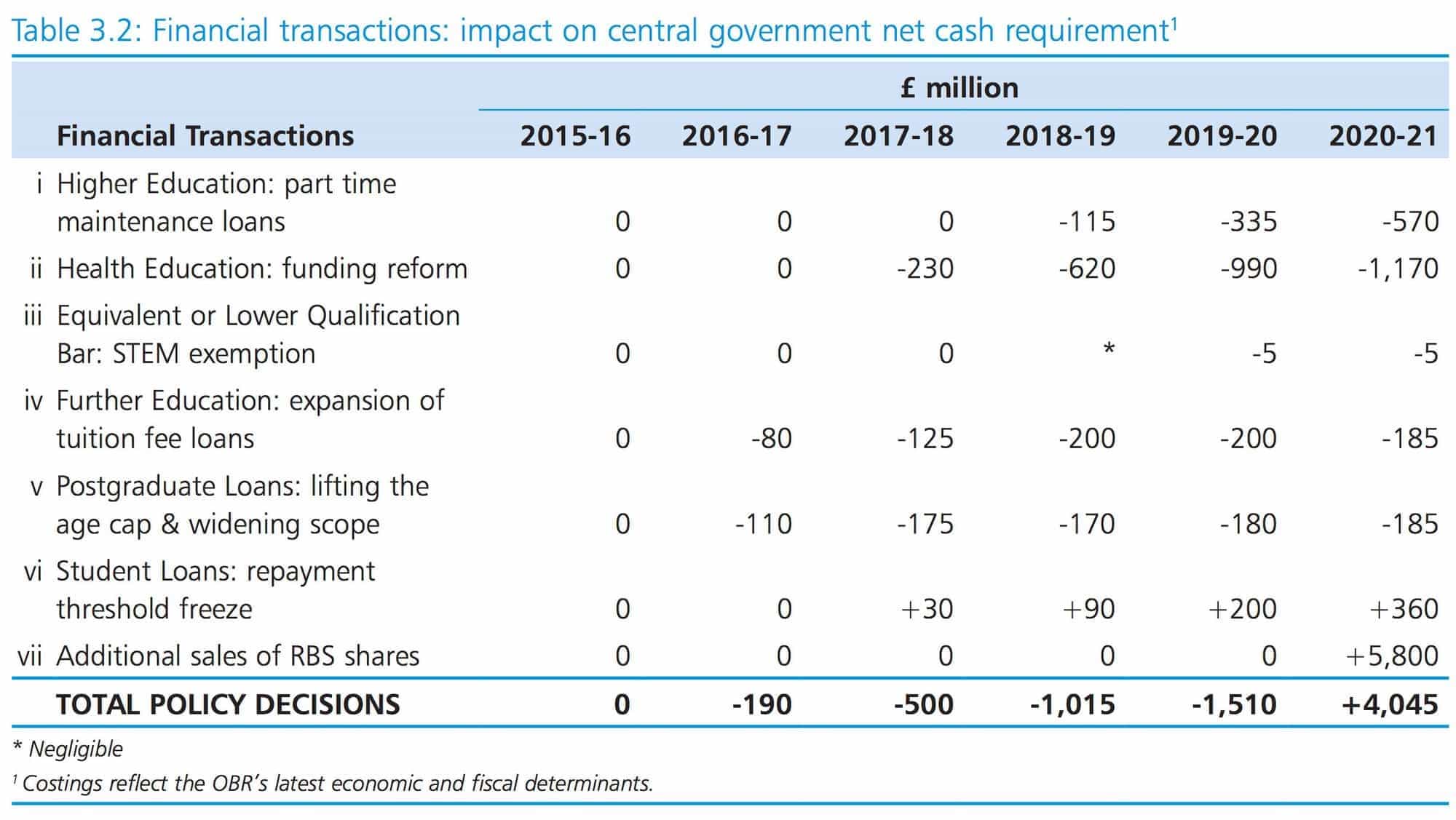

Wednesday’s Spending Review saw lots of announcements about loans. Maintenance loans for part-time students from 2018/19; postgraduate loans confirmed from 2016/17 and with a qualifying age cap lifted to 60; loans for nursing students to replace grants from 2017/18; lifting of the Equivalent and Lower Qualification bar from STEM subjects from 2018/19 enabling access to loans to fund a second degree; loans extended to high skill and professional FE courses offered at Levels 5 and 6.

The government expects over 300,000 students to be affected by these changes. There is little detail as yet on many of the assumptions or mechanics but the cashflow impacts have been sketched by the Treasury and can be seen in the table below, taken from the Blue Book. The OBR has described the projections for FE take-up as ‘very uncertain’ and the changes to part-time and postgraduate funding appear to have been finalised so late that no normal supporting analysis was provided.

Spending Review & Autumn Statement 2015

All in all this amounts to roughly £2bn of additional loan outlay by 2019/20 and that’s on top of the switch from maintenance grants to loans announced in the July Budget. UK loan outlay will hit £20billion annually in three years.

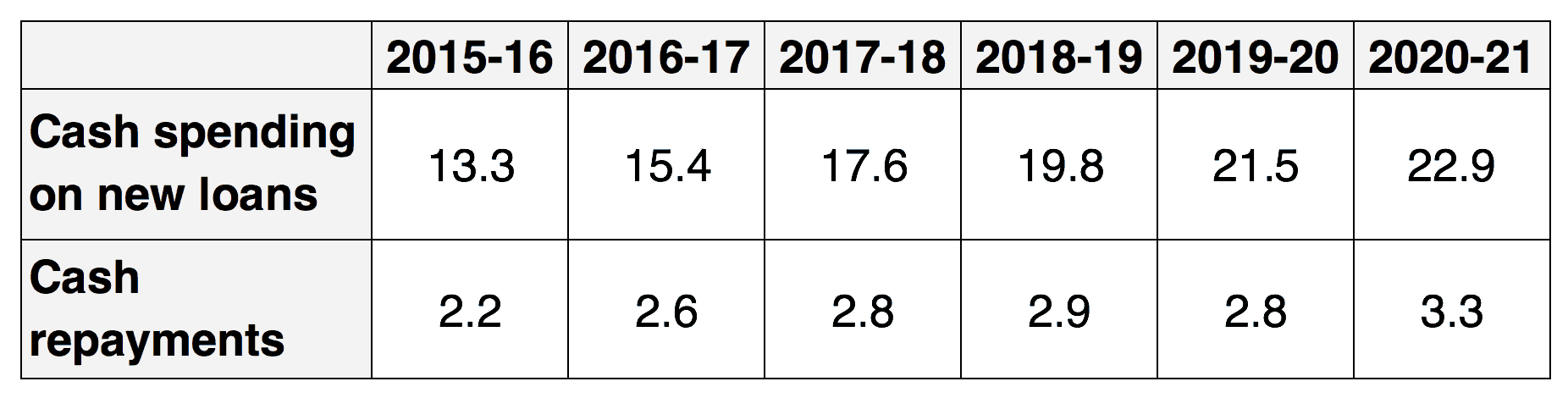

£ billions – OBR, Economic & Fiscal Outlook November 2015, Table 4.29

The amount by which annual repayments fall short of cash outlay on new loans is covered by government borrowing additional to that generated by the ‘deficit’. So, for example, on these projections the government is forecast to issue £110bn loans over the next six financial years and receive back only £16bn. £94billion will therefore be added to public debt from student financing alone.

‘Managing the loan book’ is increasingly a central policy concern with yesterday’s confirmed freeze to the repayment threshold setting one precedent for future governments.

The vast majority of new loan outlay is attributable to English HE – the loans issued by the rest of the UK come to about £1.5bn annually on these projections. The Department for Business Innovation & Skills will therefore be taking main responsibility for the outlay.

There was however, something lacking from this week’s announcements and figures. Typically, BIS would, as part of its settlement, receive an allocation to cover the amount by which the value of new loans created is deemed to be lower than the cash used to create them. This is the Resource Accounting and Budgeting (RAB) charge. Though often discussed as some form of external performance indicator, the RAB charge, as its name implies, is central to the budgeting process. It is a resource that is allocated and utilised.

It has become a byword for artificiality – we are on the third set of conventions governing its use since 2010 – but its position as a budgetary measure tells us something about the relation between the Treasury and BIS. Budgetary devices are a management tool and when it last changed the relevant conventions in 2013/14, the Treasury did so in order to incentivise BIS to address problems that had arisen with student loans.

In the Spending Review, BIS was allocated its resource budget, but no figures for RAB were published. Instead a placeholder baseline figure of £4.4billion per year was entered for each forecast year.

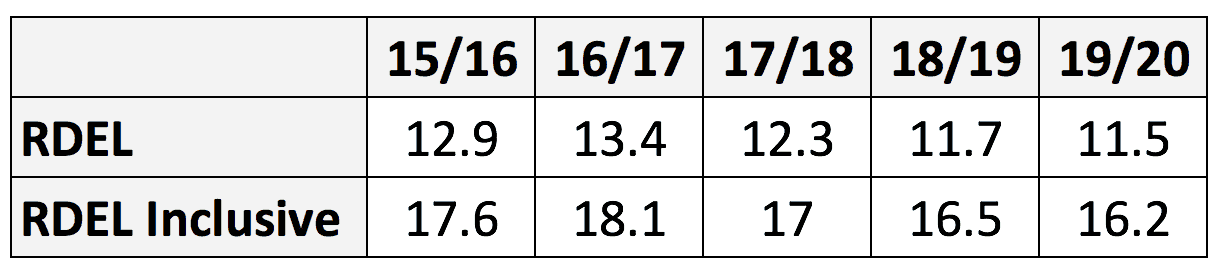

BIS’s RDEL inclusive of non-cash elements such as RAB is published in an Appendix to the Blue Book. A footnote states that RAB was £4.4bn for 2015/16 but no further information is presented. From the figures published inclusive and exclusive of non-cash we can see that non-cash in total is stable at around £4.7bn over the forecast period.

£ billions

With loan outlay rising over this period, that allocation would not make sense under current arrangements. In recent years BIS has been under ‘fiscal pressure’ because its budget allocation for RAB has diverged from revised estimates of likely repayment. For instance, the budget allocation for 20114/15 was set in 2010 at £2.9bn – when 2014 came around new modelling indicated that a higher level would be needed. As a result, some complex arrangements were set in place which turned ‘excess’ over budget allocation into a cash penalty to BIS’s other spending.

BIS has confirmed to me that they have not as yet been given RAB allocations for 2016/17 and beyond, but that these will be confirmed at the Spring 2016 Budget.

The obvious explanation for this is elsewhere in the Spending Review. The government has decided to change its ‘discount rate’ for student loans from the current level of RPI plus 2.2% to RPI plus 0.7% so as to bring the discount rate in line with the government’s cost of borrowing (as recommended by David Willetts’s recent pamphlet). The Blue Book states that this should – in conjunction with the loan repayment threshold freeze – reduce the current estimate of the RAB charge from 45 per cent of loan outlay to 30 per cent. See below for an explanation about discount rates.

One can see that at first sight this would reduce the RAB needed for £20bn of new loans down from £9bn to £6bn. No direct cash impact would be seen as it is just that the government has changed the way it values the estimated future repayments, and rejigged budgets accordingly.

A change to the discount rate would not create ‘spending headroom’ and what is allocated would be lowered accordingly (hence accusations of chicanery). What we would learn though from these allocations is whether the Treasury is still ‘incentivising’ BIS to improve loan performance further (and how strongly). It may be that this change heralds yet another change to budgeting for student loans from 2016/17.

So, in conclusion, because so much hangs on loans these days we won’t really be able to assess how BIS did out of this funding settlement until we see the RAB allocations at the next Budget. The change to the discount rate will however force the political discourse around loans to adjust. In truth, the financial sustainability or otherwise of the financing system has been altered at root by the precedent created by freezing loans – BIS and the Treasury will be actively managing the level of repayments generated by loans. The RAB allocations tell us whether further tightening is to be expected in the near term.

Besides the budgeting issues, there is another implication from changing the discount rate. All the existing loans held by BIS (and by the devolved administrations) would go up in value significantly overnight. BIS currently has responsibility for a loan book with a face value of £64billion (as at the end of March 2015). That is the outstanding balances of all borrowers come to £64bn. BIS estimated the worth of those loans – the repayments that would be generated by them – at £42bn based on the RPI plus 2.2% rate. BIS has confirmed that this revaluation will be carried out during the preparation of the departmental financial report for 2015/16 and will be published in July 2016. At a rough estimate we could be looking at an increase close to £10bn.

Good news for the government balance sheet, right?

Not as much as you’d hope. By a quirk of the national accounting statistics – illiquid financial assets, like the loan book are excluded from the calculation of Public Sector Net Debt, while the borrowing used to create them (outlined earlier) is included.

Osborne’s secondary fiscal mandate is to have debt falling as a percentage of GDP every year of the forecast period. The spurious justification offered for the loan threshold freeze was that this measure constituted a measure of the affordability of English higher education. To be clear, the affordability of English higher education financing ought to be determined by a long-run economic assessment, not the short-run presentational scores of HE in a set of statistics.

But, that aside, there is a final point to be made. Revaluing the loan book determines the level of loss or profit made against a sale price. The government has again delayed plans to initiate a five-year programme of ‘pre-2012’ loan sales. If it does manage to shift a tranche in 2016/17, its loss will now be higher given the upwards move in value against price (the private sector purchasers won’t have moved their own discount rates much). As you probably know, that the government loses money doesn’t necessarily mean that a deal won’t pass a ‘value for money’ test.

As the loan book trebles in size its place on the government’s balance sheet is transformed. BIS insists that proceeds from any loan sale do not directly determine BIS’s budgets but its hard not to see that a further tightening of loan terms may be the precondition for the abandoned dream of the 2011 White Paper: a rolling sale of each year’s new loan issue. As can be seen from the figures above, the central estimates of £12bn raised by a five-year sale programme is swallowed up by one year’s cash requirement.

Discount rates explained

£1 today is not the same as £1 received next year and again those both differ in value from £1 received in ten years’ time.

The government uses a ‘discount rate’ to measure the worth of repayments projected to be received in the future. Their value is affected by their timing.

A discount rate can cover the cost of borrowing, inflation, a risk premium or reflect the value of alternative uses to which I can put that £1. The government’s financial budgeting and reporting discount rate is RPI plus 2.2% per year. For student loans, that rate will be revised down to RPI plus 0.7%.

The example below shows how a stream of cash payments is valued differently by different discount rates. RPI is assumed to be 2% per year over the ten years.

The cash sum does not change – £100 is received as 10 payments of £10, but the lower rate of RPI plus 0.7% values the total sum of repayments at £86.56 as compared to £80.13 on the higher discount rate.

If £100 had been issued to a borrower on these terms, then the RAB on the old discount rate would be 19.9% – the new, lower discount rate improves the value of the repayments so that the RAB would be revised down to 13.4%.