Looking at sector income last week was only really one side of the story, so this time I’m bringing in expenditure too.

After some serious discussion about institution financial instability, we’ll start there. Again, we’re in England only – but other jurisdictions will get their turn soon enough.

A surprising number of sector agencies model their institutional financial position, and many affix a score or rating to this assessment. These scores are almost never made public, but are used in policy decisions around how institutions and students are supported in times of financial pressure.

Ratings and data

When I worked at HEFCE we had institutional financial health ratings for every institution – making for the most niche set of “top trumps” that have ever existed. The underpinnings of these ratings now form the basis of OfS registration assessment against condition D – and it is notable that of 180+ institutions accepted onto the register, none have been warned about their financial position. So talk of imminent bankruptcy and living month-to-month should probably be left to the headline writers for the moment, although when such a condition is placed on an institution in the future, all bets are off.

HESA, too, has a financial security index, which you lucky folks with HEIDI+ access can play with to your heart’s content. We’ve not reproduced it here, as it is available to subscribers only. But it takes a serious accountant-style look at one angle on sustainability and is as rigorous and even-handed as you would expect.

The reason for all this secrecy should be obvious – speculation about the viability of an institution affects income and day-to-day business. Would you apply to an institution with a financial warning in place? Would you apply for a job there? Would you fund research there?

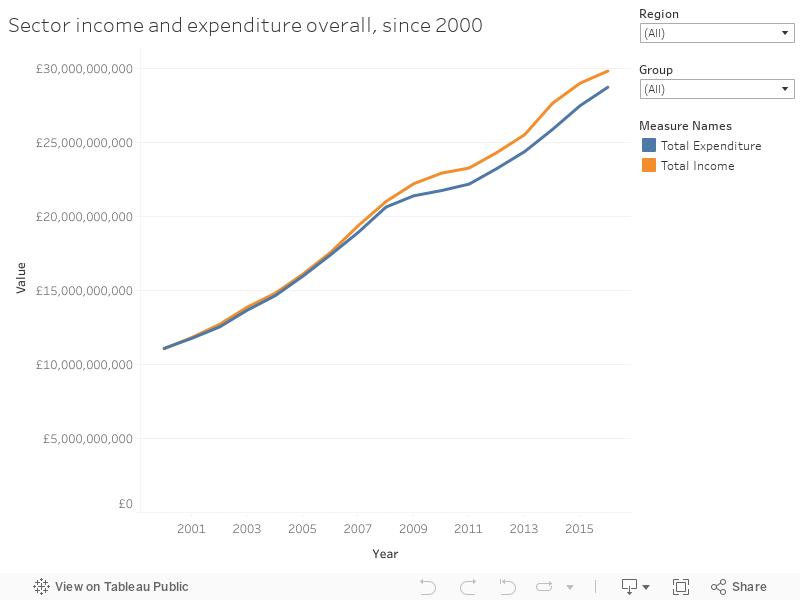

In year surplus and deficit

The simplest way of looking at overall institutional health is simply to look at the difference between annual expenditure and annual income. Both these figures are available from HESA (and I am again grateful for its support). Here’s how the sector looks overall:

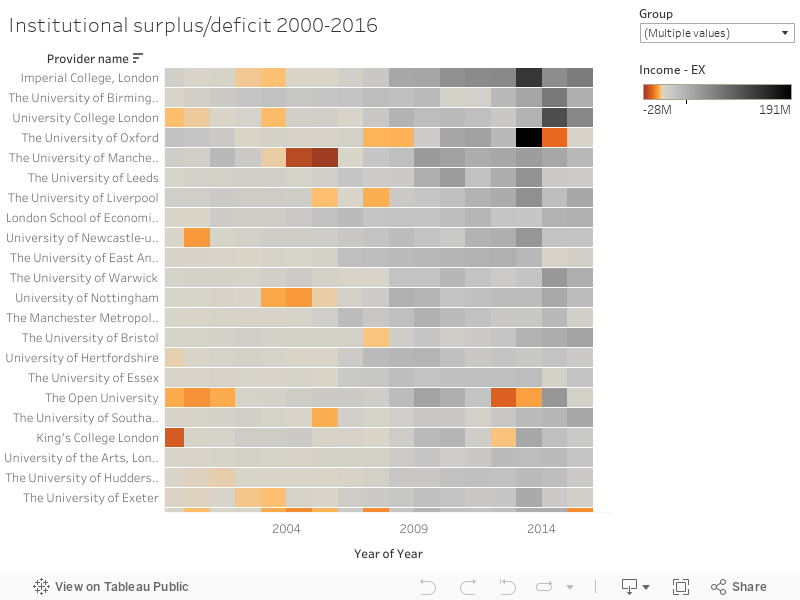

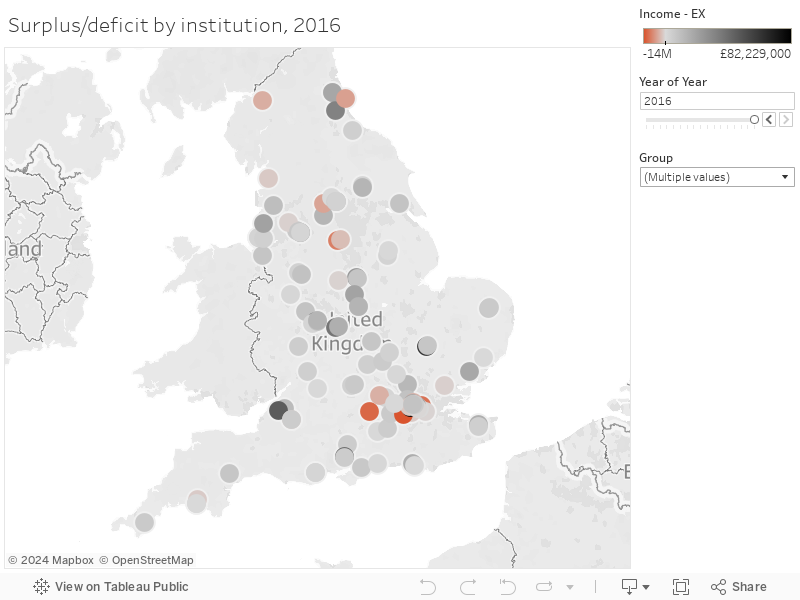

To look at year on year institutional performance, I’ve built a table and a map. The table is sorted by the total balance over the 18 years of data I’ve used, and you can scroll year on year through the map with the filter.

Of course, this is only one part of the story. As well as the current account that these figures represent, institutions will have a savings account and other assets that may be brought into play when expenditure rises suddenly. There’s also the option of borrowing.

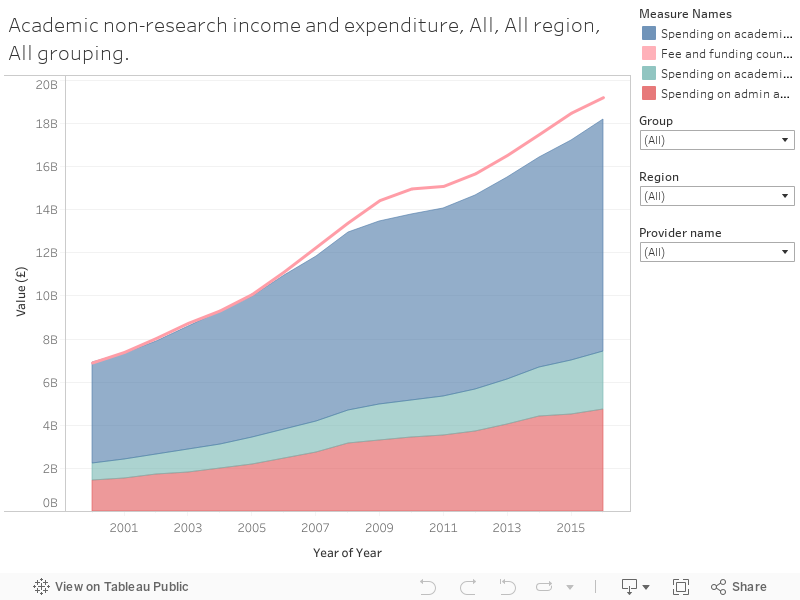

Types of expenditure

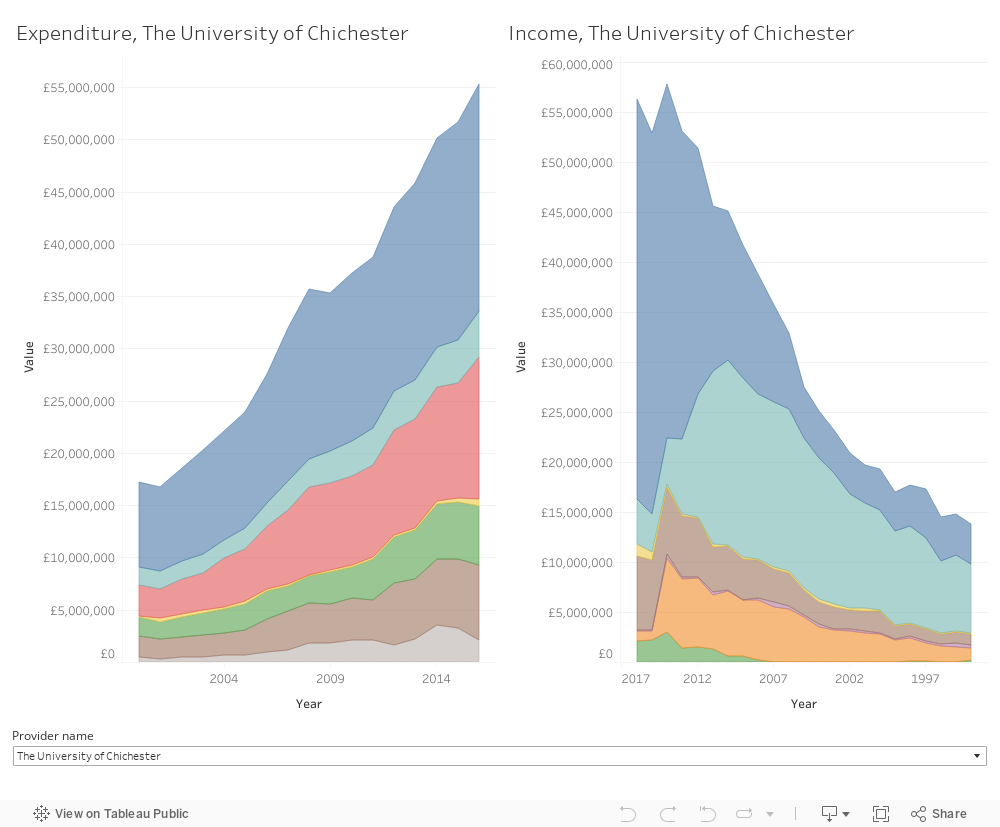

So what do our universities and other HEIs spend their money on? This first double graph looks at expenditure (left) and income (right). The axes don’t match up, but using the mouse will show you the values attached to each area and you’ll get a sense of the overall shape and growth of both since the turn of the millennium.

Matching income and expenditure lines that are linked is tricky. Cross-subsidy is sometimes seen as a dirty word when academics feel their research income is supporting what they perceive as needless central administration – less so when the stellar performance of the catering and residences teams keeps a department open.

Non-research is a messy category that broadly correlates to teaching, but includes third stream and QR on the income side, and central admin (you know, registering with the OfS and doing mandatory data returns, that kind of thing) on expenditure. This grouping (which is rough and pretty arbitrary, if I’m honest) demonstrates that there is largely a surplus here when we look sector wide, but not everywhere – many research intensive institutions make a loss here.

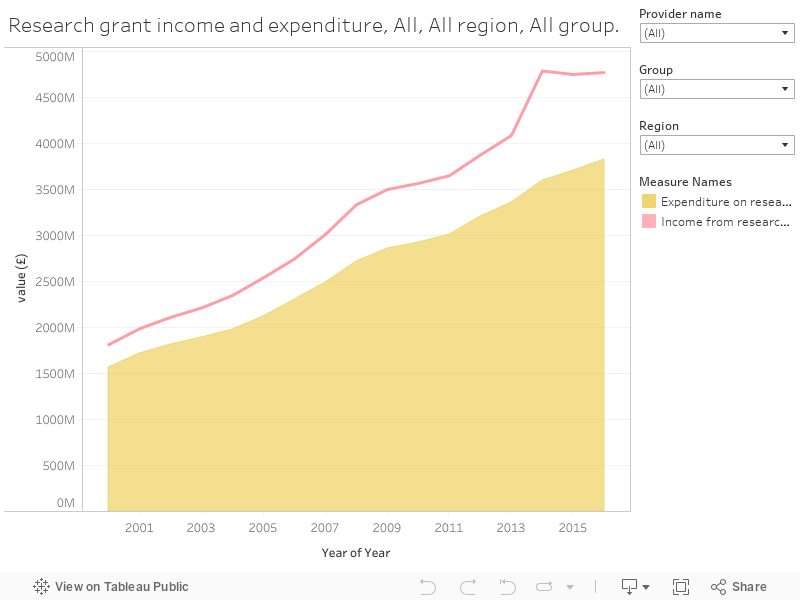

If you land a research grant or contract, you have to pay overheads – for all the things you need to complete the work, such as a functioning university and department. This graph shows, perhaps more surprisingly, that sector wide there is a surplus here too – with most institutions avoiding a loss.

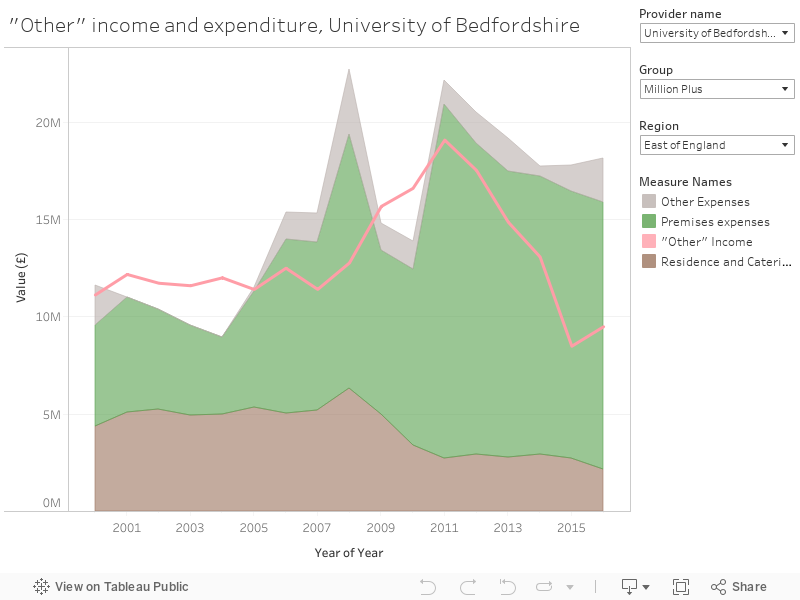

The last category is included mainly for completeness’ sake. “Other” is a big and messy category, and generally the mass of premises expenses make for a loss.

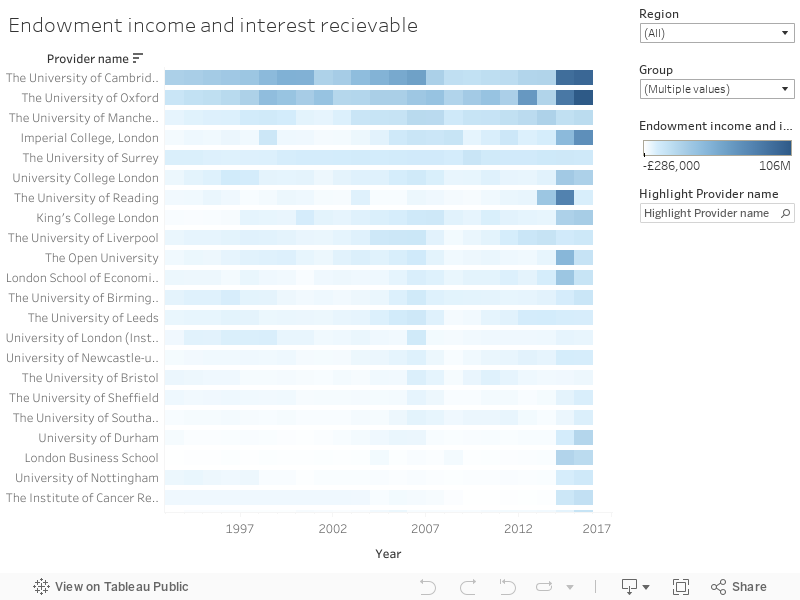

Endowments and borrowing

Those of you old who were around for the the 2003 White Paper will remember the push for universities to build up US-style endowments – charitable giving to support an institution from commercial donors or, maybe more controversially, wealthy alumni. But endowments are still concentrated in a few older, research-led institutions.

Borrowing, now that OfS have taken away some of the restrictions and barriers, is a growing part of sector finance. At present loans are available at reasonable rates, not least due to a persisting presumption that institutions are government backed. Moody’s rate most of the small number of mainstream universities it looks at at Aa3 with a negative outlook – Oxbridge are Aaa and stable.

This makes it both easy and attractive to borrow money to “sustain the level of capital investment needed to attract students and staff, universities are increasingly financing capital expenditure through external borrowing as levels of publicly funded capital grants reduce”. The question is whether it will last.

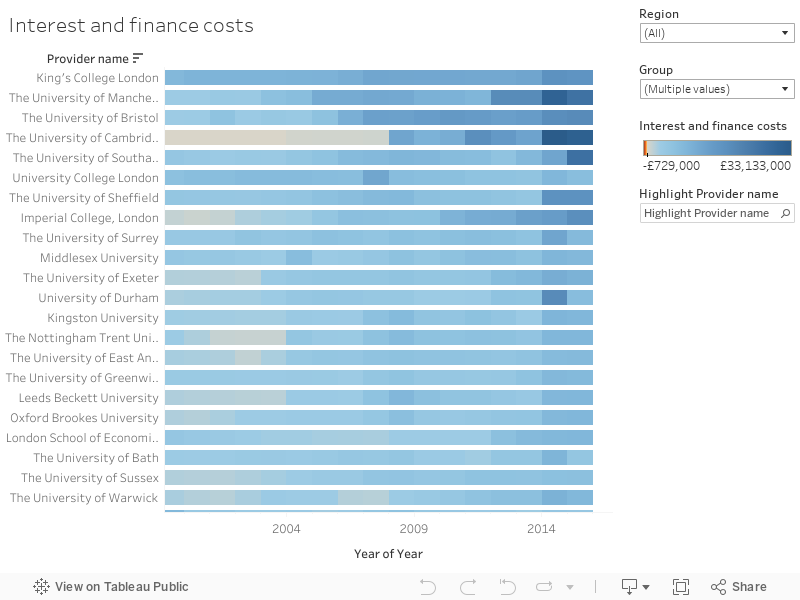

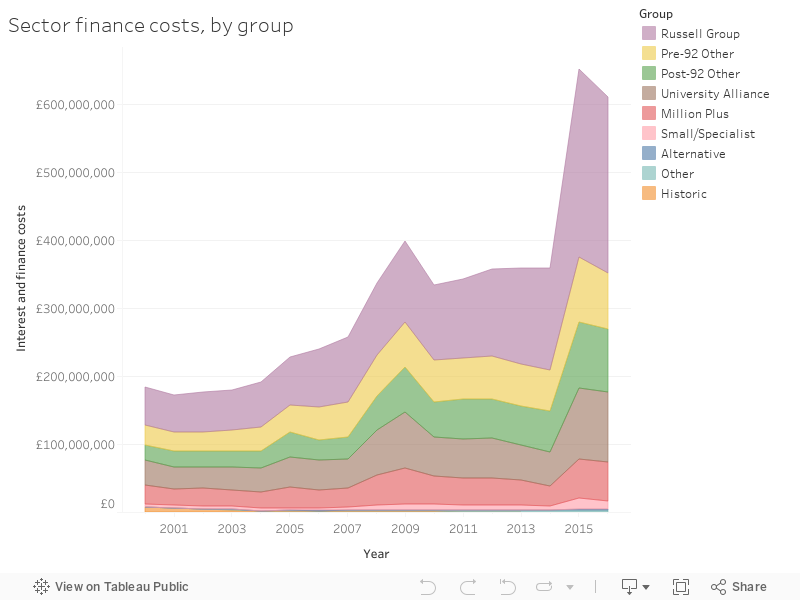

HESA doesn’t collect totals of institutional borrowing (maybe it will one day) but we can see figures for the cost of finance (basically interest and other fees). Here’s an institutional table, and a look by institutional grouping.

And here’s a look at finance costs in the whole sector, by group:

Borrowing can be used for many purposes – short-term bridging loans that cover unexpected expenses, the longer-term investment that pays for a shiny new building. At the moment the sun is shining and institutions are borrowing rather than saving. But these loans need to be repaid, or at very least rolled over. Of all the data I’ve shown you here, if I were going to stay awake worrying about one measure, it would be this.

Find part I of this series – institutional income, here.

Data notes

Thanks again to HESA for their support in obtaining the data that makes these time series possible. My comments on historic identifiers from last week still apply, so any errors are my fault. For further information on precisely what each field means, please see the relevant HESA coding manual.

Excellent – thanks!

Fabulous work David. Both this and the earlier income article are a superb analysis and use of charts.

However, like you I was surprised by view expressed by the research expenditure chart. The narrative seems to imply that this chart includes overheads such as administration and premises and after these there’s a surplus on research income…but that’s obviously not the real position. The institutional and sector’s TRAC analysis shows clearly that on an fEC basis research consistently shows asignificant deficit.

Hi Bob – there are a number of different ways of looking at this – as I hope the article gets across. Clearly much cross subsidy is hidden within lines like central administration – but the big story is that data collected for different purposes tells different stories.

Interesting article and great charts.

It’s possibly worth making clear that “sector” and “institutions” in this case refers just to universities. OFS will be regulating a wider group of HE providers including colleges with HE provision and private HEIs. Colleges are regulated mainly by ESFA (which still uses a version of the financial health top trumps) but some of the private HEIs aren’t regulated by anyone else apart from the financial markets and can be thinly capitalised.

The fact that OFS hasn’t issued a Condition D financial warning is some comfort but it’s worth remembering that anyone outside an institution can only rely on financial statements and forecasts presented by those within the institution. Any institution that has taken on a bank loan will have signed up to terms and conditions which it may breach. When this happens (eg when the financial statements are completed), the bank may take a decision which could push the institution into difficulty quite quickly.