One of the many things that appear to be missing from the Lifelong Loan Entitlement (LLE) debate is the fact that the higher education sector puts on an awful lot of short courses already.

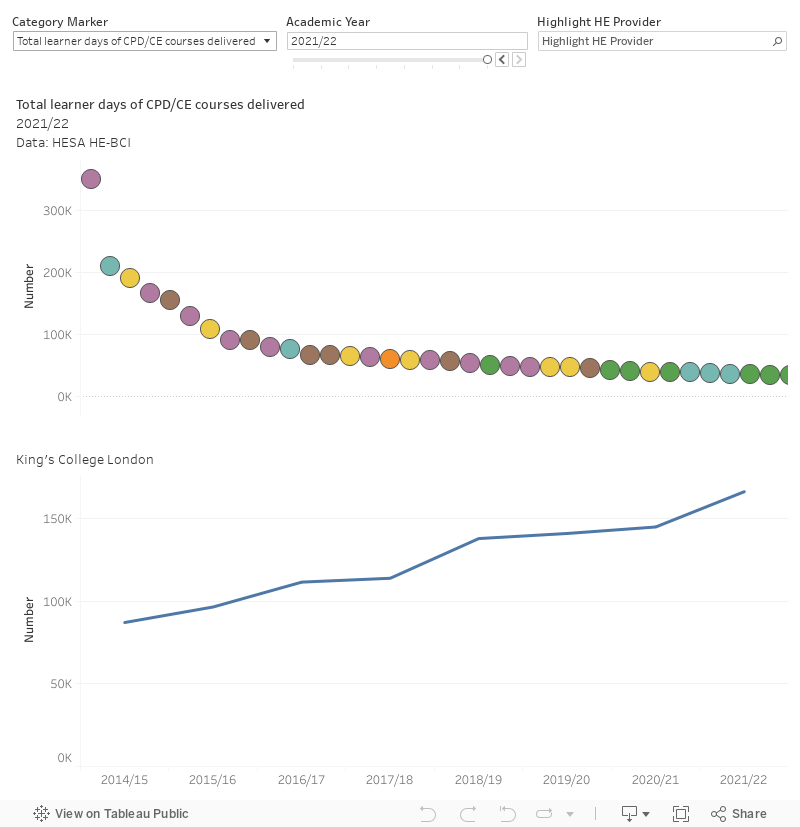

According to the most recent (2021-22) year of HESA HE-BCI data, some 3,282,792 days of continuing professional development (CPD) and continuing education (CE) were delivered by higher education providers in England – bringing with them a cool £570m of income.

Course costs

Here’s where it is happening, and if you mouse over the dot showing a provider you can also see how it is growing:

The official definition of CPD is: “Training programmes for learners already in work who are undertaking the course for purposes of professional development, up-skilling, workforce development”. Continuing Education refers to provision where the students are not taking the course as a part of their employment.

This, to be clear, is not always provision that offers higher education credit – and may (in the numerical measures at least, for provision below higher education level income is not returned) reach below the first year undergraduate level (L4) in content.

Fee waivers?

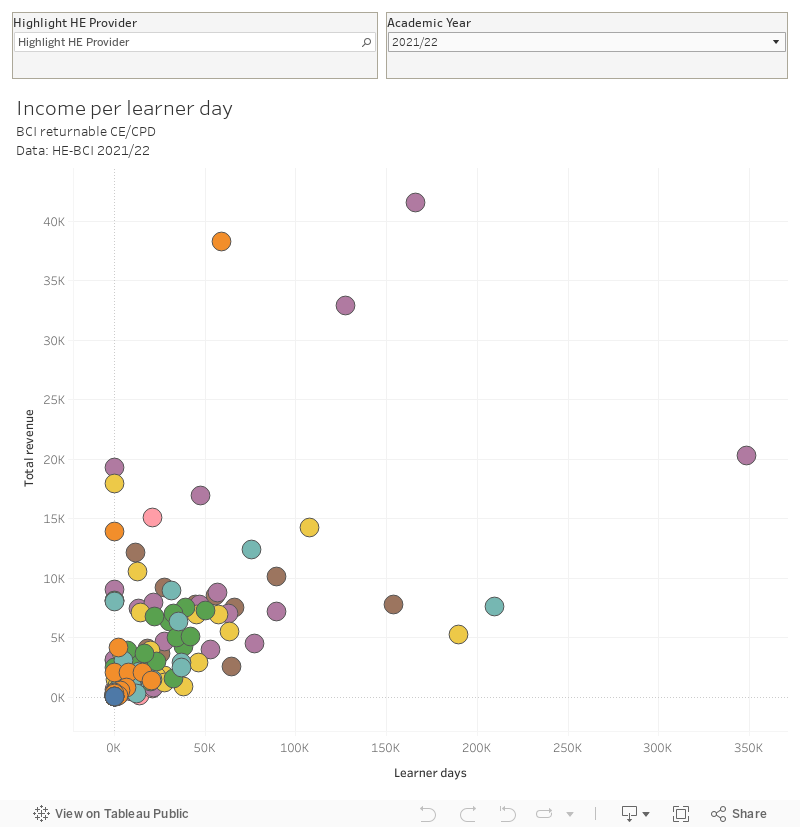

The “days” part of the calculation refers to 8 hours of learning. You might recall that we put the cost of higher education single credit (10 hours) at a little over £77 for LLE purposes – so let’s put our nominal 8 hour day at £61.60. It therefore may give providers pause to realise that the average income per learner day for CPD and CE courses was more than double that, at £175.60.

Here’s a chart of that at a provider level – I’ve shown revenue on the y axis and learner days on the x axis, with the cost per day in the tooltip.

Now I am not about to criticise government attempts to make shorter courses at providers more affordable for learners. And even though I don’t think the loan system on offer is the best one for the job, I think the idea of people being able to access support for training and professional development throughout their lives is an inarguably good idea.

But it is quite difficult to make ends meet running a higher education provider right now, and unilaterally offering many of them a fee income cut for something they are already doing well feels like a bit counterproductive. Indeed, if a flood of higher level courses from other providers, backed by government loans, enters this established market I really don’t see any way that providers can do anything other than accept a new, lower, floor price or cut their losses by stopping provision.

I should note here that credit hours are not all contact hours – but I’m making the assumption that independent study time has a cost in itself (learning resources, library study space…) and that there are non-contact hour costs (preparation, marking…) associated with a course. For this reason we should see this comparison as indicative of a wider cost disparity.

Is this planned?

Averages, of course, hide a huge variation. All kinds of providers charge less (again on average – averages of averages are not recommended) than our £61.60 floor – from the University of Manchester (£58) to the Central School of Ballet (£56), and from the University of Teesside (£50) to the University College of Estates Management (£30). But the majority – including many with existing substantial short course recruitment, are well above that.

The chances of providers being compensated for a loss of income here are pretty much nil. It may be that providers are overcharging (and perhaps that is the government calculation?), but it is equally possible that they are charging not much more than the cost of doing the courses well – or at least, a cost that the market will bear. Who remembers when the government liked the idea of a market based on fees?

And, as the HESA data collection guidance notes, quite a lot of this provision is actually paid for by employers. Would employers still be willing to do that if there is an LLE-supported variant of the same provision?

It’s not often that I find myself arguing against the government intervening in an education market place to benefit learners – but rather than seeing this as a planned market correction or price cap I am inclined to believe that we have yet more evidence that the LLE is not something that has been properly thought through.

Bonus content

The Higher Education Business and Community Interaction (HE-BCI) dataset underpins some serious regulatory activity. It is the basis for the Knowledge Exchange Framework (KEF), and is used in the calculator of Higher Education Innovation Fund (HEIF) allocations from Research England.

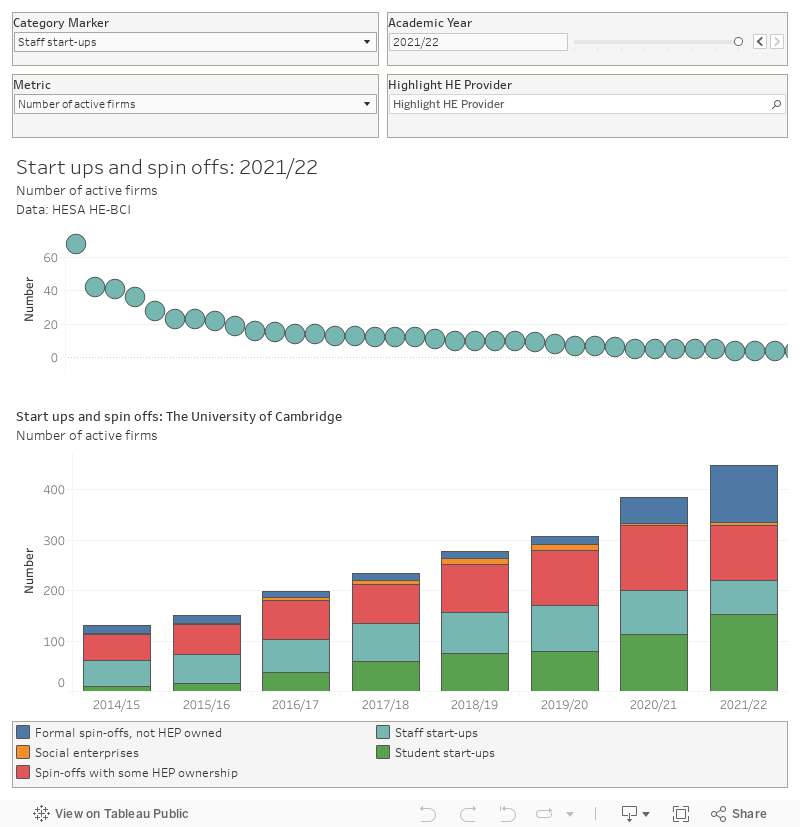

I’ve never been convinced by the data quality of HE-BCI, but there’s some interesting stuff to look at. Here, for example, is information on spin-offs and spin-outs (it appears that student start-ups are going great guns, so if you happen to be a venture capitalist do get stuck in):

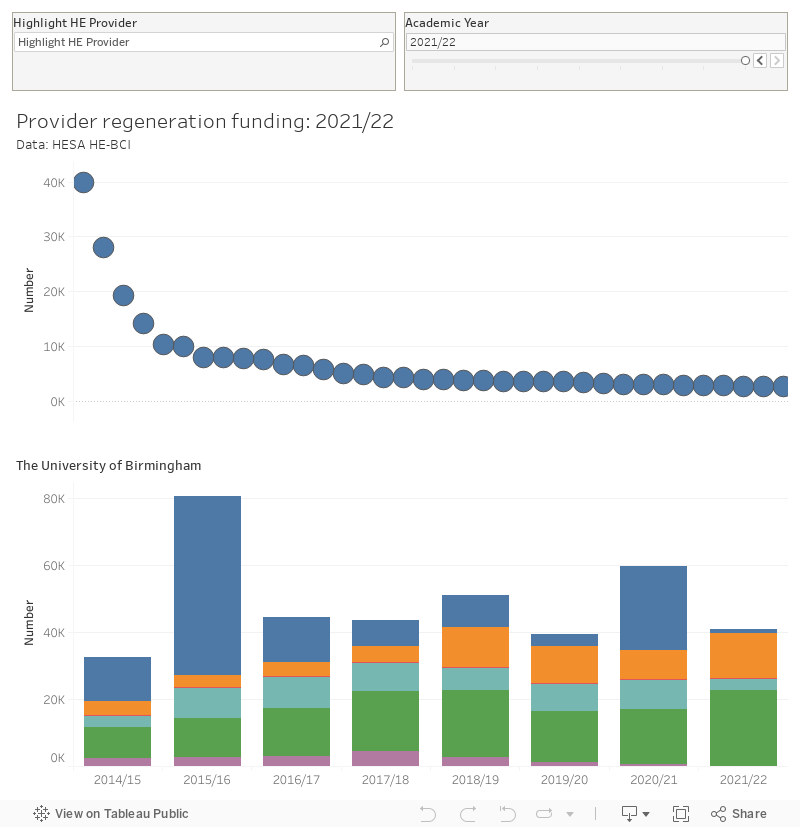

Providers do get some funding from government to do local regeneration and community work – here’s how that works out: