The 2020-21 financial year represents – depending on your perspective – either the height of pandemic-related restrictions in the UK, or the calm before the cost-of-living crisis.

So above all, what we are looking for in this year’s crop of provider-level data from HESA is evidence of stability and resilience.

Big, anchor-employer size entities like your local university should – in a rational world – be pretty much impermeable. Should a serious storm hit, there are numerous emergency devices – ranging from more gentle acts like drawing down more accessible reserves or pre-agreed overdrafts through to expensive new borrowing and rapid, painful, reconfiguration.

But there should never be any serious risk of the whole thing going under.

Key financial indicators

The revised guidance on reportable events during this period required that a provider notified OfS if it were forecast that they would have less than 30 days of liquidity (bluntly, if they could afford to run for less than a month on current cash in the absence of any new income). Though some smaller providers (and indeed smaller businesses) do usually choose to run with lower levels of liquidity and would have been exempt from this requirement, you can see quite a few places around that for the year. Thirty days is quite a low bar here.

We can also see that liquidity varies hugely across the sector, and is not stratified by provider size, shape, or history. If you buy into the conspiracy theory that DfE is happy to see parts of the sector die off, you’re going to have to assume it isn’t the parts a lay reader may expect.

I also keep an eye on staff costs as a percentage of total income for this reason – think of it as an indicator of the amount of income a provider can lose – or the amount it can increase cash expenditure – before it needs to cut into staff numbers.

You can examine the full range of KFIs (definitions) using the drop down at the top of each chart. Mouse over a provider on the top chart to see a time series at the bottom. You can filter the top chart by region and mission group (null in each case means it relates to providers I don’t usually deal with and thus don’t have the data for). The colours of the dots are Wonkhe’s custom groupings, detailed on the site last summer.

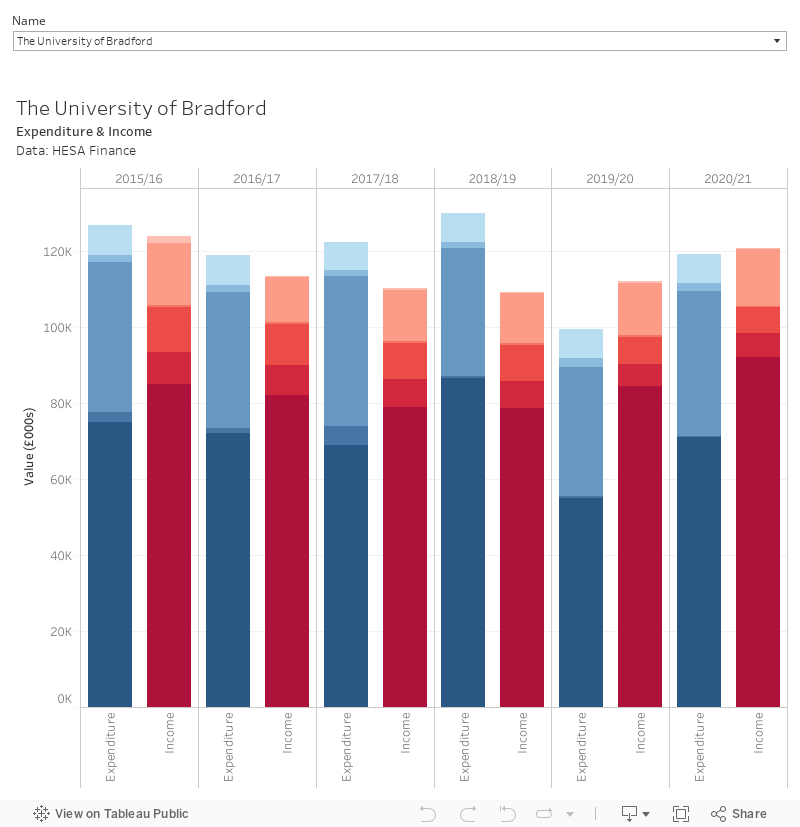

Income and expenditure

Universities are giant machines for turning money into higher education. They receive money from all kinds of places and then spend most of it (primarily on staff) to make teaching, research, outreach, and regulatory compliance happen. Here’s a quick overview of how that has panned out for your provider over the past few years.

From this, we start to look at surpluses and deficits. Here it makes sense to think on both an annual (was it a good year? Did you recruit well, or make savings, or cut outgoings, or see return on investments?) and multi-annual (did the good we did this year make up for the problems we’ve had in the past? Are recent emergencies mitigated by prudent decisions earlier on?) basis.

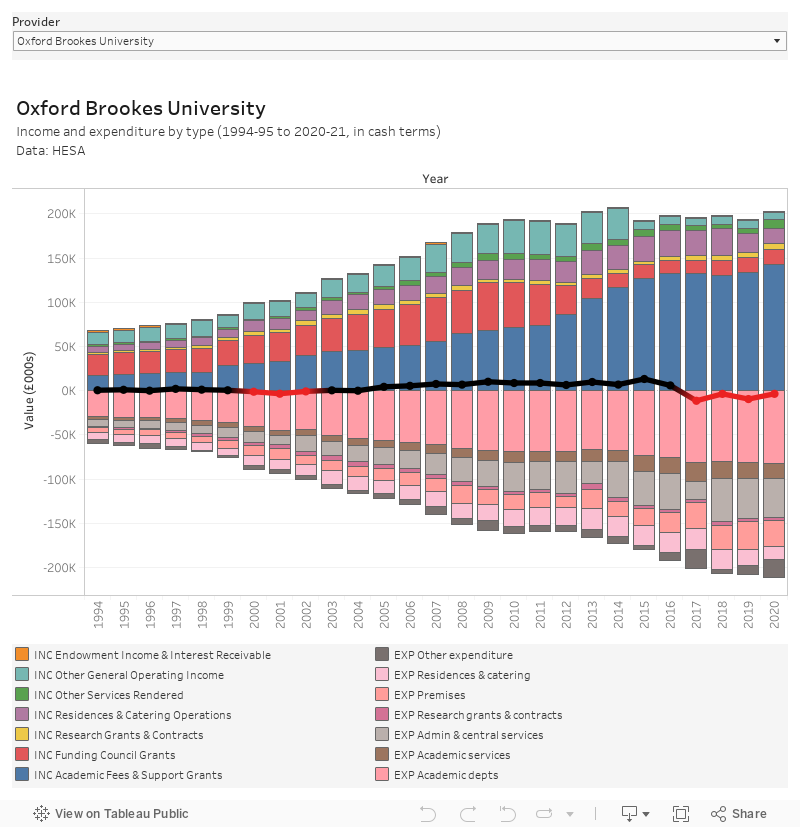

For the keen, I have a similar time series (not identical, it’s based on an old HESA publication called “UK HE Resources”) going right back to 1994. This covers most English providers – others will have at least four years of data in this format.

The limitation here is that we don’t easily get to see the real terms value when we make those comparisons. Inflation is always a factor, right now it is an essential one for anyone thinking about future stability to take. Stuff is about to get a load more expensive – indeed, it is already happening – and that means that any pound that you have now will be able to buy less come the autumn.

(Not) spending it

As hinted above, the main kind of stuff that universities buy is related to people – wages, pensions, on costs. Recent pay rounds suggest that employers want to cut wages in real terms rather than cut jobs – though either course points to renewed industrial action.

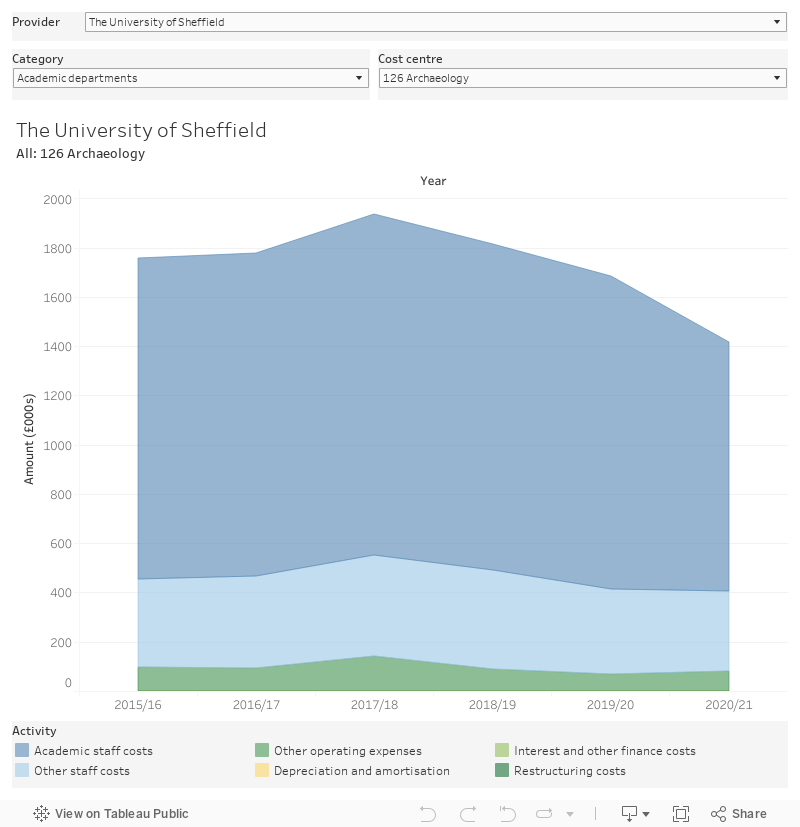

We get a lot more granular detail from HESA on expenditure than we do on income – the “cost centre” (something that almost-but-not-quite works as a proxy for department or school) is a unit of analysis that comes close to everyday experience.

Here again, we see staff costs dominate.

This is a simple chart but it is a powerful one. Select your provider at the top, the cost centre type on the left below, and the individual cost centre or summary on the right.

Even a sizable and painful cut to staff costs – at great detriment to students and the wider subject community – only yields a minor (less than proportional) cut to other operating expenses. Slashing the salary of your vice chancellor, as popular as that may be, is practically invisible on a university scale.

A hard few years ahead

Unless something politically unlikely happens, the short-to-medium term future of universities is as clear as it is bleak.

The real terms income of most universities will drop. Prices, and thus costs, will rise. Salaries will stagnate, and jobs will be lost. Corners will be cut, capacity will be lost.

The opportunities for growth will be in the high stakes worlds of contract research and international recruitment. The recent positive three-year settlement on QR funding will be the last bit of good news for most for quite some time.

There’s no money in home undergraduate student recruitment with the multi-year fee-freeze in place. We’ll see postgraduate courses become more important in institutional planning, but the market will be choppy and will favour those with already strong reputations.

And students will be suffering – with no support expected from government in England it will be up to universities to deal with students and researchers who cannot afford to live or eat.

Just a small addition to the end of your article:

“…and STAFF will be suffering – with no support expected from government in England it will be up to universities themselves to deal with staff who are unable to afford to live or eat.”

“Recent pay rounds suggest that employers want to cut wages in real terms rather than cut jobs”

One thing we’re finding in many bits of professional services – where of course an administrator or IT specialist or electrician can get broadly the same job on higher pay a mile down the road – is that it’s a case of both anyway: wages fall relative to the market, so while the job might still be there on paper, good luck getting someone to fill it. The inevitable industrial action is just a warning.

I would expect to see more Post-92s go down the “Staffordshire University Services” model to allow them to exit TPS.