Chancellors keep reaching for the same lever on student loans

Jim is an Associate Editor (SUs) at Wonkhe

Tags

Partly because we might get a little bit closer to understanding whether my hunch is right – that lots of decisions that have led to the current crisis have been driven by what goes on deep inside the Treasury and its modelling.

So let me explain what I think is going on.

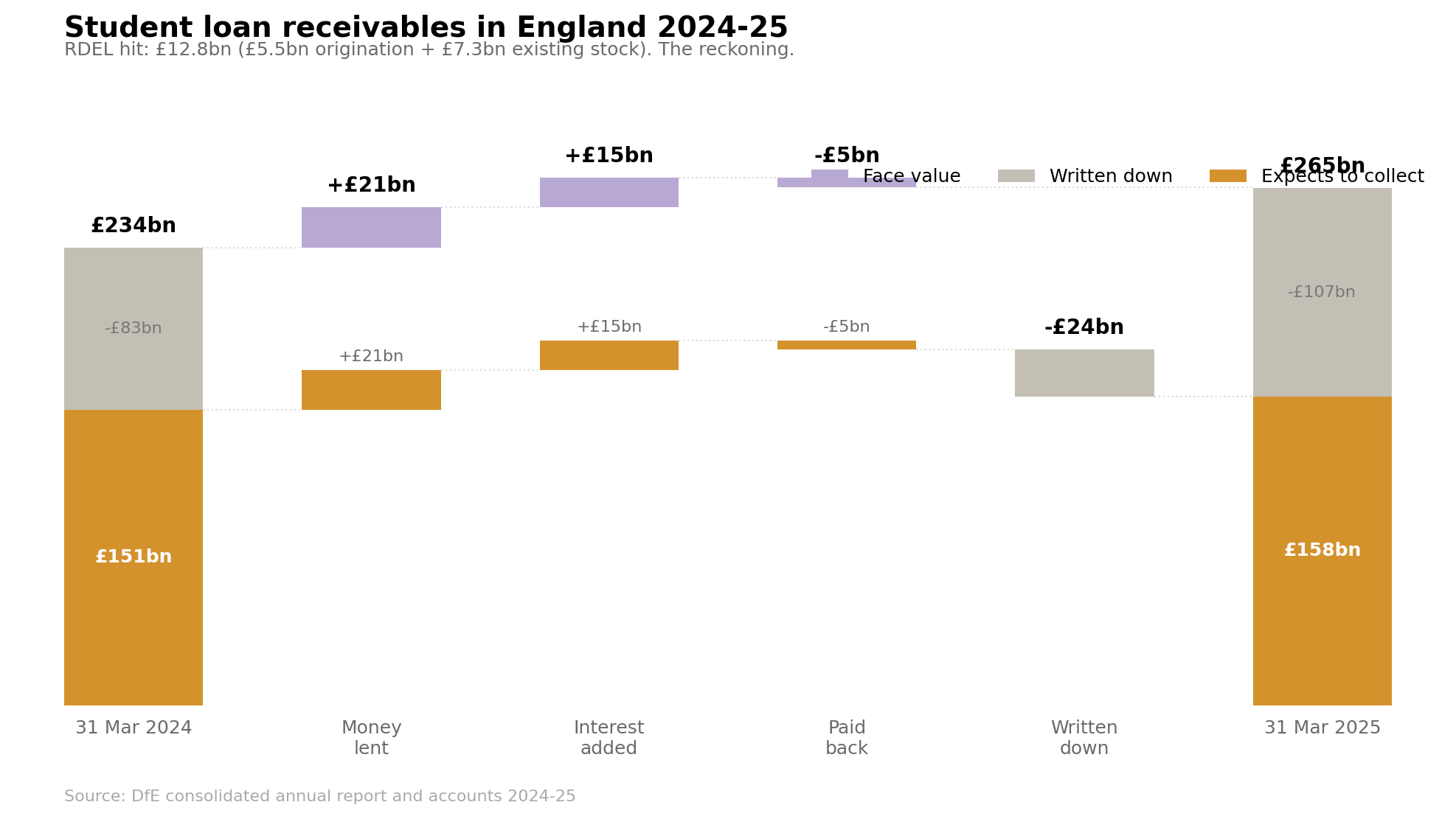

The government has “loaned” a lot of money to students over the years. By March 2025, graduates collectively owed £265 billion. That’s the number on their statements – the balance they’d see if they logged into their student loan account.

But when the Department for Education puts that same pile of loans on its own balance sheet, it values them at just £158 billion.

That’s a gap of £107 billion. The government is saying: we’re owed £265 billion, but we only expect to get £158 billion of it back.

That gap is supposed to be there. The whole point of income-contingent student loans is that they contain a subsidy. The government lends you money knowing you might not earn enough to pay it all back, and if you don’t, the remainder gets written off after 30 or 40 years. That’s the deal. It’s a feature, not a bug.

The problem isn’t that there’s a gap. The problem is that the gap keeps changing – sometimes by billions of pounds in a single year – because the government has to keep re-estimating how much it will eventually get back. And those estimates depend on what graduates will earn over the next three or four decades, which is hard to predict.

Every year the government runs a big computer model that tries to guess how much money graduates will earn over the next 30 or 40 years. If it thinks they’ll earn a lot, it expects to get most of the money back. If it thinks they’ll earn less, it expects to get less back – and the loans are worth less.

When the model decides loans are worth less than last year, the government has to write that loss down somewhere. And the place it writes it down is the same budget it uses for schools, teachers, and children’s services – the day-to-day spending budget. It’s as if someone added a bill to DfE’s tab, even though no actual money was spent. The model just changed its mind about the future, and that change in opinion shows up as billions of pounds of extra “spending.”

This happens in two ways. First, every time the government hands out new loans – about £20 billion a year – it immediately admits it won’t get about 30 percent of that back. That’s roughly £6 billion a year, every year, and it’s predictable.

But the second part is the problem. The government also has to re-check the entire existing pile of loans and ask – given what we now think about graduate earnings, inflation and so on, is this pile worth more or less than we thought last year? If the answer is “less,” the difference gets added to that same spending budget.

So let’s look at how that has played out.

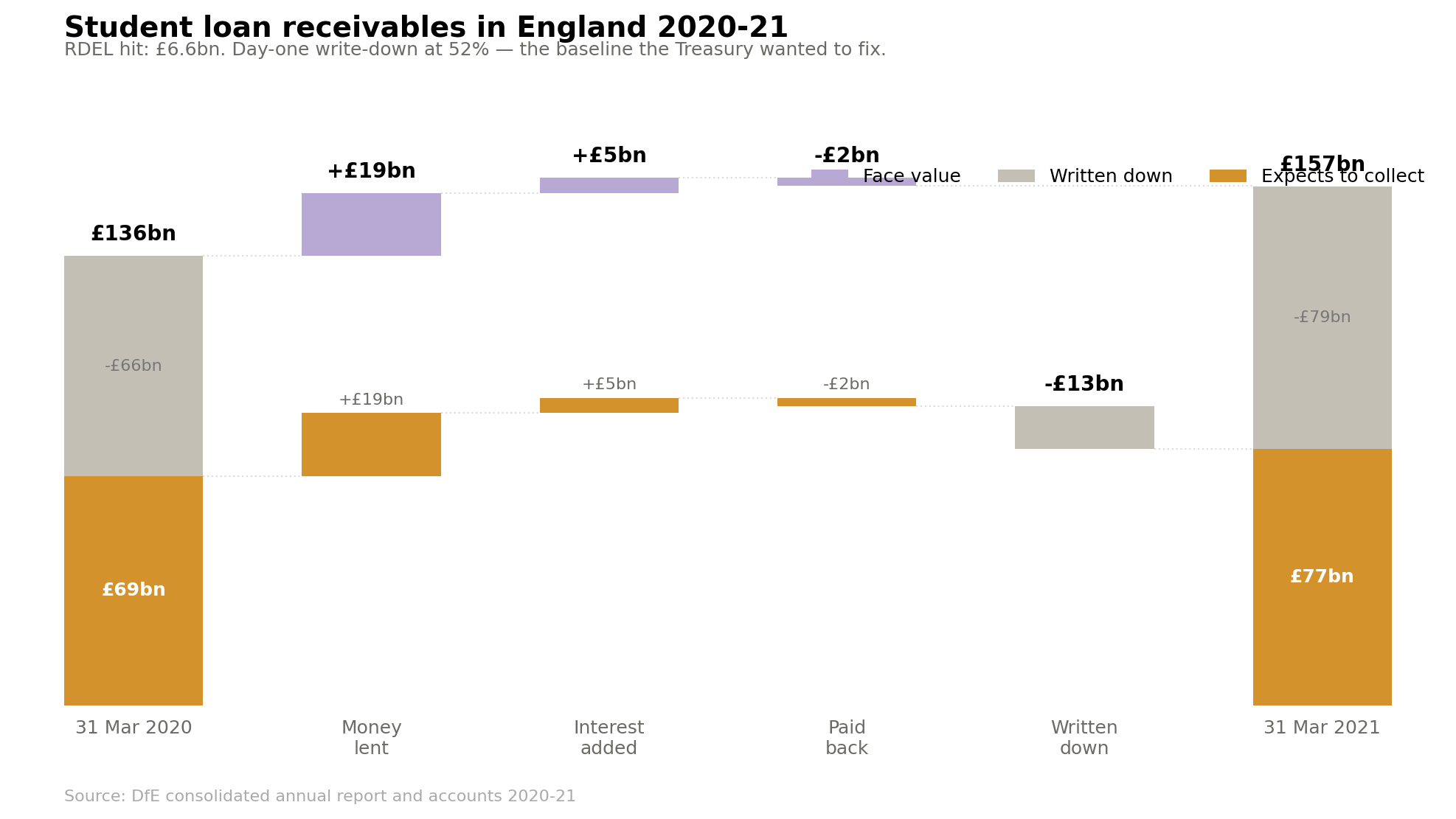

Year 1: 2020–21

The pile: £157 billion owed on paper. The government thinks it’s worth £77 billion.

What went out: £19 billion in new loans to students.

What came back: £2.5 billion in repayments from graduates.

The day-one write-down: Of the £19 billion lent, £9.8 billion was written off the moment the cheques were sent – a 52 per cent write-down. More than half the value of every new undergraduate loan was considered lost on day one.

What happened to the existing pile: Not much. The residual fair value movement – the line that captures changes in the earnings outlook – was -£410 million. A small deterioration, nothing dramatic.

The RDEL hit: Student loans cost the departmental day-to-day spending budget £6.6 billion. That’s money notionally taken from the same pot as schools, children’s services, and early years – even though it’s ringfenced and non-cash. It still counts against the fiscal rules.

The political context: This 52 per cent day-one write-down was likely the number that mattered. The Treasury may have looked at it and saw a system where the subsidy was bigger than they’d have liked. If you’re lending £19 billion and immediately admitting you’ll never see £10 billion of it back, something had to be done.

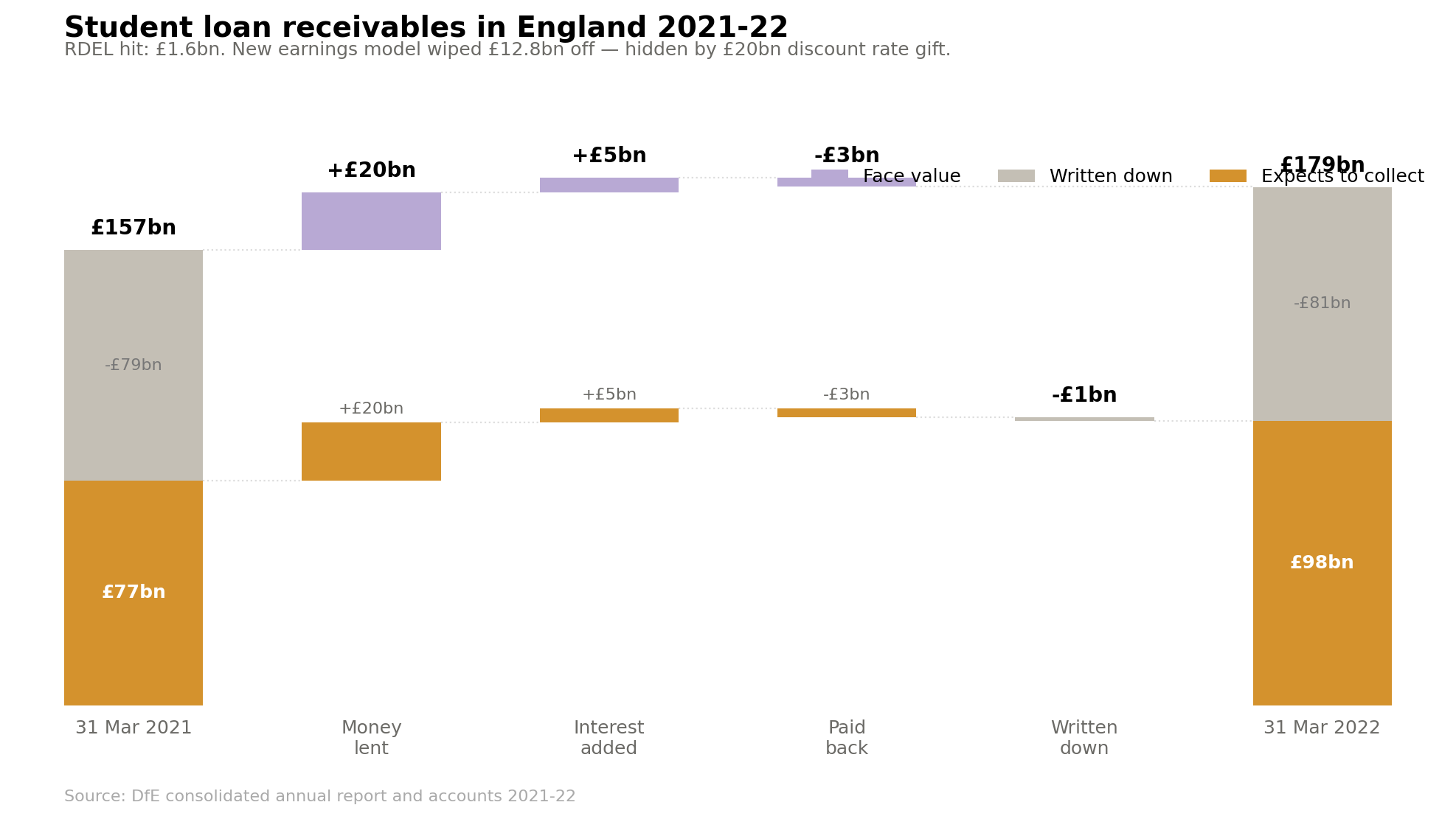

Year 2: 2021–22

The pile: Grows to £179 billion owed, valued at £98 billion.

What went out: £20 billion in new loans.

What came back: £3 billion in repayments.

The day-one write-down: £8.6 billion on £20 billion lent – 43 per cent. Already improving slightly, but still enormous.

The big event: DfE built a new, better model for predicting what graduates will earn over the next 30 years. The new model looked at the data and delivered bad news – graduates aren’t going to earn as much as the old model assumed. This single update wiped £12.8 billion off the value of the loan book.

But nobody noticed, because at the same time the Treasury changed the discount rate – the technical number used to value future payments in today’s terms. This had nothing to do with whether graduates would actually repay. It was a change to the accounting formula. And it added £19.8 billion to the carrying value.

So the bad news (graduates won’t earn enough) was completely hidden behind an accounting adjustment. The headline carrying value went up. The residual fair value movement – the pure earnings outlook – was -£6.3 billion. The model was screaming that something was wrong, but the headline figures said everything was fine.

The RDEL hit: Just £1.6 billion – a huge reduction from the year before. The discount rate gift made the spending figures look better too.

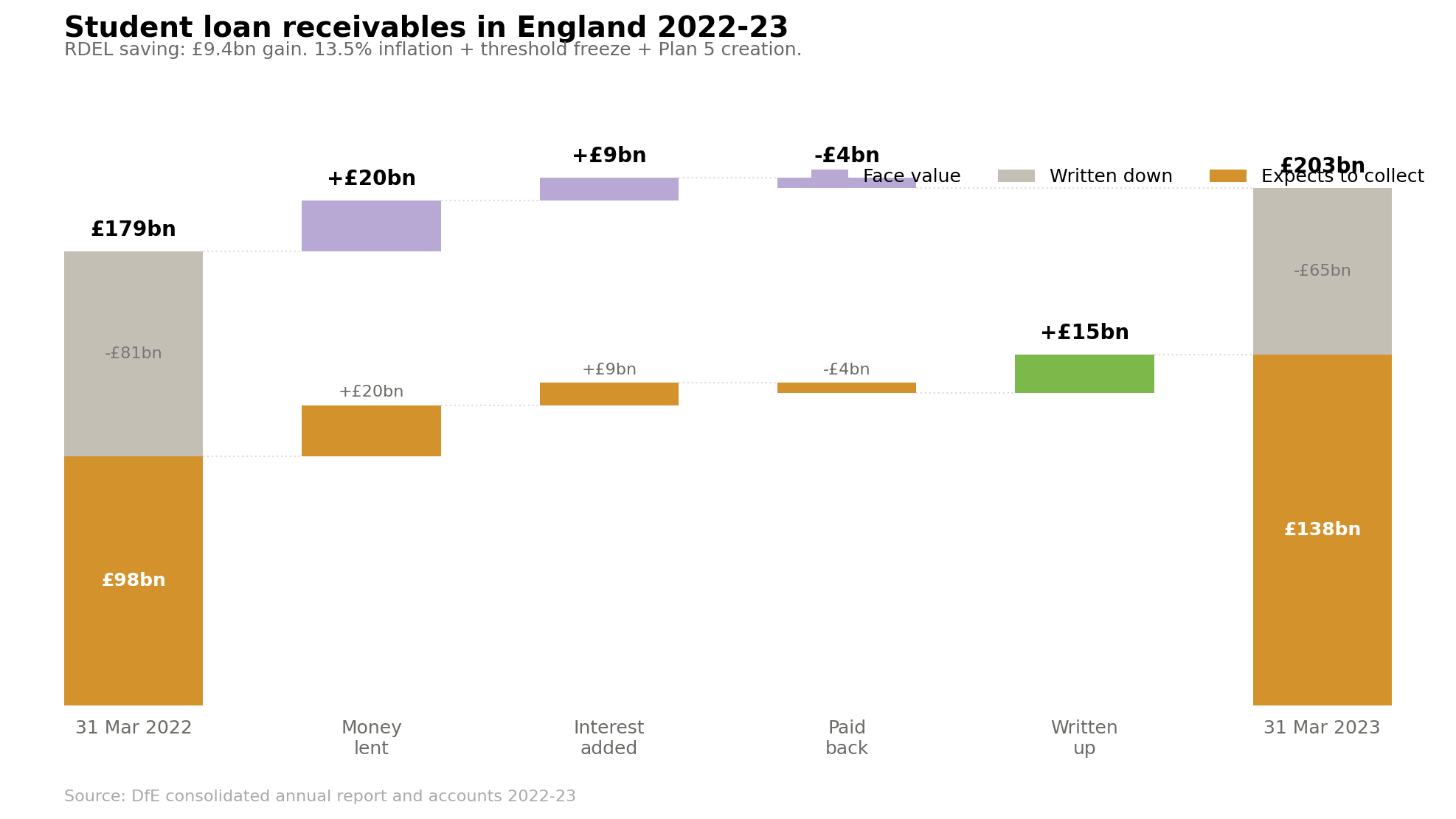

Year 3: 2022–23

The pile: £203 billion owed, now valued at £138 billion. The carrying value jumped by £40 billion in a single year. On paper, the loan book had never looked healthier.

What went out: £20 billion in new loans.

What came back: £4 billion in repayments.

The day-one write-down: £5.5 billion on £20 billion – 27%. Down from 52 per cent two years earlier. A dramatic improvement. But not because graduates started earning more.

What actually happened is two things at once.

First, inflation hit 13.5 per cent. This was terrible for the country but temporarily brilliant for the loan book’s accounting value. Because loans are valued using a formula linked to RPI, high inflation makes the “unwinding of the discount” – a purely mechanical effect of time passing – generate enormous gains. It hit £14.2 billion this year, compared to £6.6 billion the year before and £1.3 billion the year before that.

Second, and much more importantly for the long-term story, the government changed the loan terms. Rishi Sunak’s Treasury froze the Plan 2 repayment threshold – the salary at which graduates start repaying – instead of letting it rise with earnings.

And it created a brand new Plan 5 for students starting from September 2023, with a lower threshold (£25,000 instead of £27,295) and a longer repayment window (40 years instead of 30).

Both of these changes had the same effect – they squeezed more money out of graduates. With a frozen or lower threshold, you start repaying at a lower salary. With a 40-year term, you repay for a decade longer. The model immediately recognised this – the “impact of changes in assumptions and modelling” line showed a £22.4 billion gain, the vast majority of which was these policy changes flowing through to the existing Plan 2 stock.

The day-one write-down on new lending fell from 52 per cent to 27 per cent – not because the graduate labour market improved, but because the government redesigned the repayment terms to extract more from borrowers.

The RDEL hit: Not a hit – a £9.4 billion gain. Student loans actually reduced DfE’s apparent spending. The combination of high inflation and the threshold reforms meant the loan book was revalued upwards so sharply that it produced a negative RDEL charge. In a department spending roughly £90 billion a year on actual services, a £9.4 billion accounting gain was transformative for the headline fiscal position.

Why this was great for Sunak: At a time when the public finances were under pressure, the student loan RDEL line was handing the Treasury billions of apparent savings. The day-to-day spending numbers looked better, the borrowing numbers looked better, and the fiscal headroom looked better.

All because (a) inflation happened to be high, which nobody planned, and (b) the government made graduates repay more, which it very much did plan. Neither of these things meant the system was working better for students or for education. The subsidy was being reduced by squeezing borrowers, not by improving graduate outcomes.

Meanwhile, underneath all of this, the residual fair value movement – the pure earnings outlook – was -£6.7 billion. The model was still saying graduate earnings were getting worse. But the signal was completely drowned out by the inflation noise and the policy changes.

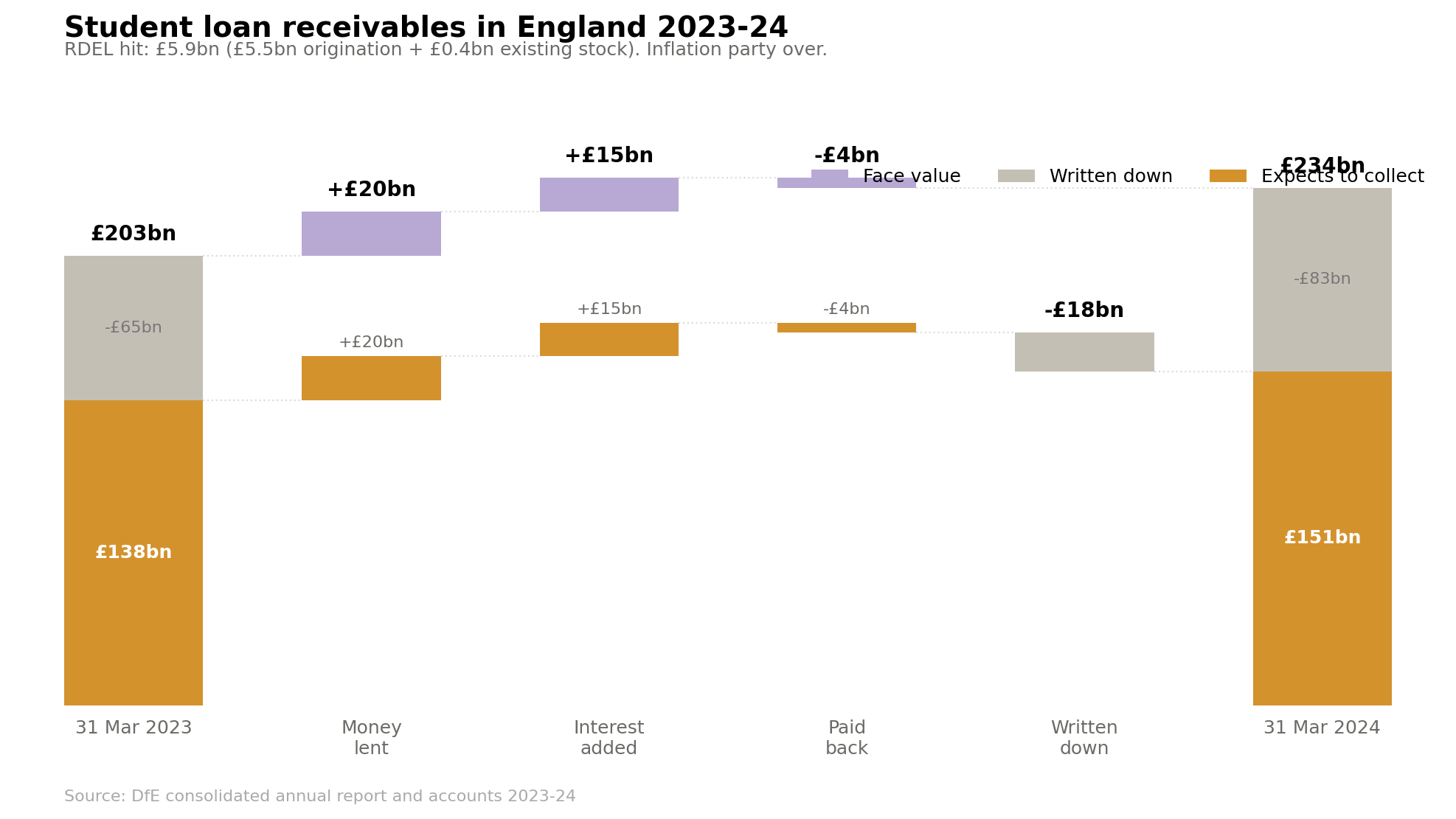

Year 4: 2023–24

The pile: £234 billion owed, valued at £151 billion.

What went out: £20 billion in new loans – now split between two plans. Plan 2 got £16 billion (for students already partway through courses), and Plan 5 got its first £3.7 billion.

What came back: £4.4 billion in repayments.

The day-one write-down: £5.8 billion on £20 billion – 29%. Plan 2 at 30 per cent, Plan 5 at 29 per cent. The new system was landing where the Treasury wanted it – a ~30% RAB charge, roughly half what it was three years earlier.

What happened: Inflation fell back to about 4 per cent. All the flattering effects disappeared. The unwinding of the discount dropped from £14.2 billion to £5.4 billion. The headline fair value movement swung from a £23.9 billion gain to a £2.5 billion loss – a £26 billion swing in one year.

The earnings outlook had a rare good year – the residual was +£846 million. But this was largely because the brand new Plan 5 loans showed a +£1.7 billion residual — the model hadn’t had time to be disappointed yet. Plan 2 was still deteriorating at -£1.3 billion.

The RDEL hit: £5.9 billion – back to being a cost. Of that, £5.5 billion was the steady, predictable day-one write-down on new lending. The remaining £0.4 billion was the annual revaluation of the existing stock – small this year because the earnings outlook was marginally positive.

This year also introduced much better disclosure. DfE published a full budgetary outturn breaking down the fair value movement by plan type and by budget category. You could finally see how the damage was distributed. The transparency improved — but the underlying story was becoming clear.

Year 5: 2024–25

The pile: £265 billion owed. Valued at £158 billion. The gap: £107 billion – 40 per cent of face value, the highest it’s ever been.

What went out: £21 billion in new loans. Plan 2 is now winding down (£10 billion – just students finishing courses), while Plan 5 takes over (£10 billion).

What came back: £4.8 billion in repayments.

The day-one write-down: £6.1 billion on £21 billion – 30 per cent. Steady. The government is giving away 30p of every £1 it lends, on day one. That’s the designed-in subsidy, and at this level the Treasury considers it acceptable.

The big story is the existing pile. The overall fair value movement was -£8.6 billion – the worst since 2020-21.

The residual fair value movement – the pure earnings outlook – hit -£6.7 billion. That’s a £7.5 billion swing from last year’s +£846 million. The accounts say it plainly – the residual “reflects changes in determinants such as the [graduate] earnings outlook, which is more pessimistic than in the prior year.”

The model looked at what graduates are going to earn over the next 30/40 years and concluded – it’s worse than we thought. Much worse. Plan 2 took the heaviest hit at -£6.5 billion. Plan 1 (pre-2012 graduates, now well into their careers) showed -£460 million — which is troubling because these are people the model should understand well by now. Plan 5 showed +£1.1 billion – still too early to disappoint.

The RDEL hit: £12.8 billion – the highest in the series. Of that, £5.5 billion was the steady day-one origination charge. The remaining £7.3 billion was the annual revaluation of the existing stock – almost entirely the earnings outlook getting worse. That’s a swing from £0.4 billion the year before to £7.3 billion. A £7 billion surprise, landing in the departmental spending budget, driven by a model re-estimating what graduates will earn between now and 2055.

Chancellors use the same trick

The pattern is now clear. When the measured cost of the student loan system gets too high for comfort, chancellors reach for the same lever – freeze or lower the repayment threshold.

This makes graduates repay earlier and for longer, which makes the model predict higher future repayments, which makes the loan book look more valuable, which reduces the RDEL charge and improves the fiscal position.

Sunak’s version was to freeze the Plan 2 threshold and create Plan 5 with a £25,000 threshold and 40-year term. Result – the day-one write-down fell from 52 per cent to 27 per cent. The RDEL line swung from a £6.6 billion cost to a £9.4 billion gain. The fiscal improvement was enormous – and it was achieved entirely by extracting more from graduates, not by improving the labour market or the quality of provision.

Reeves’s version, in November 2025, was to freeze the Plan 2 repayment and interest rate thresholds for three years from 2027-28. Same playbook. The OBR costed this as increasing cash repayments by £0.4 billion a year in the medium term and – critically – producing a one-off £5.6 billion reduction in borrowing in 2026-27.

That £5.6 billion comes from the increased value of the loan book flowing through as a capital transfer from households to government under ONS accounting rules. It’s scored in the year the legislation is enacted, not spread over the years when graduates actually pay more.

So in one year, 2026-27, the government gets a £5.6 billion windfall. Not from taxing anyone new, not from cutting spending, but from announcing that graduates will start repaying a bit more of their income in 2027-28, and booking the present-value benefit of that decision immediately.

This is the same accounting mechanism both chancellors have exploited. The loan book is so large – £265 billion and growing – that even small changes to the repayment terms produce enormous one-off fiscal effects. A threshold freeze that costs individual graduates a few hundred pounds a year across millions of borrowers translates into billions in the government’s fiscal position.

But the catch is that the threshold freezes don’t fix the underlying problem. They reduce the subsidy by squeezing graduates harder, not by improving what they earn. The residual fair value movement – the line that captures the earnings outlook – has been negative in four of the last five years.

Graduates aren’t earning what the Treasury needs them to earn, and freezing thresholds doesn’t change that. It just means graduates repay a larger share of their (still-disappointing) earnings. The system gets “cheaper” on paper while the graduate benefit gets worse.

The kernel of the row with Martin “miss-selling” Lewis is – should the government just suck it up when projections of graduate repayments fall? Or should it play with thresholds to recover? Neither is evil or wrong per se – but as it stands, it’s very hidden. Or was.

The OBR’s view forward

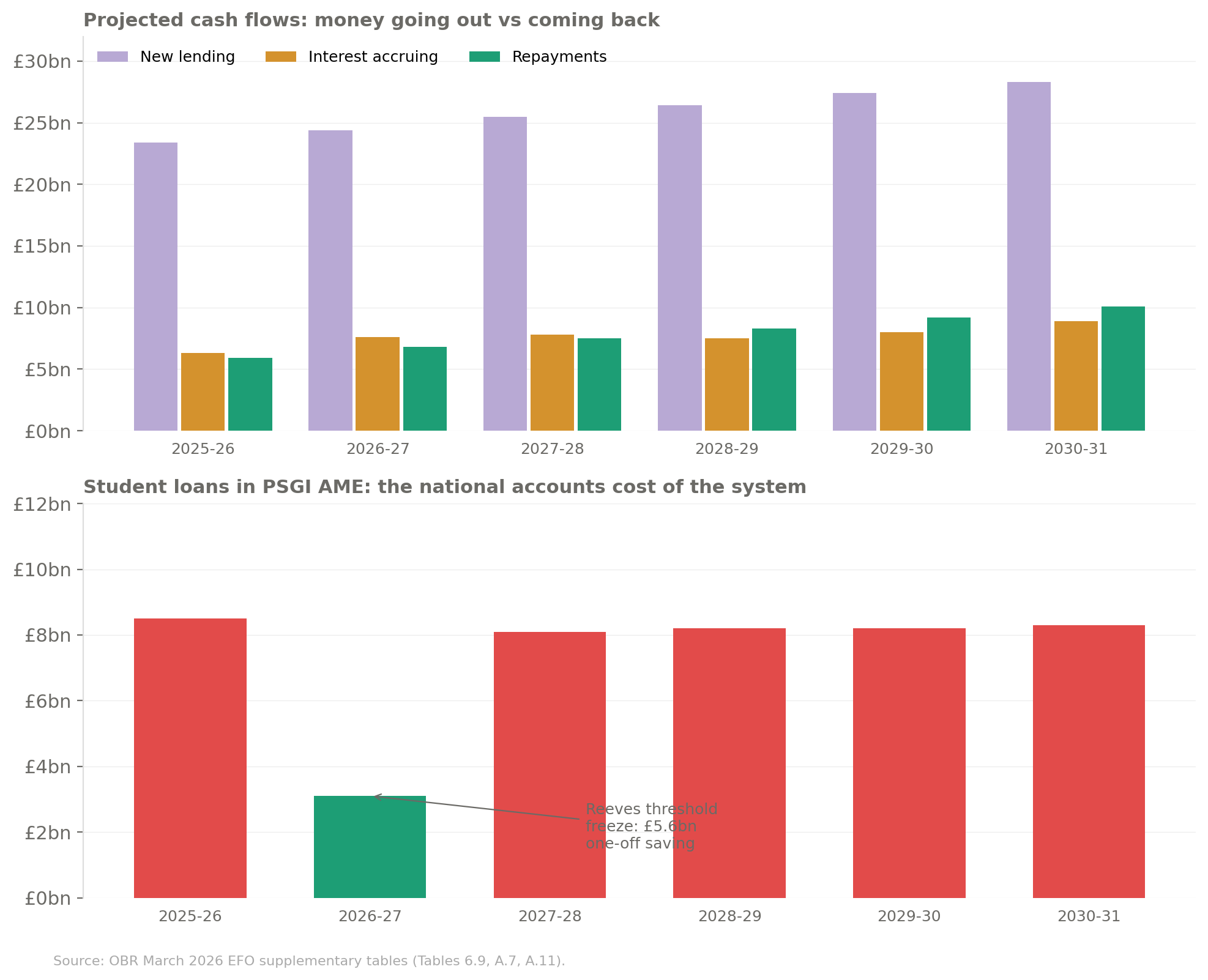

The OBR projects student loan cash flows in its March 2026 supplementary tables.

The 2026-27 dip in the PSGI AME line to £3.1 billion – down from £8-9 billion in every other year – is the Reeves threshold freeze showing up. The £5.6 billion one-off improvement lands in that year.

Lending keeps growing. Repayments grow too, but never come close to closing the gap. The steady-state national accounts cost runs at about £8-9 billion a year, as far as the eye can see.

What these projections can’t tell you is whether the annual revaluation of the existing stock will produce another multi-billion pound surprise. The OBR uses DfE’s model outputs – the same model that has been systematically too optimistic about graduate earnings, the same model that produced a £7.5 billion swing in a single year.

Nobody knows what the student loan book is really worth, because nobody knows what graduates will earn over the next 30 or 40 years. The government is adding £20 billion a year to an asset whose value depends on the answer.

Which brings us back to that Treasury Committee inquiry. The question is partly whether the system is too generous or too expensive. But it also comes down to this.

If graduates are earning less, one option is to take less of their money, because they need to keep it. The other option is to take more of their money, because the Treasury wants it. One option is to leave the terms alone for “loans” you’ve already made.

How would you score options a, b, and c?

One more thing

By the way. If the government can do it for its books, why not for borrowers?

Student loan statements could show two things side by side. The first would be the legal balance, because that is the formal amount outstanding under the loan rules. The second would be an estimate of what the graduate is now expected to repay over their lifetime, based on the same sort of modelling government already uses to value the loan book. That would give borrowers a far clearer picture of what their repayments actually mean in practice.

At the moment, many graduates log in, see a very large balance, see interest added, and feel as though their repayments are making no difference at all. For lots of borrowers, that is misleading. The system is income-contingent, and many will never clear the full face-value balance before write-off. What matters to them is not just whether the nominal balance is falling, but whether they are making progress through the amount they are realistically expected to repay. A second figure would help show that progress.

A better statement could therefore include the current legal balance, an estimated lifetime repayment under current assumptions, and the share of that estimated repayment already made. In plain English, it could say something like: you currently owe £X under the loan rules, but based on your current earnings path you are expected to repay around £Y in total over the life of the loan, of which you have already repaid £Z. That would be much easier to understand than the current single-balance approach.

This would not change the legal terms of the loan, and it would not replace the official balance. It would just present the system in a way that matches how it actually works for borrowers. The result would be a statement that feels more honest, shows a visible dent being made, and helps graduates understand the difference between the debt on paper and the amount they are likely in practice to repay.

Perhaps the graduates are earning less than forecast because the Govt is relying on models that mistakenly predict that if you raise the %HE participation then the added graduates will earn the same as the existing graduates are earning. Whereas in reality they earn far less because they are drawn from school leavers with ever lower Prior academic attainment ? i.e. The single biggest determinant of career pay outcomes is innate academic ability and not whether you have spent a further 3 years ‘in school’ . And now the reality is coming home to roost that sending ‘everybody’ to university is proving a colossal waste of time and money, and far more 18 years old should go to work instead of entering HE (and needlessly blighting their personal finances); and that the only beneficiaries are those drawing a salary by working in the bloated HE sector.

The only conclusion that this Inquiry should come to is that all student loans are a loathsome burden for any young adult to bear, no matter what the terms. And that society needs to dramatically re-order itself to avoid loading our youngsters with these life sapping loans as far as possible by 1 / Reducing the number that go to Uni to only where it is strictly necessary – which is probably 15-20% of population and save an absolute fortune on debt write offs & stop millions of young adults from doing a pointless degree and only having a debt to show for it 2 / Make it cheaper for remaining graduates with subsidised course fees, zero interest rates and means tested maintenance grants. 3/ Encourage employers to stop discriminating against non-graduates and start employing 18 year olds again by subsiding training costs and wages .

The introduction of Plan 5 *increased* the cost of student loans relative to reformed Plan 2. This is clear from the IFS analysis https://ifs.org.uk/publications/student-loans-reform-leap-unknown.

This is a very important point that the Treasury Committee need to grasp in their inquiry together with the distributional analysis of the Donelan reforms: every Plan 2 student pays a lot more, the lowest earning 60% of Plan 5 students pay a lot more, the highest earning 30% of post-2023 students enjoy a huge cut in effective tax. The impact of the current Chancellor’s repayment threshold freezes for Plan 2 students are a rounding error relative to the changes implemented by Michelle Donelan.

The remit of the Treasury Committee inquiry is also disappointingly narrow and fails to even ask what the objectives of the student finance system are in order to allow it to properly engage with the question about whether the government should focus finite public subsidy on insuring graduates against the risk of low lifetime earnings (Plan 2) or shift the balance to providing interest subsidies for high graduate earners (Plan 5)

Another really helpful and informative bit of analysis from Jim. What he illustrates is the fundamental, unavoidable problem that comes when the State lends money to large numbers of students, at levels where most of the borrowers will not be able to pay it back during an averagely successful working life. Over time, that has turned the loan book into an increasingly significant, but also increasingly unstable asset for the State. For all the reasons Jim gives, it is inevitable that Treasury will take a keen interest in what is happening to a £265 bn entry in the national accounts, and will respond if the “real” value of that £265 bn has decreased by more than had been assumed. That’s Treasury’s job. It’s also inevitable that fairly small changes in graduate labour market predictions will produce billions of pounds of changes in the projected value of the loan book, because the loan book is now so huge that even a 1% alteration in assumptions is significant.

One can argue about whether a particular Treasury response has been fair, or unfair, to particular groups of graduates. But always remember that we got here because of the 2010 decision (implemented from 2012) to fund higher education primarily through loans rather than grants (and thereby show savings in the national accounts, while giving universities more money). That was what moved the loan book from a significant, but reasonably predictable asset, into something much bigger and much more volatile. If the fee loan were still at a level where most graduates will repay it, then for most of them it might indeed feel like a “graduate contribution”, unwelcome but understood, rather than the ever-increasing, unending burden that some are now experiencing.

To illustrate, in 2011/12, the maximum fee loan was £3,375 and the maximum maintenance loan (for low income students living away from home in London) was £6,928; out of London it was £4,950. Most students would have emerged with a debt of £25-£30,000. On the government side, in March 2012 the face value of the loan book was £39.5 bn, and its estimated “real” value was £28bn (according to the BIS annual report). Over £4bn a year was going out in loans and around £1.5bn was being repaid. All of that is definitely serious money, for both students and government, but seen over a working life it feels relatively manageable and reasonably predictable – certainly in comparison with the numbers Jim is describing above.

Of course the 2010 decision was also taken in order to underpin a demand-led system. Treasury wanted to cut the grant funding that helped meet institutions’ teaching costs, but it was prepared to offer higher fee loan funding, and give this to any student who was accepted onto a course. It would be interesting to know if Treasury now regrets that decision. It did get its grant reductions. In 2010/11, the Higher Education Funding Council for England got £5.7 bn funding for distributing to institutions, who were teaching 1.2 million full time UK students. That compares to £1.4 bn that OfS got last year (when there were 1.7 million students). What is more, the government paid out £1.5 bn in student grants in 2010/11, and that was virtually all switched into loans. In all, nearly £6 bn grant savings. However, set that alongside Jim’s perfectly reasonable estimate that the steady-state annual cost of the current loan system to the national accounts seems to run at £8bn-£9bn, and it isn’t obvious how much money is in fact being saved in the long run.

What is more, the funding changes have not only made the loan book balloon in size, but are themselves affecting its value. The decision to lend more money than most graduates would ever repay was the first momentous decision of 2010. The decision to set a fee loan at a level much higher than the actual costs of teaching a classroom-based HE subject like Business Studies was the second (and it was a necessary decision if the teaching grant was to be cut by as much as desired). This has encouraged unbridled competition for however many students can be attracted; has incentivised every institution to maximise its number of students in the cheapest subjects; and has attracted new providers to enter the market because they can make decent profits from teaching these subjects. It is to that decision that one can trace the growth in franchise provision on which Jim has regularly commented. And if the graduates from such provision do indeed have lower than average employment prospects, then of course the value of the student loan book will reduce further, and its overall costs will rise still more.

The 2012 funding system has now had quite a few years of operation. Like any funding system, it drives behaviours. It drives Treasury to obsess ever more about graduate salaries and graduate employment, and fiddle ever more with repayment terms, to reduce its losses on an ever-increasing loan book . It drives all institutions to recruit as many students as they possibly can. It makes it possible to teach low cost subjects at a profit, thereby driving increases in low-cost subjects and for-profit institutions. It has also delivered growth in student numbers and greater competition between a greater number of institutions, both of which its creators wanted. In that sense the policy has “worked”, and of course there are drawbacks to every funding model. Nevertheless, it is worth remembering that different ones are perfectly possible and that some have been tried and tested previously. If the outcomes of the present model are really thought unacceptable, there are alternatives.