What if austerity really was over?

Jim is an Associate Editor (SUs) at Wonkhe

Tags

The old system – which on second reading Blair only won by 5 votes – had seen fees capped at £3,000.

The repayment threshold (£15,000 in 2006/7, rising by inflation) and the write-off period (25 years) mean that by 2011/12, the BIS (universities were in the Business department at the time) estimate of the subsidy going in was 33 per cent.

In other words, on average fees were really £2,000 even if the sticker price had settled up at £3,000.

So when the estimate was that on average, fees would be £7,500, and the assumed RAB charge was modelled at 28 per cent, we could have taken to the streets with a message proclaiming that “average fees” would rise from £2,000 to £5,400.

In our defence, we suspected that the RAB charge might end up being nudged down because it was clear that the repayment threshold might end up frozen – as I noted on here last week, it took a lot of effort to find Labour MPs to argue for a commitment to uprating it all, generating a new RAB estimate of 32 per cent by June 2011 (a commitment that the Tories then attempted to renege on later in the decade).

We also assumed that the idea of price competition emerging was fanciful – it hadn’t happened with £3,000 max fees and was never going to happen with £9,000 max fees.

But anyway, it’s the sticker price that people see, “tripling tuition fees” was a snappier slogan and it wasn’t up to us to explain the astonishing complexities about to be built into student loans.

Blame austerity

Over the past few weeks coalition partners Vince Cable, David Willetts and special advisor Nick Hillman have all justified the 9k regime in the context of austerity:

The first thing you have to remember is the politics of the time. So it was just after the 2010 general election and every big political party in the 2010 election had promised big cuts because it was just after the big financial crash… higher education was in the business department and so the business department was in line for really big cuts.

Remember the key driver here was the austerity cuts that the Treasury insisted we did and which we believe the electorate had voted for in 2010.

In the Commons debate on 9 December 2010 (the vote on the fee cap regulations), ministers generally framed the reforms as part of deficit reduction – Vince Cable described the package as a policy “that tackles the fiscal deficit”.

At the time, John Denham argued as follows:

Every year they will borrow £10 billion to fund student loans, and every year they will write off £3 billion… [this could]… cost the taxpayer more.

The same debate also included an argument that the required borrowing “will actually outstrip any gain that might have been made”, citing rising borrowing figures and saying this would make “the deficit worse” in the consolidation period.

It turned out that George Osborne was recognising the whole of what was loaned out as an asset, without estimating the eventual write-offs in the government books – hence grants were abolished for more generous maintenance loans, and the cap came off places.

But in terms of the central fiscal mechanism within the coalition’s austerity programme, the OBR’s November 2010 Economic and fiscal outlook explicitly estimated that replacing teaching grant with higher fees would allow the BIS resource DEL to be reduced by around £2.9 billion per year by 2014–15.

So in austerity accounting terms:

- BIS resource DEL cut: about £2.9 billion per year

- Offset by: about £5.6 billion per year additional lending (not scored as deficit spending at the time)

- £5.6 billion × 0.28 RAB = £1.568 billion

- Total savings: £1.332 billion

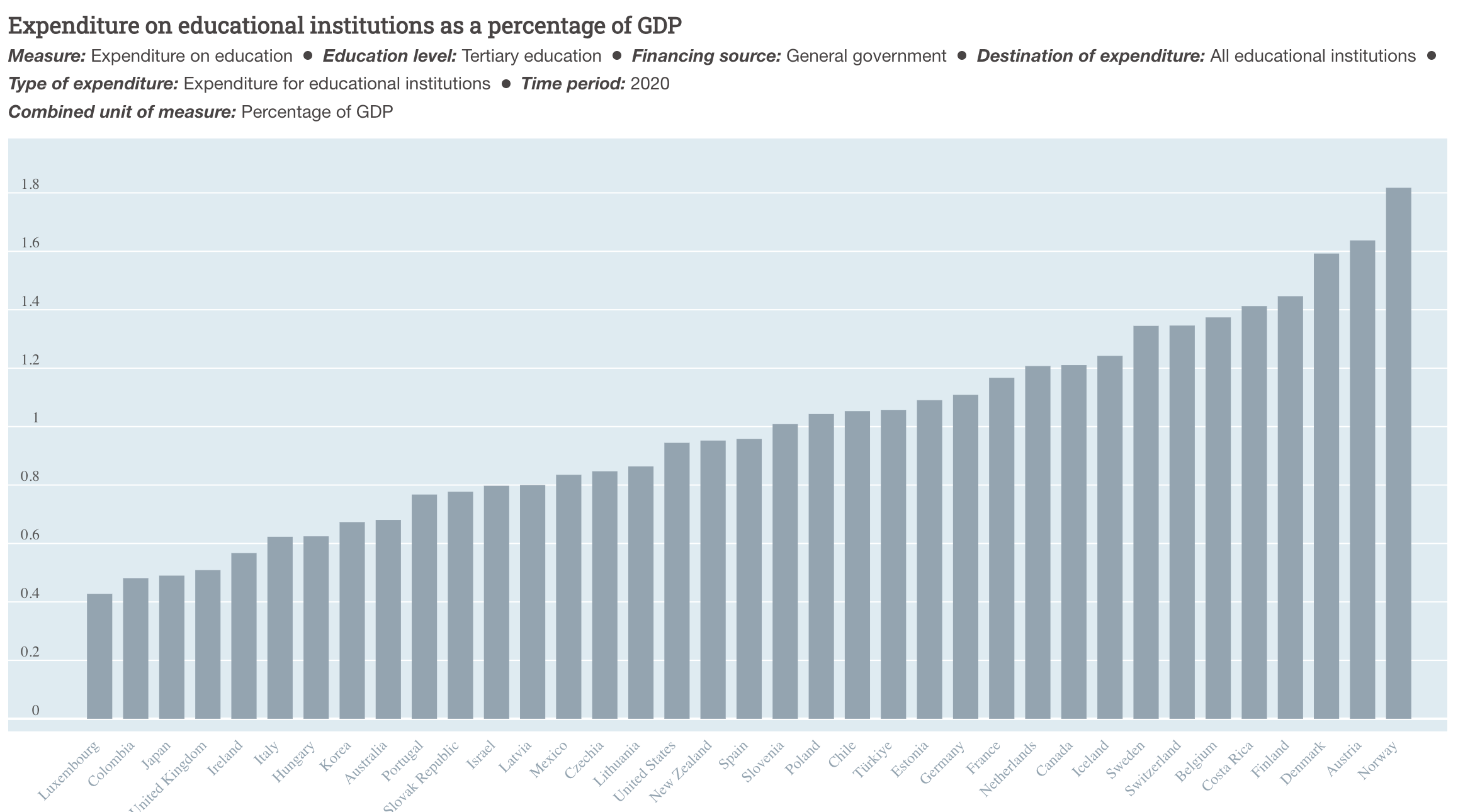

One of the upshots is embarrassing graphs like this:

The age of austerity is over

Much has been written (including by me) Theresa May Conservative Party Conference speech on 3 October 2018, when she defied the Treasury and raised the by then frozen repayment threshold to £25,000.

The line less often quoted:

The change did come with a cost. In the Autumn Budget 2017 costings table (which uses OBR-certified scorecard numbers), the “Student loans repayment threshold” measure (raising Plan 2 repayment threshold to £25,000 from 2018–19 and indexing with average earnings) is shown as a net cost to the Exchequer, rising over the forecast period.

The table shows £0 in 2017–18, then -£125 million in 2018–19, -£235 million in 2019–20, -£370 million in 2020–21, -£490 million in 2021–22, and -£615 million in 2022–23 (negative figures are costs, meaning higher Public Sector Net Borrowing than otherwise).

The OBR also flagged that the main fiscal effects of the threshold increase would occur much later, because higher thresholds reduce repayments and therefore increase the value of loan write-offs when balances are cancelled at the end of the repayment term. In its Autumn Budget 2017 policy measures annex, it notes that the “largest effects on borrowing” from the threshold change would occur around the point of write-off, roughly thirty years after the loans are issued on the new terms.

Attacking May’s statement, Jeremy Corbyn and multiple Labour MPs used the wording in debates to argue that the “claim” did not match local government and public service realities.

Either way, Rishi Sunak (with Michelle Donelan fronting it out) reversed the measure – freezing the Plan 2 threshold and setting Plan 5 down at £25,000. Previously, Sunak used particular wording as Chancellor in October 2021, in a formulation that was widely reported as “Austerity is over, but not undone”.

In government, Labour’s consistent formulation has been “no return to austerity” – Rachel Reeves used the “no return to austerity” line during the 2024 election period, repeated it in her Labour conference speech on 23 September 2024, and then put it into formal fiscal statements as Chancellor (for example the Autumn Budget speech on 30 October 2024, and the Budget speech on 26 November 2025).

But as I noted here, funding for students and universities has got worse, not better. Austerity never ended in HE. It got worse.

What if it really was over?

Ignore the “per head” calc for a moment. If we uprate that earlier £1.332 billion by RPI-X, it’s about £2.06 billion.

Today, the OfS recurrent grant is around £1.3bn, and the estimated transfer element of student loan outlay (ie the bit that won’t be paid back) is around £7.7bn – a total of approx £9bn.

The problem with constant calls to “develop alternatives” from the system’s architects is that it’s nigh-on impossible to do unless we have a sense of the available envelope.

That the envelope has been getting smaller is much of the problem. So even if we expected all of the costs of expansion to be met by graduates, returning to pre-austerity by finding that £2.06 billion would make identifying options a lot more straightforward to do.

The government planned to absorb student debt by raising thresholds, but economic growth was not sustained after 2007, so the debt rose as a proportion of the government debt and the long-term earnings growth of students did not materialise either. Annual GDP growth rate since 2009 is half what it was 1993-2007. The Foreign Secretary announced yesterday that the peace dividend is over. If the defence budget rose to 3.5% by 2035 with an annual 5% compound rate of inflation it would cost near to £60 billion. The Prime Minister has announced today that we need to reach the 2035 target much sooner. You have written about the modelling assumptions here:

https://wonkhe.com/blogs/the-walls-are-closing-in-on-our-doomed-student-loan-system/

If I were preparing an economy for a 75% increase in defence expenditure in less than 5 years, I would want to constrain other fiscal liabilities and be more cautious in my planning assumptions. The government is very unlikely to raise more debt and will instead sustain taxes at the current historically high level into the next parliament and cut keeping budgets in real terms. So there is no more money for student loans.

There are some missing numbers in this interesting article which relate to the February 2022 reforms announced by Michele Donelan when she was Higher Education Minister (coincidentally on the day that Russia invaded Ukraine).

In the March 2022 spring statement and OBR economic forecast, we found out that the freezing of the fee cap and repayment threshold plus the interest rate reductions and 40 year write off for Plan 5 would, as a package, reduce Public Sector Net Debt (PSND) by a total of £3.7 billion by 2026-7 and Public Sector Net Borrowing (PSNB) by a total of £37 billion for the same six year period. OBR explained the numbers on page 207 of their March 2022 forecast and comment that the big reduction in PSNB is because of the “upfront accrual of substantial effects on distant cashflows”. In other words, students starting after 2023 would still be making repayments in the 2060s and this, in turn, made increased the value of student loans in the national accounts

Unlike between 2010 and 2012, the decision makers in government in spring 2022 (PM Johnson, CEx Sunak, CST Clarke) didn’t reallocate these savings to HE grants or other parts of the education budget but, instead, used the money to reduce national insurance and to provide support for energy bills. The numbers are on pages 12 and pages 27-29 of the HMT March 2022 spring statement. In his speech, Rishi Sunak didn’t use the word austerity once but made a pitch that the government could lower personal taxes and reduce the national debt while also providing security