Fundamental to this question is an understanding of what kind of market we are dealing with. Since 2004 the higher education market has been designed to allow for competition on price – partially to drive efficiency, partly to drive competition.

Price has actually achieved none of these things – it barely even achieved variability. But the maximum fees have become a totemic indicator of the supposed rapaciousness of universities – even though the government’s own (Augar) review had to remove the standard margin for sustainability and investment (MSI) to get any indication of a profit being made.

And whatever the complexities of the funding model, or the way that the government actually does subsidise the sector to the tune of around half all outstanding fees, the meme that students pay £9,000 (actually £9,250) a year for their studies is a pervasive one that has been encouraged by ministers. It’s a sticker price, but given that it is also a maximum price (that happens to be the default price), it does odd things to a very odd market.

There is almost no competition on price in English higher education. Competition instead relies on various notions of quality (the hard registration baseline measures, the vagaries of the TEF, and the rest of the data in league tables and Discover Uni) and reputation at a provider or subject level. Reducing the maximum fee – in most cases, the actual fee – harms provider income and thus the actual quality of the student experience, and recent changes to high-cost subjects (sorry, “strategic funding”) and London weighting will mean this would have a profound impact for some providers and subjects.

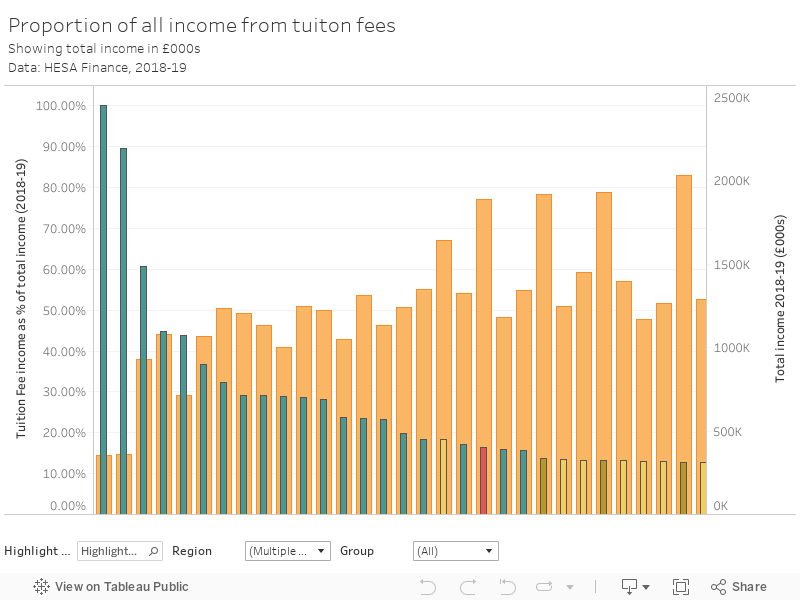

Some providers in England do rely on tuition fee income as their major source of income – here, the percentage of all income that comes from tuition fees is shown in orange, the other bars and axis show the total income of the provider.

Providers will need to make up any fee income deficit in order to continue to offer the same quality of student experience. And I suspect we will see the return of one unexpected old debate.

Top of the pops

Much of the debate about university finance back in the 1980s and 1990s focused on the idea of “top up fees”.

At that time, the government was under pressure both to provide additional funding for student maintenance (so-called “top up loans”) and to increase the “unit of resource” (funding per student) for universities. In ruling out the latter, there was a suggestion – though never quite a policy, not even 1980s Conservative backbenchers would wear it – that movement on the former (loans of up to £420 were available from 1989) would allow universities to charge students directly for parts of their tuition.

There’s a wonderfully telling quote in an old edition of The Times (12 October 1988) – an unnamed “senior official” from the Department of Education and Science is reported as saying:

We realise that there might be a need to provide some kind of incentive for the scheme to get off the ground, but the logic of the idea is inescapable. If a university has 10,000 students and charges each an extra £500 – the price of a second-rate skiing trip – it can raise an extra £5m a year. This could be used to finance extra students above the number the University Grants Committee agree to pay for.

Then, as now, there was known to be a list of between ten and twenty higher education providers that were in serious financial trouble – the increasing cost of teaching students coupled with the decreasing amounts available (within fee allocations for full-time undergraduate students and the block grant for other modes) to do so had seen financial crises at providers like Cardiff, Aberdeen, and UCL. More would likely follow. In real terms, government spending per student had fallen by more than 40 per cent between 1976 and the publication of the Dearing Report in 1997.

Dearing reaffirmed the principle that the state should remain the primary funder of university education- citing the benefits to the UK economy and society (the social rate of return). However, there was also a suggestion that graduates should contribute more to the cost of their education in future – recommending an income-contingent system of loans for maintenance costs (replacing the mortgage-backed loans available alongside grants at the time) and favouring the exploration of a graduate contribution to the costs of tuition on similar terms.

Where we are

Although the Dearing principle that the state should remain the primary funder of undergraduate education has since been lost the state is still an important source of funding, particularly for students in high-cost subjects who would be expected to work in careers with low average earnings. Dearing’s suggestion of a move to more funding directly following student choices has also had a lasting impact.

Indeed, the only new aspect to this old argument that has emerged since Dearing is the idea of variable fees as a mechanism for competition. Both the £3,000 fee cap introduced in 2003 and the £9,000 cap proposed in 2010 were set as a maximum rather than a standard rate – the idea being that providers could compete on price as well as on quality, with the former providing signals about the latter.

Although markets are simple, time-honoured ways to drive efficiency in the distribution and exchange of goods, finances, and services – the market for higher education did not work like this. Other measures, concerned with ensuring quality and standards did not slip, proved more important.

How choice currently works

In England in 2021 a person seeking entry to a course of higher education would usually use a service called UCAS to identify a suitable course at a suitable provider. For a provider to feature their courses on UCAS, it must be either registered with a regulator called the Office for Students (OfS), or deliver a course validated by a provider that is. Registration with the OfS requires that a certain minimum quality of provision is offered, either directly or via a validated partner. The OfS establishes this minimum standard via the collection of data and provider statements, and via more intensive research conducted by a specialised agency with a function set out in primary legislation – the current holder of this function is called the QAA. The OfS, UCAS, and the QAA are all funded via provider subscriptions.

The OfS also has powers to regulate the relationship between applicant and provider, stipulating a preferred set of terms for an “offer” of a place. These “offers” are generally made based on performance in nationally offered qualifications awarded after a provisional offer based on predicted performance is made. These qualifications are offered by a number of independent exam boards, with overall assurance offered by the JCQ – which publishes qualification awarding details and shares data with UCAS which can then share with providers.

Meanwhile, an applicant must approach another agency (the Student Loans Company) to seek funding both to pay course fees at levels initially set by the Secretary of State as a series of maximum levels (which in practice become the default prices), which are then assigned to various providers based on registration status by the OfS. The SLC may only fund students at a given level with respect to certain courses offered by providers registered by the OfS. These fees are transferred to providers based on the continued assurance that the student is participating in the course. An applicant may also apply for funding for their living costs – maintenance – which is available based on the type, of course, they have applied to, the geographic location of the provider, and the income of their parents or guardian.

Both fee and maintenance funding is made available as time-limited, income-contingent loans. This is a rare form of financial instrument in which an applicant takes on debt in the hope their future salary will grow to the extent that repayments will not exceed the salary benefit that a HE qualification confers. The graduate contribution begins when earnings reach a defined threshold and continue at an income- and RPI- linked variable rate of interest until 30 years have passed or the loan principal value plus accumulated interest is cleared, whichever comes first. The Treasury is deemed to have paid for any portion of the original loan that is not recovered for any individual graduate – this model subsidises the education of graduates who earn less earlier in their careers, but there is also a regressive feature in that graduates who repay early will pay less overall as they would avoid interest.

The value of the fee loans is transferred to the provider by the SLC in termly instalments. This covers the majority of the costs incurred in educating the applicant in question – but some courses, providers, and applicants attract additional funding, which is distributed directly by the OfS and does not need to be repaid by graduates. Some providers use fee or other income to cross-subsidise other activities, such as research.

The Department for Education sets the parameters of loans available from the SLC, the repayment rates of graduates, and offers guidance to the OfS in the distribution of other funding and on the requirements of registration.

Students and graduates unhappy with their course or provider have recourse to a dedicated Ombuds function, the Office for the Independent Adjudicator for HE (OIA). The OIA deals with student complaints after these have passed through provider processes – and has the power to recommend (not mandate) financial and other compensation.

It’s not actually straightforward

Set out in full, like that, it can be difficult to spot the market. Who is the customer, who is the vendor, and how is the money moving?

To draw some parallels – if I was to buy a car, I might choose to borrow money to do so, and my decision on where to borrow money (and how much) is itself very obviously a choice provided by a market, and there are hundreds of commercial (a finance company) or non-commercial (a friend or family member) ways for me to borrow. The choice of an applicant to seek finance from SLC is also a market in action – but because the SLC is the only sensible option for most applicants, it is a market with a state-backed monopoly.

Is this a problem? A “proper market” for student finance would allow lenders to lend money based on an assessment of risk – students studying medicine would find it easier to borrow than students studying history (based on likely future salary and employment), and students with rich parents would find it easier to borrow than students without. Men could borrow more than women. White people more than people of colour. And access to HE by disadvantaged applicants would suffer as a result. Any introduction of competition into the student finance system would increase the proportion of state-backed (assuming the current system becomes a lender of last resort) loans that are not repaid – as the state would offer loans to students who could not raise finance otherwise. The loss would be socialised, the profit privatised.

My choice of car is another market I participate in – though incentives may exist (a grant if I choose a fancy hybrid, differing tax rates for other choices), I can buy pretty much any car I like. Except I can’t if I don’t have the money upfront- I can only spend money that someone will lend me and that rusty old customised relic I’ve fallen in love with may not be something that a lender would assign value to. If a lender did choose to give me money to buy a low-value car, it would be less likely to get the money back if I was unable to keep paying.

In the same way, SLC can only lend money based on a subset of courses and providers that have passed the OfS (and related) quality bar – though it can’t just repossess my BA if I don’t earn enough! There is a quality baseline below which I can’t get finance for my purchase. Above this, SLC judges that the risk that the product I am buying will not offer an eventual salary that I can repay the loan with is acceptably low.

How do I find this new car of mine? I might look on a website or aggregator that lists cars for sale. These tend not to pass independent comment on the quality of an individual vehicle (though they may link to reviews, owner satisfaction surveys, and historic resale values), but most will take some measures to filter out known fraudsters. Some offer a measure of protection if I buy through them; others may align their practices to the needs of particular kinds of sellers at the expense of others. I have consumer protection rights too.

Things are better (or worse, if you prefer free markets) in higher education – both major aggregators (one state-run, the other run by a consortium including nearly all providers) only feature courses at providers above the basic quality bar, and the state-run comparison engine (Discover Uni) offers a range of data about the experiences of previous students and graduates alongside a government-backed rating (the TEF). One curious feature is that there is no guarantee that I could actually get these benefits – if I sign up for a course which the government suggests might lead to a salary premium and I don’t get one, I don’t get to blame the government for providing misleading information. And if a provider receives a poor recommendation based on historic or skewed data, it has very little power to challenge this in a meaningful way.

Vouchers for all

So because of these differences that separate the higher education market from any other market that we might experience, I’ve taken to thinking that our current funding model is a voucher scheme.

I’d explain the system as it is experienced as follows: everyone in England becomes eligible for a government-backed higher education voucher aged 18 and can use it to pay for any one of a list of courses (with the government topping up providers where the cost of delivery is substantially more than the face value of the voucher). The cost of the voucher (plus interest) is recouped (mostly) by the state via a time- and total amount- limited marginal tax rate on graduates.

The vouchers themselves are simple – it doesn’t matter what subject, provider, or course configuration they are used with, provided it is on the eligibility list. Though voucher eligibility is near-universal for English domiciled applicants, not every provider will accept every applicant – other restrictions, such as capacity and academic entry requirements, apply. Though other information and incentives can be employed at both the demand (bursaries, fee waivers…) and supply (strategic subject payments…) sides, there is no mechanism to directly require applicants to use vouchers in particular ways.

There is currently only one broad way to use a voucher – to pay for a higher education course of a defined length and delivery mode. Those who don’t want to study a higher education course in that way (perhaps they want to do a few credits each year while working full time) don’t currently have any other recourse to these funds.

The availability of a higher education course that is chosen through UCAS and fundable via SLC is a simple statement of baseline quality. The provider or course has been judged (by the regulator) to meet the standards expected of English higher education. If the regulator has concerns that a course or provider does not meet these standards, it can do a number of things:

- Remove the provider from the register entirely

- Restrict what the provider can do in the market

- Issue a fine

- Place a public notice on the register of providers to require an improvement

- Work privately with the provider to bring about an improvement

The latter three options do not restrict what the provider can do in recruiting applicants on to courses or on the SLC for lending money with respect to these courses. The use of a condition of registration or a fine where details are made public may have an impact on recruitment, but there is limited evidence to show that this has happened. For the last option, the OfS continues to offer a positive market signal with respect to a provider or course it knows to be problematic. And other sources of information (UCAS, DiscoverUni, the providers’ own prospectus) follow the OfS lead.

Vouchers gone wild

This isn’t a common model of a market outside of the provision of public services. Some compulsory school systems in the US and elsewhere (Michael Barber brought the idea to Pakistan, for instance…) use a voucher system – parents can use a voucher provided by the state to pay for tuition at a range of public and private schools. This brings parental choice as a driver (and thus, it is argued, quality) into the creation of a market where none previously existed, without – necessarily – introducing competition based on price that would accentuate existing inequalities and quality gradients.

To the state, whether a school is public or private, charitable or religious, is immaterial. The funding follows the parents’ choices. In some systems, certain disadvantaged groups of students are eligible for a more valuable voucher – giving well-performing schools an incentive to admit children from poorly performing areas. The argument goes that “poor” schools will fail to enrol students and close, and “good” schools will grow. This same mechanism of change is apparent in English higher education, with the obvious caveat that students are expected to pay the costs of these vouchers back as individual graduates rather than as a component of general taxation that covers all public spending.

In some cases, the voucher may not cover the entire cost of school tuition, and parents or guardians will be required to top up the voucher to meet fees. This is obviously regressive – people with less available resources cannot access certain schools. In most cases, schools are expected to expand to meet demand, although there will be a temptation to limit size for the sake of quality.

Can quality remain constant while numbers are scaled up? To answer that question, we’d need a stable, criterion-referenced outcome measure that is not linked to uncontrollable external factors. We obviously don’t have that in English higher education, unless anyone has any suggestions?

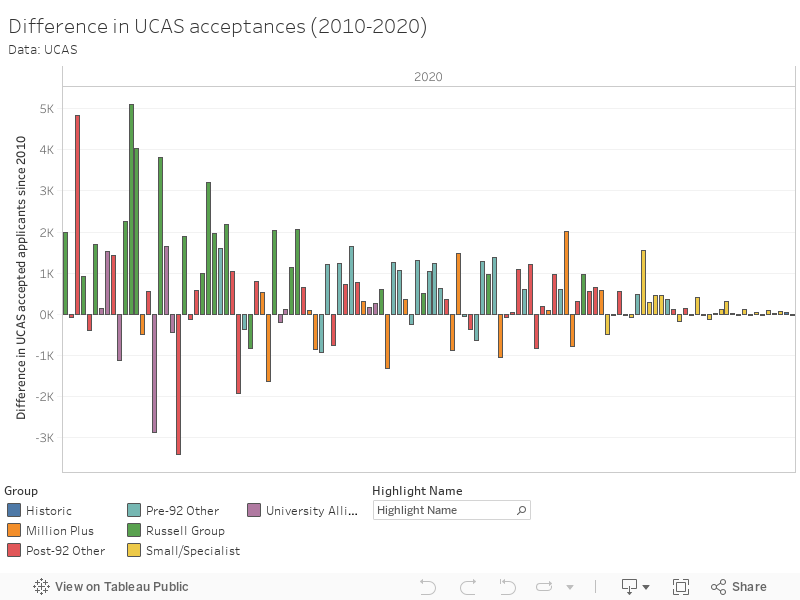

Even just looking at growth or shrinkage in the UCAS acceptances between 2010 and 2020, you don’t see anything that would even suggest a plausible pattern. Some providers have grown, some have shrunk, and you’d be hard-pressed to find two with similar explanatory stories. Have those that have grown attracted more students with high-quality provision or opened the floodgates, quality be damned? Has the market passed judgement on shrinking providers, or have some taken a deliberate decision to focus on quality, not quality? Or in each case – both?

Inequality in a voucher system

The existence of this voucher in English higher education means that directly experienced inequalities in higher education are based on incidental costs rather than the cost of the course – for this reason, means-tested maintenance loans (in a more traditional sense) are offered to students who need them, under the same repayment terms as the fee vouchers. These can be used directly by a student to buy accommodation, textbooks, travel, and food.

But there are also indirect inequalities in higher education – some courses and providers are less likely to have students from disadvantaged backgrounds even though the sticker price is the same. This may partially be because of differences in aspiration, but the most likely explanation is that the record of high educational attainment required for that kind of study is disproportionately found in people with non-disadvantaged backgrounds.

This problem is at least recognised in general terms (the access and participation plans, the oft-postulated idea of contextual admissions), but we’ve never really addressed the fact that disadvantaged applicants have both a financial and an educational (attainment) disadvantage. And it is difficult to lower requirements for some groups because of a need to control demand. At least we don’t need to factor in an ability to pay fees.

But there is a small group of providers that are able to benefit from the voucher system and charge students course fees directly.

More about “approved”, fees, and quality

Surprisingly little attention has been paid to the difference between the “approved” and “approved (fee cap)” registration. It’s worth going over briefly here. Approved providers:

- Are not eligible for OfS teaching funding (the strategic funding allocations)

- Are not eligible for Research England funding (QR and HEIF allocations)

- See students able to access fee loans up to the lower fee amount (currently £6,165 a year for full-time courses, £7,400 a year for accelerated degrees)

What’s not as well recognised is that whereas Approved (fee cap) providers are only able to charge up to the higher (£9,250) fee amount in total with all of this covered by fee loans, for an Approved provider although the maximum fee loan available is the lower fee amount the actual fees charged are uncapped – with the student left to cover the remaining amount. Most Approved providers get around this by accessing student finance in delivering courses validated by an Approved (fee cap) provider and priced at the higher fee cap – but there are exceptions.

For instance:

- Regent’s University London charges £18,500 for a three-year course – £18,495 of this could be covered by the fee loan, with the additional fiver covered by the student.

- But at Hult Business School, the fee is £34,050 for the course (including required fees) – for three years of study, a student could access £18,735 from fee loans with £15,675 required from elsewhere.

- At Buckingham – a two year “accelerated degree” costs £25,200. An accelerated degree at an “Approved” provider is eligible for £14,800 of fee loans, so the remaining £10,400 needs to come from somewhere else.

This is not always made clear, either on UCAS or provider sites. But these are examples of the “top up fee” that caused so much consternation in the early 90s. If the maximum fee loan level is dropped to £7,500, why would these providers be able to charge “top up fees” while others are not? To be clear, I can’t think of a good reason why any providers should be charging students tuition fees directly (I’m with Dearing, and indeed Robbins, here), but the difference between those who can and those who cannot make these charges seems incredibly arbitrary.

There is surely a version of the next few months where the maximum voucher value is reduced to £7,500, there’s no compensation via the treasury, but a crumb is thrown to providers in making “top up fees” a reality for most.

What happens now?

Even without such a shift for some – I’m thinking particularly of smaller, specialised providers that do not conduct much research and are not in receipt of much OfS funding (practice focused arts providers, perhaps) – there is a clear temptation to attempt to maintain the unit of resource by moving to an Approved registration and charging the student. It’s possible that a market for private finance (at less advantageous terms than the government model) would spring up to support this shift.

Larger providers could think seriously about disaggregating – becoming multiple providers with some parts registered as Approved (Fee Cap) and others as Approved. For each subject area, there’s a calculation that could be done that compares fee income, research income, and other OfS income with the likelihood of students to be willing to pay outside of the government system.

If you genuinely believe in the idea of “research-led teaching” or have any concern with the idea of young academics finding jobs that involve time to do research, this would be a real problem. I could foresee entities broadly similar to the CU Coventry model – offering low-cost degrees with the support of a “name” research university, dominating in certain areas or subjects. Great as part of a diverse system, worse if every arts or social sciences provider works in the same way.

Adding the concept of tuition fees and an accompanying finance system to higher education in England was meant to drive up quality and reduce the impact of the sector on government borrowing. It did neither – we got the language of consumption and competition but not any of the postulated benefits.

An uncompensated reduction in maximum fee levels is supposed – as far as I can tell – to save money, make students feel a little better disposed to the Conservative party, and take another “culture wars” kick at universities and academics. It would really only have any chance of succeeding in the latter.

As always, fantastic overview and analysis, David.

As the piece alludes, if I were advising Government I would be flagging the potential chilling effect major changes could have on the Government’s desire for alternate forms of HE delivery, such as accelerated degrees (beyond Buckingham’s offering) and more work-integrated learning. These things are more expensive than a simple ‘economies of scale’ calculation. It would be a great shame if some of these innovative programmes were victims of a rush to bring the headline figure down.

Great overview but shouldn’t you look also at the actual costs of loan repayments both to students and to government? The former will pay something between nothing ( if their earnings remain below the threshold) and a multiple of the nominal loan value if they are high end earners. Either way, students won’t know for 30 years what their degree actually cost them. Similarly, the actual cost of the government subsidy is unknown until the end of the 30 year window for each year’s cohort: the RAB charge is a current estimate of the discounted value of this prospective repayment stream. Smoke and mirrors?

Cheers Mike. We’ve covered the cost to government a lot on the site in the past – I wanted to take other perspectives for this piece.

Understood!

Really interesting, as always. It was a huge shame that the debates in Parliament on HERA (when it was still just a Bill) did not include more detailed consideration of the OfS categories, I think. I wrote about this at the time here: https://www.hepi.ac.uk/2016/11/30/dear-peer-open-letter-members-house-lords-research-bill/

Excellent piece David. Should be required reading for many in Sanctuary Buildings.

The market concept is further complicated by the fact that different institutions (indeed, different courses) will either be selective or recruiting – the whole dynamic is variable across the board.

I also wonder about the extent to which teaching is cross-subsidising research and what that means for the (FT/UG) market dynamic here – especially since many of the new entrants to the market are teaching only.