The clear blue water on student loan interest rates has evaporated

Jim is an Associate Editor (SUs) at Wonkhe

Tags

Ask anyone, and they’ll tell you that interest rates on student loans are usurious. It has certainly felt like that – pre 2012, the rate was just inflation – but for the bulk of the past decade the rate has been set at RPI+3%.

There was method in that madness – a thirty year term plus a repayment threshold were always the counterweights, resulting in those doing well out of their degree paying more, while protecting those who weren’t.

The problem always was that nobody was grateful for the subsidy involved in their 20s (the repayment threshold) and their 50s (the write off), especially when the SLC was sending them a statement every year displaying the principal growing.

So as well as carrying out an instruction from Rishi Sunak’s treasury to reduce the subsidy level overall, DfE moved to address the unpopular interest rate by chopping it back to inflation – while pretty much hiding the distributional impacts and barely mentioning that the threshold was to be frozen and the term would now be 40 years for new starters:

To make the system fairer for students, the student loan interest rate will be set at RPI+0% for new borrowers starting courses from 2023-24, meaning that graduates will no longer repay more than they borrowed in real terms. This meets a key manifesto commitment to address student loan interest rates in this parliament.

That opened up the prospect of the Tories being able to go into the election saying “we scrapped interest on student loans” (by restricting the rate to RPI), with Labour’s (still unannounced) plan involving keeping RPI+3% to allow for stepped repayments.

But the plan’s gone wrong. The interest rate is set on 1 September each year, based on the RPI of the previous March. And last September, RPI was 13.5%.

That doesn’t mean that interest rates actually are 13.5%, or indeed 16.5% for those on the old system. That’s because in the legislation, DfE has to monitor interest rates set by commercial banks using monthly data provided by the Bank of England – and if the average commercial interest rate is lower than the interest rate being charged on student loans, a temporary interest rate cap is set.

In March 2024 that means an interest rate of 7.7% on Plan 2 (ie post 2012 loans), Plan 5 (September 2023 entrants) and PG loans.

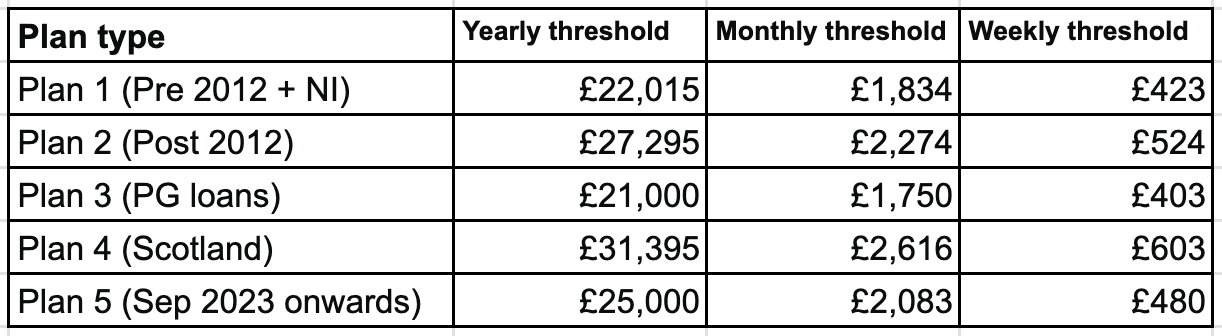

And unless something wild happens, it means that both old system and new system loans will be subject to the average commercial interest rate throughout the run up to the election – all while CPI (RPI is both discredited and being phased out) is down at 4.2% and falling, and while the freeze on the threshold for the bulk of UG loan holders at £27,295 bites harder thanks to increases in wages.

As I say, the problem with having a subsidy via a repayment threshold and a write off is that those benefiting don’t feel grateful. But what’s probably worse is a still high-looking interest rate, entry-level nurses being drawn straight into repayment (the current starting salary for a Band 5 Nurse in the UK is £28,407 per year) and a note that will now say you’ll be paying into your early sixties rather than your fifties.

This seems crazy. No wonder applications for nursing are down.

A recruitment campaign based on the slogan “Become a nurse and get paid £28,407 a year gross, less immediate student loan repayments for the next forty years,” does not look attractive.