Student loan forecasts are out from the Department for Education for England

Jim is an Associate Editor (SUs) at Wonkhe

Tags

This time last year, full-time undergraduate higher education students starting in 2023/24 were expected to borrow on average £42,800 over the course of their studies – and 65 per cent of them were expected to repay their loan in full.

Somehow, in a single year, that’s now fallen to just 56 per cent – and then you get to the small print:

This did not account for the fact that this statistic had been calculated for all borrowers on Plan 5 loans, so it includes a number of years of future cohorts. Over time it is expected that an increasing proportion of Plan 5 borrowers will be forecast to fully repay due to trends in relative RPI and earnings growth forecasts.

It means that for the past few years, DfE’s numbers (which get given to the OBR) have been wrong. Figures on the proportion that will repay in full for the old “Plan 2” student loans (with a 30 year write off) all looked worse than they really were, and the figures for what are now Plan 5 loans all looked better than they really were.

That matters because when Michelle Domelan and Nahdim Zahawi were selling the switch in the last Parliament, they did so on the basis that student finance would be put on a more sustainable footing by “ensuring more students are paying back their loan in full”.

The so-called “RAB Charge” – an estimate of the proportion of the value of newly issued loans which is not expected to be repaid – was supposed to fall from 42 per cent for old style Plan 2 loans issued this year to 21 per cent for the new Plan 5 loans. Partly because of the way the Treasury values money in the future, the actual comparison for this year is now 34 per cent for Plan 2 and 30 per cent for Plan 5.

As well as asking graduates to start paying back the loan earlier, and writing off after 40 rather than 30 years, there was a removal of interest on those on top of RPI. Nobody likes the sound of student loan interest, but the only real impact of that was to let the richest graduates off from paying their graduate tax earlier in their career.

For the rest of the cohort, a massive (and bigger than we thought) chunk are now paying their graduate tax for 40 rather than 30 years to pay for that tax break for the rich – they really do seem to have been mugged off in a fairly straight bit of reverse Robin Hood.

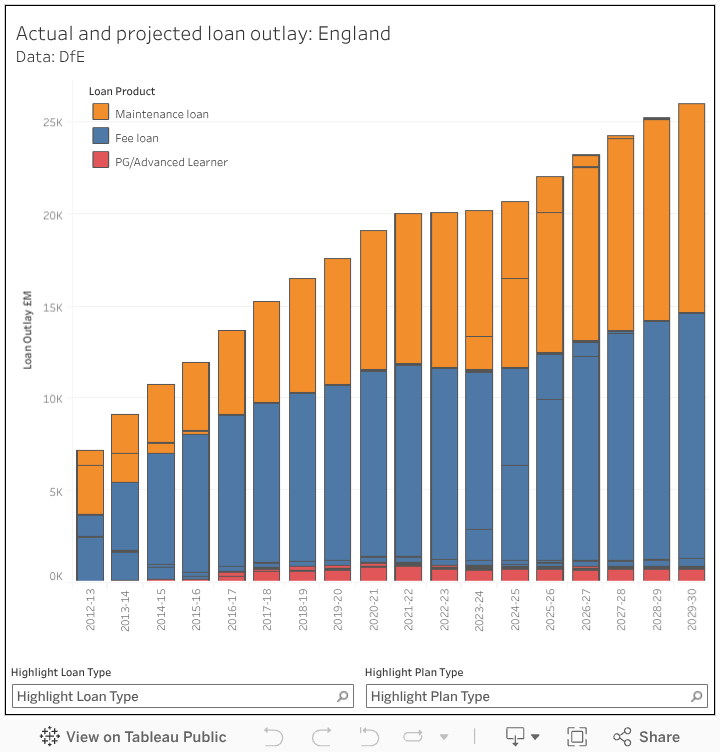

Here’s how the total amounts being loaned out have been (and are set to) changing – the LLE is not modelled here:

Inflationary increases

One little nugget of note in the numbers is to work out what the policy assumptions are that civil servants have been operating under when putting the figures together.

For example, the actual existing policy on home UG fee limits this time last year was that the freeze on the fee was due to end in September 2025.

In other words, when the max fee was “allowed to rise” to £9,535 shortly after the Autumn budget in 2024, Bridget Phillipson didn’t actually do anything – returning to inflationary lifts was already the policy and had been modelled and OBR’d.

Nothing has changed here – so if the inflationary lift for 2026/27 doesn’t come, ministers will actually be making an active cut to what’s been modelled.

Might that happen? Chancellor Rachel Reeves has a fairly sizeable hole in the finances after this week’s Welfare Bill shambles and the winter fuel payment U-turns – and it’s worth remembering that these DfE figures only look at what happens once DfE loans the money out via the SLC.

They don’t cover the huge loss that the Treasury is now making on borrowing the money on the bond markets to loan to students in the first place – which thanks to a mix of Putin, Truss, Kwarteng, Trump and Merz has now become a much more expensive endeavour.

If there’s no inflationary increase, the presentation of it won’t admit that’s a Treasury-imposed cut – but it very much will be if that happens.

Flap flap flap

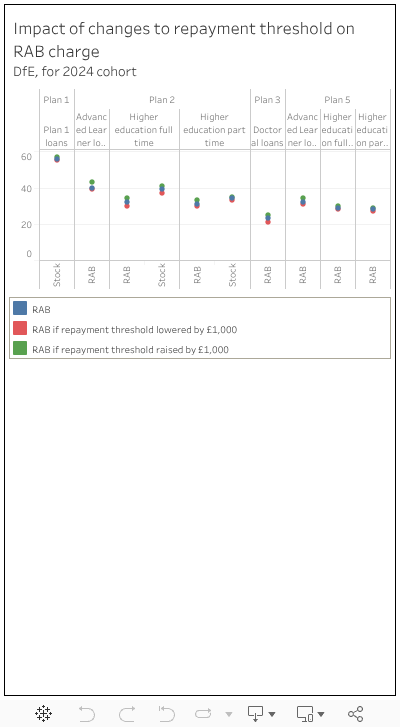

One of the maddening things about the system is that because you’re looking at the value of money up to 40 years from now, the RAB charge can be very sensitive to a butterfly flapping its wings. Here DK has charted up of tiny little changes to projections to average earnings and inflation:

The TL;DR is that if graduate wages go up it obviously makes the system look much more affordable – so that widely discussed collapse in graduate jobs via AI this year ought to make many very worried.

The repayment threshold has quite a bit of an impact too – there is very much an incentive for government to keep it as low (and therefore punishing for new grads) as possible”

Parental contributions

One fascinating little aspect of the release is an excel sheet wrapped in a zip file that’s otherwise not referred to elsewhere – that shows loan outlay, average loan outlay per student, the number of students and proportion of students by Household Residual Income band.

Annoyingly, it’s not broken out by loan type – but if we just look at those borrowers who have declared a residual household income of £25k or more (and therefore having to put in a parental contribution) that’s now climbing quite fast – it was 280k students in 2018-19, but is now 331k. That’s because wages grow over time, but the threshold over which we expect parents to top up hasn’t changed since 2007.

Back on the RAB, it remains the case in these figures that the “RAB Charge” (the estimate of the proportion of the value of newly issued loans which is not expected to be repaid) is 0 per cent for Master’s loans. That’s a creative bit of presentation – the excuse is that:

RAB charges cannot be negative as they measure the level of government subsidy to the student loan system.

You have to get right into the drop-down footnotes to find what’s really going on:

Without this rule, the figure produced by the student loan repayment model using the HMT discount rate is –20.6% for the Master’s RAB charge in 2024-25.

That’s right folks. Every time DfE loans out £1 on a Master’s loan, right now it reckons it’ll be making 21p on it. Quite why the total that students can borrow remains so miserly remains a mystery.