NUS turns its attention to parents

Jim is an Associate Editor (SUs) at Wonkhe

Tags

You may not get the full amount, so you may have to find other ways to fund the rest of your living costs. This could include, for example, part-time work, local authority assistance, bursaries, scholarships, or family contributions.

Part of the problem is the implication that if you do get the full amount, that will be enough to fund your living costs.

The collapse in retail and hospitality jobs and the widespread reduction in bursaries and scholarships (local authority assistance? ha) pretty much wrecks the next sentence.

That leaves “family contributions”, almost as an afterthought. But new research from the National Union of Students (NUS) suggests that for most students, parental support isn’t the backstop – it’s the main structural support holding the whole thing up.

NUS UK has polled over 1,000 parents of current students to understand the economic impact of sending a child to university, and the findings should be uncomfortable reading for anyone who still believes that England’s student finance system should enable young people to study independently.

86 per cent of parents contribute financially to their child at university, regardless of their own income. Most are paying over £200 a month during term time. And almost one in ten are paying over £1,000 a month – that’s £12,000 a year on top of whatever the maintenance loan provides.

Frozen since 2008

The core of the problem will be familiar to regular readers – the parental income thresholds that determine how much maintenance loan a student receives have been frozen since 2008.

Students only receive the maximum maintenance loan if their parents’ income is below £25,000 a year, the same threshold that was set when Gordon Brown was Prime Minister, when the median annual wage was £24,908 – crucially just below that threshold for maximum support.

Here in 2025, the median salary is £39,039, which is significantly above the current threshold. If the £25,000 threshold had increased with inflation, NUS estimates it would now be around £41,000. Put another way, a system that was designed to give maximum support to families on below-median incomes now only gives maximum support to families earning around 60 per cent of that median.

A student studying outside of London with two parents both earning the 2025 median salary – so a household income of around £78,000 – would receive a maintenance loan of just £4,767 a year. The maximum loan for students living away from home outside London is £10,544, so that median-income family is expected to find roughly £5,777 to top up the loan to reach what the government apparently thinks is an adequate amount – and as we know, even that maximum figure doesn’t actually cover average living costs.

Who’s paying for what

The polling gets into the detail of what parents are actually funding. 36 per cent of parents are paying rent directly to their child’s landlord, and another 36 per cent are buying food directly.

And 48 per cent of parents expect their child to work while they’re at university, which means students are cobbling together three separate income streams (loans, parental support, and employment) just to get through term.

Tellingly, 11 per cent of parents weren’t aware they’d need to financially support their child through university. The government website’s coy “family contributions” framing clearly isn’t cutting through – parents discover the reality when the first rent payment is due and the maintenance loan doesn’t cover it.

The impact on household finances is predictably grim. 84 per cent of parents say that supporting their child financially at university has some impact on their household finances, with 10 per cent describing that impact as “severe” and 17 per cent calling it “significant.” Only 15 per cent report no impact at all.

The polling also found that over 80 per cent of parents whose household income is below £20,000 provide financial support to their child while at university. These are families who should, in theory, be closest to receiving maximum support through the loan system – but they’re still having to find money they don’t have to plug the gap.

This is what happens when you freeze thresholds while wages and costs rise. The maximum maintenance loan for students living away from home outside London (£10,544) is over £9,000 below an annual salary at the national living wage. As the report puts it:

…it has gone beyond surviving on beans, students are now surviving on foodbanks.

Meanwhile, NUS’s own 2024 cost of living research found that 93 per cent of students have cut back on costs to save money. While socialising, clothes and holidays were cut by the majority, over 50 per cent had cut back on food, 41 per cent on healthcare, and 11 per cent on sanitary products. Only 5 per cent of students hadn’t cut back on anything.

The system, of course, assumes that parents will provide financial support – but what about students whose parents won’t or can’t? Currently, the threshold for a student under 25 to be classified as “independent” and receive the full maintenance loan is estrangement from both parents for over 12 months.

That’s a high bar, and plenty of students fall through the gap – their relationship with their parents isn’t bad enough to count as estrangement, but it’s not good enough for the financial support the system assumes will materialise.

And things get even worse for these students in their final year.

What parents want

The polling also asked parents what they’d like to see change. 73 per cent said support adjusting the income thresholds to bring them in line with inflation – which would effectively mean a one-off catch-up adjustment plus annual uprating thereafter. 74 per cent support raising maintenance loans in line with inflation each year.

That’s the other ongoing problem in the system – the use of projections of RPI-X by the OBR to set the maximums, when the OBR has been consistently undershooting its inflation projections, a problem that then compounds.

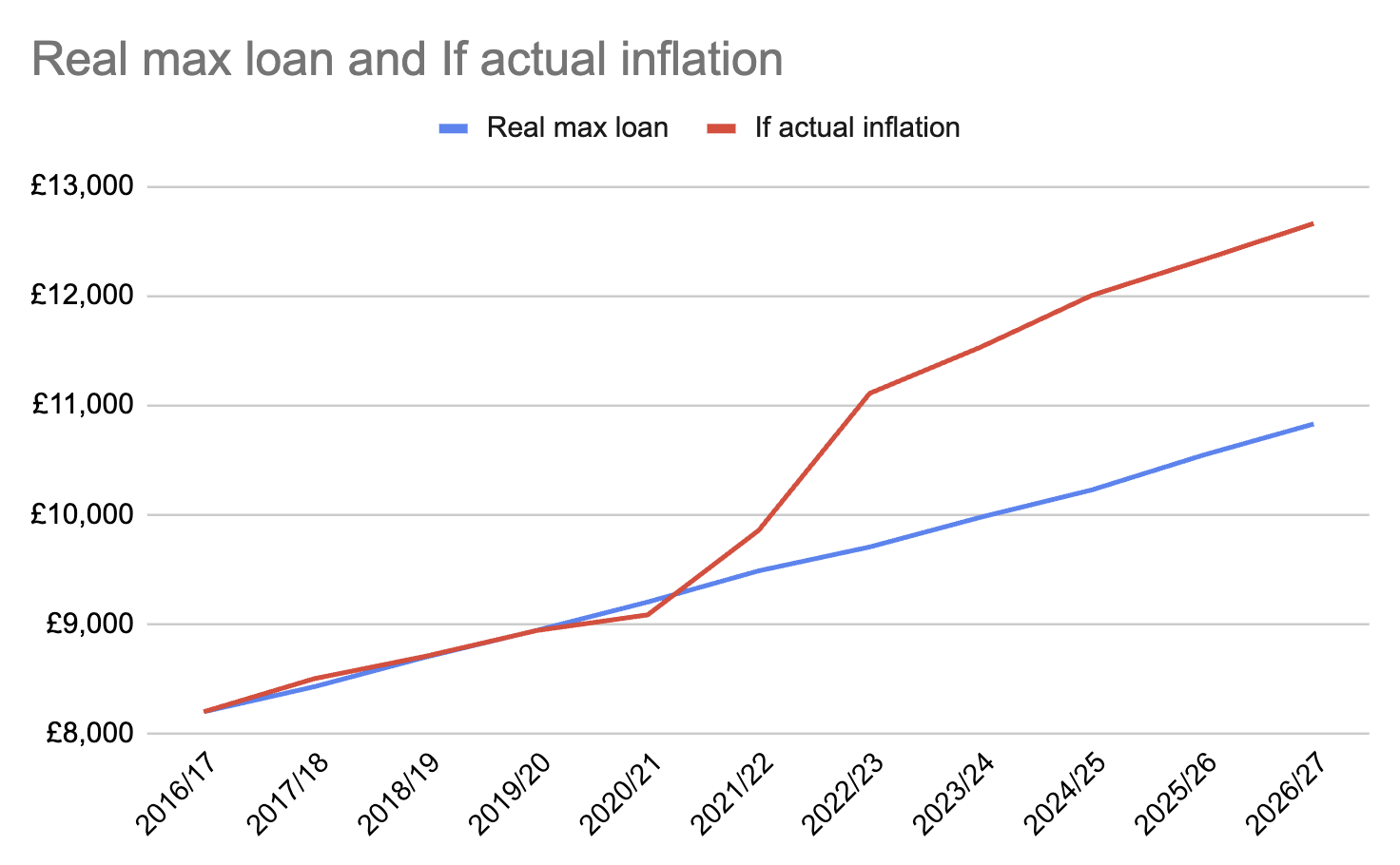

If we take 2016 as the baseline, the gap is now running at just shy of £2k:

NUS’ report says that the government has announced that maintenance loans will increase in line with a “more realistic” measure of inflation for the first time in eight years – it’s not clear what NUS is getting at there, given the use of RPI-X projections is still hardwired in.

Totemic maintenance grants are, of course, being brought back in 2028/29 – but only for students whose parental income is below £30,000 per year and only for students on an as-yet-unknown specific set of courses. Both those criteria, and the continuing freeze on the maintenance loan threshold at £25,000, are far below what would actually address the deficit facing students and their families.

NUS is calling for three things – that the government increase parental income thresholds in line with inflation annually (with a one-off catch-up adjustment), that the maximum maintenance loan be raised to the equivalent of minimum wage and increased annually as such, and that the Student Loans Company make it easier for students to be classified as independent if they’re not supported by their parents.

The stealthy shift

What this research really exposes is that successive governments – of both colours – have allowed the maintenance system to decay through inaction. Freezing thresholds isn’t a neutral choice. When wages rise and thresholds don’t, you’re gradually increasing the burden on families without ever having to announce a cut. It’s austerity by stealth, and it’s been going on for nearly two decades.

But the other bit of stealth is the overall amount that graduates are supposed to be contributing to their HE.

Last week the IFS made some updates to their loans calculator to embed the freeze on the repayment threshold for those on Plan 2 announced by the Chancellor at the budget.

When Willets and Cable introduced £9k fees, the promise was that graduates would contribute around 60 per cent of the costs of their HE, partly via a repayment threshold of £21,000 in 2016, rising in line with average earnings. That would mean a threshold of about £31.5k now.

The Augar review, on the other hand, proposed pegging the threshold at median non-graduate earnings (working-age population). That would mean repaying at £30.5k per year.

But for Plan 5 (post 2022) borrowers, it’s down at £25,000, and for Plan 2, frozen at £28,470.

For new entrants, the IFS makes that a RAB charge of 10 per cent – ie the government is now chipping in just 10p in the pound.

Meanwhile, if you run the numbers on the 2022 entrant system, the government won’t be putting any money in at all – IFS has the RAB charge for a cohort on those rules as minus 10 per cent. Kerching!

So the sums which were used for justifying the original government policy of widening access and participation stopped making sense 20 years ago. I do see any prospect of what the NUS seeks being ever provided by the state, chiefly because the share of government expenditure on defence is going to rise and savings are unlikely to be found elsewhere except government borrowing costs. The cost of providing technical or vocational education and training is lower than for higher education, so government funds could be re-allocated from teaching costs to maintenance costs, which is where we should have begun in 1997 and is now being fulfilled by the higher technical colleges and Skills England.

Now they have built up a massive debt, you can use as an asset against which to borrow for infrastructure investment.

Never mind looking at two parents earning 2025’s median salary. A single worker paid for 37.5 hours a week at national living wage will have a gross income of £24,784.50 from April 2026 (tax code 1257L). It won’t be long before a student of a single parent working full time on NLW won’t be able to get full support.