Mayors will be told to have a plan. But not over student numbers…

Jim is an Associate Editor (SUs) at Wonkhe

Tags

I say potentially – this is one of those moments where we’re relying on Department for Education (DfE) ministers and officials having those regular meetings with Ministry of Housing, Communities and Local Government colleagues that they say they have.

The basic idea is that tenants will be able to make informed decisions when entering into a tenancy agreement, and given that a separate provision will require landlords and agents to publish the asking rent for their property (given it will be illegal to accept offers made above this rate) you’d hope that information will be included in the database.

One extra flag in that database – whether it’s intended that the property will be rented only to students – would suddenly transform the data landscape when it comes to students and rent.

That’s important for all the reasons that the Augar review panel set out in 2019, only to have DfE ministers just pretend that the chapter had never been written.

That said that steps should be taken to ensure that students are given improved and more consistent data on the range and cost of available accommodation, that appropriate benchmarks should be devised for the proportion of maintenance support spent by students on accommodation, and even that OfS should examine the cost of student accommodation more closely – working with students and providers to improve the quality and consistency of data about costs, rents, profits and quality.

After all:

The public subsidy of student maintenance, much of which is spent on accommodation, gives the OfS a legitimate stake in monitoring the provision of student accommodation in terms of costs, rents, profitability and value for money.

I’m not sure at this stage that OfS would be my first port of call for that – but as I say, maybe the Private Rented Sector Database could do a lot of this heavy lifting anyway – notwithstanding that the situation regarding purpose built student accommodation (PBSAs) will need addressing too.

In the Devolution white paper, all areas, with or without a Strategic Authority, will have to produce a spatial development strategy (SDS) – and these will guide local plans, determining housing needs “to support the largest increase in social and affordable housing in a generation.”

For obvious reasons much of the focus is about supply – but for many areas, the issue is also about wild swings in demand caused by… an uncapped free market in university places.

The data we have on student accommodation tends to be awful – property investment firms with a vested interest in X or Y, patchy stuff from website aggregators and a Unipol/NUS (and for London, Unipol/HEPI) survey that appears once every few years.

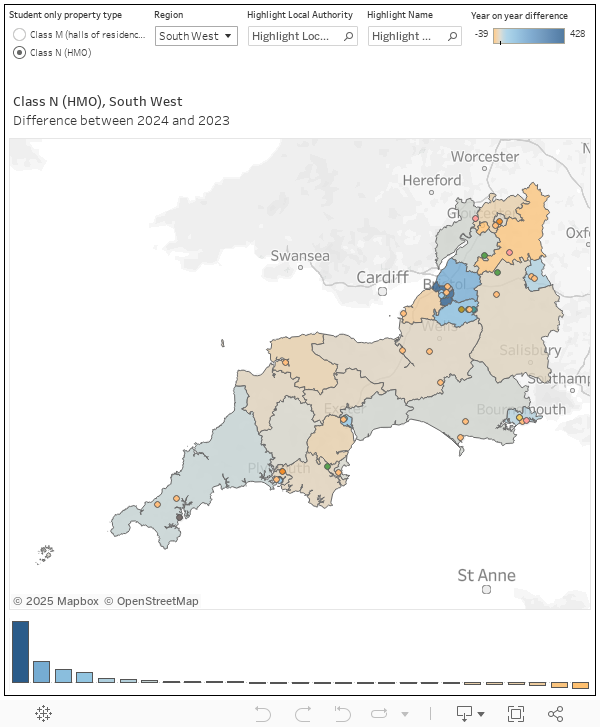

The closest we can get to understanding some of the impacts at a local authority level is our old friend the Council Tax Base data set, which was updated this week.

Unhelpfully, it has a census date of October which doesn’t make it the most reliable intel in the world. Here DK has plotted up the headline figures for the number of “Class N” (houses as opposed to halls) exemptions in each council tax-collecting local authority in England for this year and last year:

Bear in mind here that these figures represent the number of properties that contain only students which have applied for a council tax exemption in the year before the census date. It’s not especially reliable or accurate as an estimate of student housing needs or the student population, and as such you should take these numbers as indicative rather than descriptive.

If we look at the last two years alone, areas like Manchester, Liverpool, and various bits of London saw significant increases in student housing – but smaller university towns like Lancaster, Lincoln and Colchester seem to have experienced sharp declines.

Over the past two years, Class N eligible properties have become more concentrated in the largest hubs, which we can see either when looking at increasing maximum values, the interquartile range, or the standard deviation between LAs.

The biggest areas are getting bigger, while the long tail is getting thinner. That could be about shifts in student enrolment patterns, changing housing market dynamics, and local policy decisions impacting housing incentives or restrictions – or maybe that students are in halls instead.

Or maybe not. The correlation between the increases in Class N (private student properties) and Class M (student halls) from 2022 to 2024 is 0.86 (with a p-value of 3.71e-07, essentially zero). That indicates a pretty strong positive relationship between the two.

In other words, areas that experienced growth in one category (e.g., Class N) tend to also see growth in the other (e.g., Class M), and areas with declines in one type of student property generally saw declines in the other.

Policy is always about trade-offs. The supposed advantages of the uncapped market in student places is normally extolled on the basis of individual choice. But if that’s a choice only exercisable on the basis of personal resource, it’s a highly faulty one.

OfS is in theory worried about that – Risk 11 in the Equality of Opportunity Risk Register notes that increasing student numbers may limit a student’s access to key elements of their expected higher education experience, and could disproportionately affect those without the financial resources or wider support to react appropriately:

For example, where appropriate student accommodation is limited, students with less money or who are accepted at a late stage in the application cycle, may not be able to secure suitable housing.

I’m going to go ahead and predict that despite its appearance in the EORR, there won’t be many providers that will have put in place a bunch of meaningful mitigations on that risk. And if the theory of change on that risk is provider recruitment restraint in a sector-wide financial crisis, the theory of change is probably duff.

Perhaps the market is shifting so students moving away from home will tend to live in cities (with inevitable health implications), while universities in towns recruit local commuters. If that is a plan rather than a trend, we need to ask what now happens to all the PBSA in the latter. It’s not as if PBSA can be easily switched into serving other citizens – it was, (clue in the name), “purpose-built” for students.

But this is also about pace. Pulling planning levers takes time. Shifting away-from-home student populations out of towns at high speed, as they take up places at higher tariff providers (or, in the case of international students, decide not to come) leaves a very different kind of economic impact in its wake, and a lot of empty buildings.

And it means finding affordable rental properties in cities is even harder – for both students and other citizens. Asking local authorities to plan strategically when demand generated via students can shoot up and down so fast is a recipe for disaster.

If, for example, we were to surmise that a given university location needs to have in its vicinity a calculated stock of affordable and safe property to support the housing needs of its students, the painful international bust we’re seeing now would never have happened – because there wouldn’t have been such a big boom in the first place. Sliding doors, and all that.