Investing for the long term often loses out to pensioner power

Jim is an Associate Editor (SUs) at Wonkhe

Tags

As a result of today’s announcement, a pensioner in England with an income of £34,999 will get extra help with their heating bills.

In fact, given a quirk in the system, a two-pensioner household where both earn £34,999 – so earn £69,998 in total – will also get the benefit.

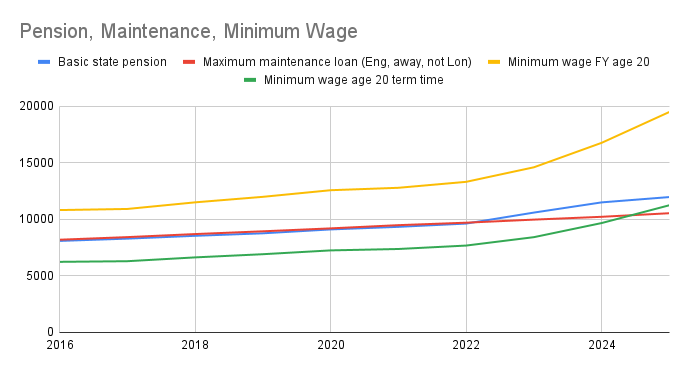

Meanwhile, a single parent in England on £34,999 who has a child at university (away from home, not London) will be expected to top their child’s maintenance loan by £1,506 a year.

Loan, not grant. And if they’re away from home, they won’t be living on £9,038.

Meanwhile, the full new State Pension for the year ahead is £11,973.

There’s a million reasons why the theoretical maximum maintenance loan for students should not be compared with the Single Tier Pension (STP) rate – one’s a loan, one’s not, one is means tested, one isn’t, both may be topped up by other benefits or other income, there are different costs, one is more likely to be renting while the other more likely to have paid off their mortgage, I could go on.

But one of the reasons I think it’s important to make the arbitrary comparison is because of how closely the STP rate and the minimum wage used to track the maximum maintenance loan rate – and how far apart they are now, partly because they symbolise, in an unspoken way, what we think people can live on.

Here they are compared, along with the 18-21 minimum wage for 30 weeks at 37.5 hours a week – bearing in mind that the student maintenance loan is a means-tested, maximum loan:

There are plenty of wags on the socials making the point about the UK state being basically pensions (spent on the elderly) and health (where a huge proportion is spent on the elderly), with a couple of other dwindling twiddles added on.

Wrestlegerontonomia

More sophisticated versions of the observation are available. My favourite comes from Tim Vlandas, who’s an Associate Professor of Comparative Social Policy at Oxford University.

He argues that right across advanced democracies, a demographic drift is turning the median voter greyer, richer in assets, and more conscious of prices – and that this grey-tinged gravity pulls policy priorities towards pensions, healthcare, and low inflation, all while pushing education, childcare, and growth-boosting investment to the periphery.

Governments, eager to placate electorates in which older citizens both outnumber and out-vote their juniors, start off all pro-growth – but as the realities of elections loom, duly protect pension promises (the triple-lock here) and pursue price stability, even if that means accepting anaemic growth, higher unemployment, and chronic under-investment in human capital in the long-term.

He calls this a “gerontonomia” – states sustained not by autocratic diktat but by democratic demand, where the socioeconomic comfort of today’s retirees is purchased at the cost of tomorrow’s dynamism.

He does caution against caricature. Elderly voters aren’t monolithic, nor are they solely selfish – but their structural position (out of the labour market, shielded by public pensions, and less likely to reap long-run returns from social investment) tilts their preferences in predictable ways.

Three things then amplify the outcome – the crowding-out of growth-friendly spending, contractionary zeal in the fight against inflation, and a curious electoral immunity whereby stagnant economies hold on to incumbents, as long as pensions keep pace with prices.

The result, he warns, is a democratically endorsed economic stagnation that may, in time, erode faith in democracy itself among younger cohorts frustrated by a system seemingly stacked against their future. Cue populism.

He leaves readers on a big question – whether capitalist democracies can recalibrate before the cycle of grey power and slow growth tightens further, with the alternative remaining stuck in a status-quo sustained by silver-haired voters, stable prices, and stunted prospects.

Turning (to the) Japanese

One country that is often pointed to on the impact of an ageing population is Japan.

With 30 per cent of its population over 65 (it’s about 20 per cent in the UK), Japan’s grey voters are widely believed to have created this sort of gerontonomia effect – an electoral dynamic where the government prioritised pension protection and inflation control over growth-oriented investments like education (Japan ranks among the lowest OECD spenders) and structural reforms.

That has produced what the theory predicts – decades of minimal growth that voters tolerate because older citizens are insulated from unemployment and wage stagnation, while politicians avoid disruptive changes that might threaten asset values or pension security.

The result has been a self-reinforcing cycle where the Liberal Democratic Party has (until recently) maintained power through older voters despite presiding over economic underperformance, creating what has amounted to a democratic mandate for stagnation.

That has, though, been starting to change. Japan has recently achieved its inflation target after three decades of deflation, and there’s real wage growth for the first time in ages. Unlike, say, England – where we’re increasingly relying on parents to fund students through higher education (with all the social inequality that beings), Japan began to reduce student reliance on parental funding in 1999, when the Japan Student Services Organization (JASSO) introduced a major expansion of its student loan system – relaxing eligibility criteria and increasing borrowing amounts available through low-interest Category 2 loans.

That dramatically expanded access to higher education financing – although it did leave graduates with huge debt burdens that often exceeded their ability to repay, and financial hardship for increasing numbers of borrowers. That system’s limitations became apparent as evidence emerged that prospective students from low-income households were actually forgoing university education to avoid debt, while real wages stagnated and non-regular employment increased, making loan repayment increasingly difficult.

That drove further reforms – including the introduction of income-contingent repayment options and ultimately the 2020 establishment of grants – representing a recognition that the loan expansion, while democratising access to higher education, had just shifted the financial burden from parents to students themselves rather than really addressing affordability.

Not that the LDP has been thanked for it. While it has historically relied on older voters, even that base has been becoming frustrated – the party’s failure to address structural economic issues that affect retirees, like inflation, healthcare costs, and family security, has weakened their traditional support.

Some argue that the party became so focused on maintaining the status quo for older voters that it failed to invest, innovate or address long-term structural problems – and then when scandals broke that threatened basic competence and honesty (a slush fund scandal involving the party factions Seiwakai and Shisuikai kicked off last year), the party lost its core legitimacy even among its traditional base. The party then suffered its worst performance in over a decade in the October general election.

Hence with Japan’s population projected to fall from 122.6 million today to just 87 million by 2070 – with only 45 million of working age – the arithmetic of democracy is becoming impossible. The government (as in the UK) is looking at a shrinking workforce that has to support expanding elderly care needs while it already carries public debt at 260 per cent of GDP – a fiscal trap where any solution alienates core constituencies.

Raising taxes on working-age voters to fund elderly benefits is politically toxic with a diminishing workforce, cutting benefits loses them votes given older voters’ dominance, and continued borrowing is increasingly unsustainable as debt ratios climb toward dangerous levels.

Tooling up?

Can capitalist democracies escape traps like this? IMF economists like Gee Hee Hong and Todd Schneider frame Japan as the world’s “policy laboratory” for aging societies, and the government’s own Population Strategy Panel – 28 business and academic leaders – has proposed comprehensive reforms involving lavish, long-term investment in education and research and innovation.

Its January 2024 blueprint treats universities as a central plank of its “people-investment” agenda – it says public education will need to cover the full pathway “from early childhood through to university and other forms of higher education”, urges wider open access to high-quality digital course content, calls for lower tuition fees through greater public support so that household income no longer dictates study prospects or graduate incomes, and presses for a step-change in quality via smaller classes, ICT-rich teaching and industry-linked career education to ensure graduates’ skills match labour-market needs.

Meanwhile Gee Hee Hong and Todd Schneider also argue that Japan has to treat human capital investment as central to its demographic strategy. There’s a “higher technical” aspect to it – they argue for a need for universities and vocational colleges to expand STEM, digital, and lifelong-learning provision – all of which requires investment.

But how do you get electorates to pay for it all? Gee Hee Hong and Todd Schneider acknowledge that demographic and electoral calculations limit room for new borrowing – so they call for a gradual but relentless consumption-tax rise to pre-fund old-age costs and free up cash for productivity, participation, and skills policies.

Because levies like that are broad-based, older households pay too – but they argue that early, predictable increases hurt less than sudden pension cuts later, and spread the burden more fairly across generations. Whether the the LDP is punished for it – and whether retirees will accept the logic – remains the big question. But at least Japan is asking that question.

Government’s operate under a budget constraint and so every £ spent supporting one group is a £ that cannot be spent elsewhere. WONKHE contributors have a habit of forgetting this so it is good that Jim flags this inconvenient truth. However, there is no necessary tension between pensioners and students. The Government could decide to support both by raising income tax or VAT. Most taxpayers, however, do not benefit from degrees. In contrast, provided they live long enough and make 35 years of contribution to national insurance, all tax payers will one day receive a state pension. And if the current rules prevail, three-quarters of them will receive winter fuel allowance. Surveys repeatedly show majority support for a shared cost model for higher education with only around 35% support for ‘free’ University tuition funded out of general taxation. There has also been increased funding for vocational training, making up to an extent for the cuts this sector had to deal with after 2010 which higher education did not share in proportionately. There is broad public support for this policy even if it requires higher taxes. The Social Market Foundation found that nearly three-quarters of the public supported increased investment in vocational and technical education, even at the cost of higher public spending. Their survey also reported that nearly half felt the Government gave too much priority to Universities over technical training. YouGov polling is similar. Labour ran for office on a mandate for change. They would say, Jim, that this is what they are offering.