Ditching interest and debt would blow the debate about HE funding wide open

Jim is an Associate Editor (SUs) at Wonkhe

Tags

The problem is that most of them fall into the classic trap of bemoaning that graduates don’t seem to be shifting much of the principal through their repayments – a “weighed down with debt” framing which promotes Ts and Cs which enable graduates to “repay” more of that “debt”.

Other frames are available.

As well as a continued freeze to the maximum tuition fee and a miserly increase in maximum maintenance loans, there are really three major aspects to Michelle Donelan’s “stealth” reforms to student loans from last year to take note of:

- A reduction in interest rates to RPI only – so graduates will not repay more than they originally borrowed over the lifetime of their loans when adjusted for inflation;

- The introduction of a £25,000 per annum (increasing with inflation from April 2027) repayment threshold;

- A 40 year write off period (up from 30).

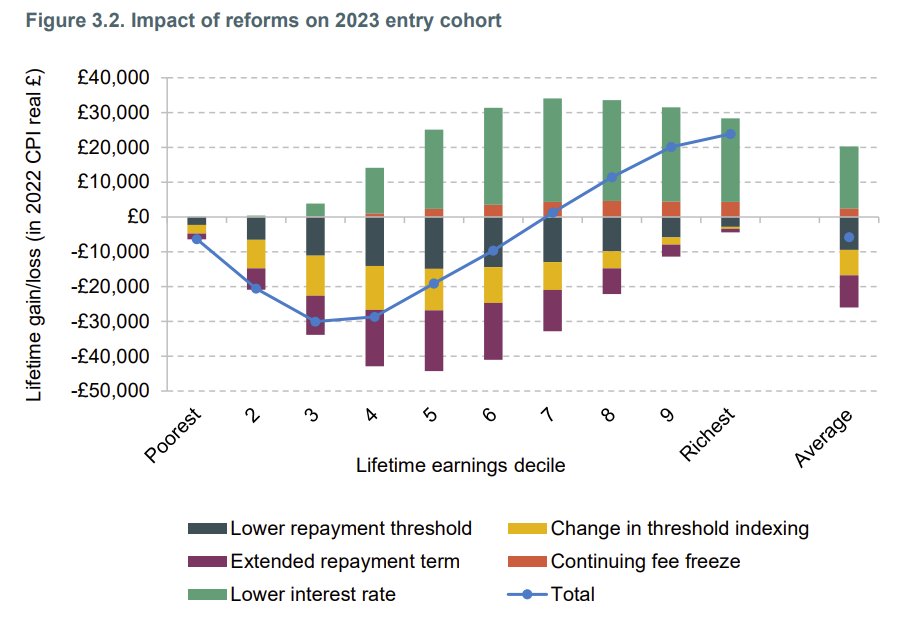

We’ve discussed before here the relatively regressive nature of these changes when it comes to repayments (this chart from IFS):

Right now the majority of “borrowers” in fact just pay the “graduate tax” for thirty years – and all the interest rate and balance do is upset people and determine who gets let off the graduate tax in their late 40s because they’ve “repaid”.

So reducing interest means the richest will stop paying the graduate tax even earlier, and increasing the term will mean everyone else pays more because they’re getting less of a subsidy via that write off.

The big question though, in the context of that miserly increase to maintenance loans, is what we might be able to afford to do if we cancelled the egregious windfall for the rich but kept the 40 year term.

To do so we can play around with IFS’ Student Finance Calculator (noting that we have to amend its current switches for the September 2023 Plan 5 system, which seem to be wrong on the repayment threshold that will apply) by seeing how much different policy options cost.

If we’re trying to price up the “long run” (ie adjusted for inflation) cost of a September 2023 cohort, we see:

- Pre-Donelan reforms £5.2bn (subsidy of 18p in the pound)

- Donelan reforms £4.2bn (subsidy of 14p in the pound)

How? Well, to pay for that interest rate and to give a bit back to the Treasury, the repayment threshold and the 40 year term aspects were created.

If for example we abolished that interest rate cut, the difference would be so dramatic that the subsidy would end up at –20p (ie the government would make a long run profit of £2.4bn).

But what’s astonishing is that even if we then topped up maintenance loans to where they should be, and dealt with the family household income threshold where we start to deduct down from the maximum entitlement, there would still be a long run profit.

In fact if the calculator is right and we chose to keep the 40 year term but turned it into a long run graduate tax for everyone (rather than letting the rich off), we could:

- Match the value of the Wales student finance package (linked to national living wage and no parental threshold)

- Create a £2,000 per head teaching, learning and support fund to be spent on priorities etc

- Create a £1,000 per head uplift for every students’ union

- Create an additional £1,000 per head civic student support fund to be spent in accordance with student determined regional priorities

…and STILL the there would be no overall subsidy on student loans, and even then when I say “everyone” I’m not counting what we’d raise from those who pay upfront and buy their kids out of the system.

The point is that very very few people realise quite how expensive Donelan’s giveaway to rich men has been, and the extent to which it is strangling the unit of resource available to pay staff, or allow students to pay for food and rent. It’s a hidden giveaway that is preventing meaningful debate, and when folks like Policy Exchange host debates on student finance without mentioning it they’re making people like me choose between SNCs and putting the heating on when we almost certainly don’t need to.

And so if the government just created a 40 year graduate tax (with repayments pro-ratered based on credits) it could very easily fix a huge multitude of problems in HE which involve spreading an ever-thinner pie around.

I’m noy saying a 40 year “term” is what I’d propose, I might still means test some bits of student finance, there’s a debate about grants v loans, I might have a higher repayment threshold or a lower repayment rate and I would want more of any increased unit of resource to be deployable by the government rather than the voucher following the student.

But anyone operating within the unspoken parameters of “it must be a loan” and “that loan must have no real interest” that then tries to argue for maintenance or “fee increases” is falling for a fiscal framing trick that makes pretty much every option unpalatable to the Treasury.

The sooner Labour gets on and grows a backbone over a graduate tax – requiring it to own its own frame rather than just play within the trap laid for them by the Conservatives’ – the better.

And next time someone in the debate mugs you off by not mentioning what else we could do with the price of Donelan’s gift to rich men, call them on it.

I agree with a lot of this but two points to add:

1. Analysis of whether student loan changes are progressive or regressive tend to look just at data covering those who enrol on HE courses (about 50% of the cohort). The changes proposed in the 2019 Post 18 review (40 year repayment period, new threshold) were intended to redistribute funds within post 18 education (eg from HE tuition to FE plus maintenance). 2023 Donelan package didn’t secure this.

2. Another issue about changing student loan terms and/or bringing in graduate tax features is whether this just encourages well off parents/grandparents of some HE students to pay the tuition and maintenance directly. This 2020 research suggested those with home-owning families, who’d been privately educated, whose parents didn’t have degree or who are female all a bit less likely to take out student loans

https://www.researchcghe.org/publications/research-findings/the-determinants-of-student-loan-take-up-in-england/

Abolish the maintenance loan/grant and allow students to claim universal credit.

Based on this, the cut in student loan interest is costing £6.6bn per cohort. That intuitively sounds like it must be too high but, even so, it is incredible that it did not get reversed once the fiscal situation became very bad around October time – an odd priority for nearly £7bn per year of spending…